AleaSoft, January 10, 2019. The cold snap that has reached Europe is having an impact on electricity prices and demands in electricity markets. AleaSoft analyses the main European electricity, fuels and CO2 markets, as well as the Spanish market and electricity system in the last December, the second most expensive December in the decade and the third in history.

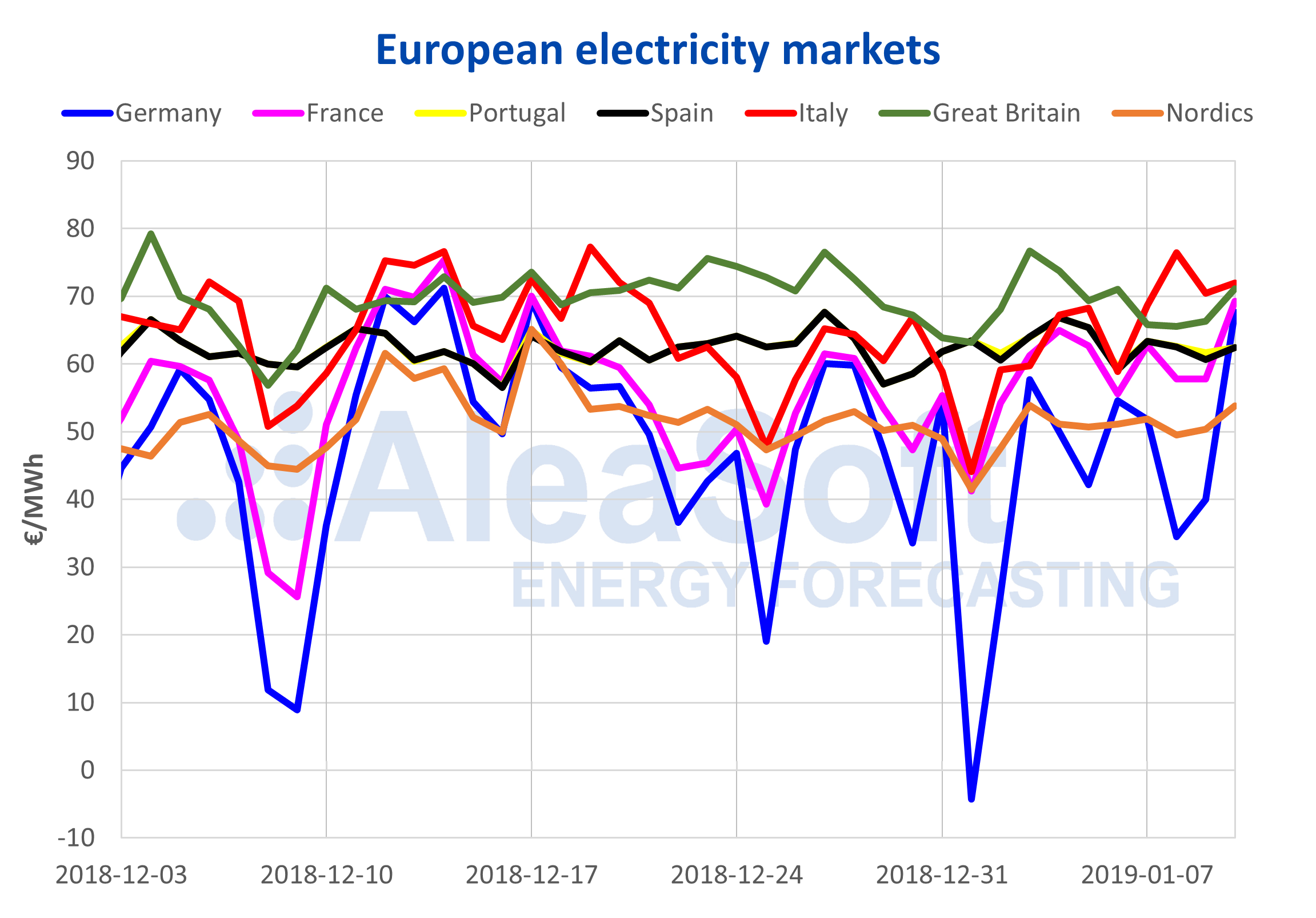

The price of the wholesale Iberian electricity market in Spain for January 10 was 62.40 €/MWh, the lowest price for that day among the main European markets, with the exception of the market of the Nordic countries, traditionally the lowest. The cold snap that has begun to hit the European continent has brought a rise in prices that has placed the French and German markets close to 70 €/MWh and the British and Italian markets above that, also influenced by the fall of wind energy. This week, since January 7, started with prices in the main European electricity markets around or above 60 €/MWh, except for the German and the Nordic countries markets that remained around or below 50 €/MWh.

Sources: Prepared by AleaSoft with data from OMIE, , N2EX, IPEX and Nord Pool.

Electricity futures contracts are trading at lower values this week compared to the previous one, following the behaviour of gas, coal and CO2 futures. Futures for the second quarter (Q2-19) fell by 3.7% in Spain and Portugal, and by 3.4% in France and Germany.

OMIP at Y+7

The Iberian market for gas and electricity derivatives OMIP has begun to offer electricity futures trading for Spain and Portugal for seven years ahead, until 2026. The average price for Spain contracts for the next seven years is around 49 €/MWh. The challenge will be that sufficient liquidity is achieved for such long-term contracts, so that it is a sufficiently robust price signal for the market.

Brent, fuels and CO2

The price of the Brent oil barrel keeps its upward trend since it hit bottom on December 24, and yesterday, January 9, futures for March exceeded the $60-per-barrel barrier and settled at $61.44. Progress in trade negotiations between the US and China created an optimistic climate and producing countries see how the production cuts agreed last year begin to have an effect on the price. If the agreements are fulfilled, the reduction in production will continue in 2019, so, for now, the trend is expected to continue upward.

Sources: Prepared by AleaSoft with data from ICE.

The price of gas and coal futures stands this week, of January 7, below the prices of the previous week, 2.8% for the TTF gas and 3.5% for the API2 coal. But forecasts of a colder January end and a cooler than usual February could create an upward trend for the coming days and weeks, although high levels of coal stocks make this trend less solid.

On the other hand, the entry into operation of the CO2 emission rights Market Stability Reserve on January 1 has not succeeded, at least for now, in making the price of CO2 to begin the recovery of the level of the 25 € per ton lost last week, on January 3. At the moment, yesterday, January 9, it settled at 22.04 €/t. It should be noted that in February the auctions in Germany will resume, which will put on the market the pending titles of the last auctions of the year 2018 that were cancelled, and we will see how this increase in the supply affects the price.

Spain

Electricity demand this week is shaped by the return to normality after the holiday season. AleaSoft‘s forecast indicates an increase in demand of 13.5% this week, of January 7, compared to the previous week. Part of this increase is due to the recovery of labour and school activity, but also to the drop in temperatures, which during this week will be on average 1.5 °C below the usual temperatures for these dates and 0.2 °C below the average temperature of the previous week. According to the estimates of AleaSoft, correcting the effect of festivities and holiday season, the increase in demand for this week stands at 1.3%.

For the following week, of January 14, the weather indexes of AleaSoft point to a slight recovery of the temperature that will increase on average around 0.1 °C, although by the end of the week important temperature drops can be seen. In addition, labour activity will also increase given that Monday, January 7 was a holiday in some regions. All this, according to the AleaSoft‘s forecasts, will lead to an increase in demand of around 2.5%.

Hydroelectric reserves decreased by 1.5% last week and stand at 10 022 GWh this week. These values represent an increase of 39.8% year-on-year, and are practically at the average level of the last ten years.

Sources: Prepared by AleaSoft with data from REE.

Wind and photovoltaic energy

Wind energy recovered this week after a very discreet production during the Christmas and New Year weeks. According to AleaSoft‘s estimates, wind energy will be 79.6% higher this week of January 7, compared to the previous week. Regarding the forecasts of solar energy, which includes both photovoltaic and solar thermal, AleaSoft‘s estimates indicate an increase in production of 7.5%.

December summary of the Spanish electricity market

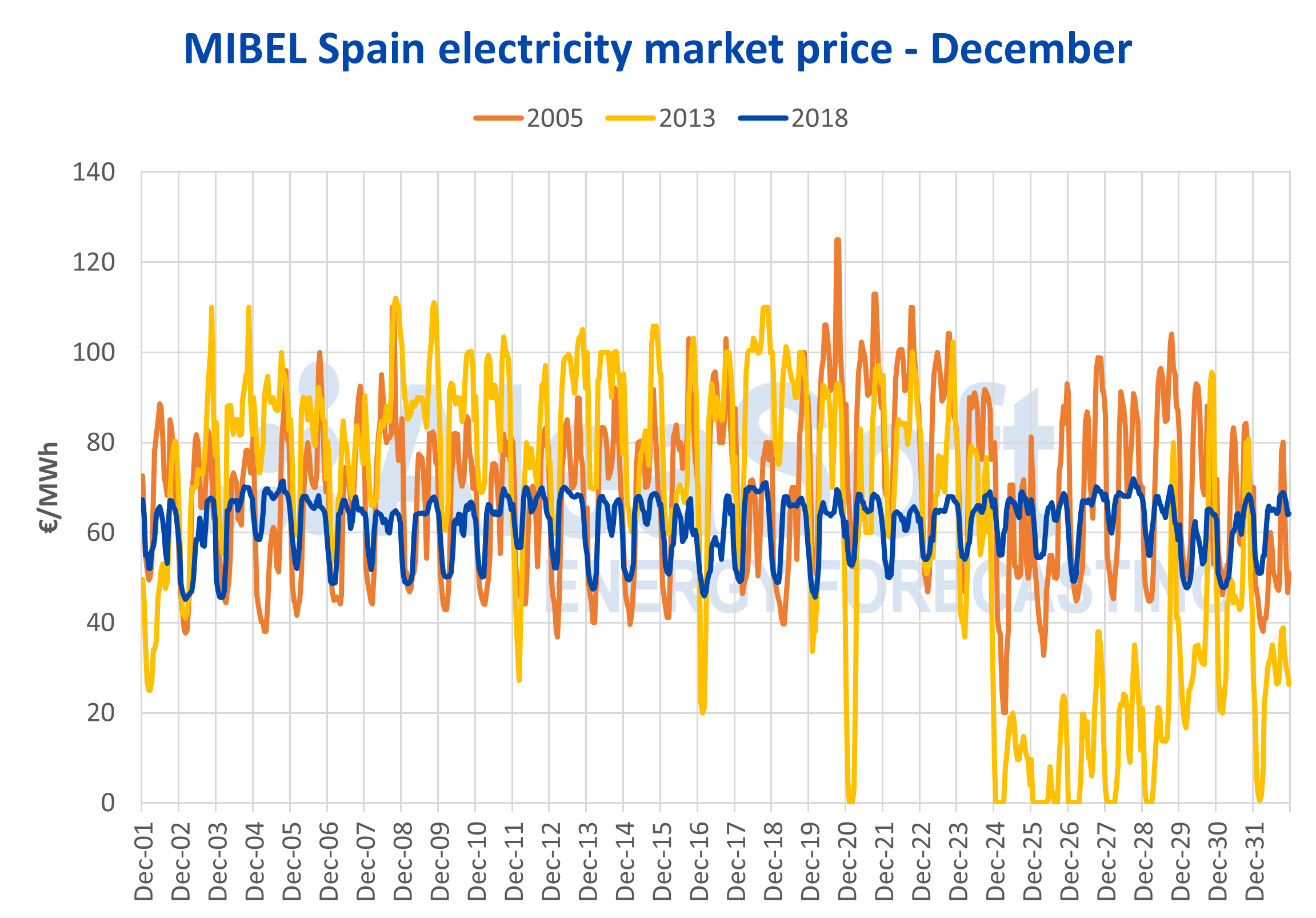

The average price of the day ahead electricity market MIBEL in Spain in the month of December was 61.81 €/MWh, which represents a decrease of 0.16 €/MWh compared to the month of November, but an increase of 3.87 €/MWh compared to December 2017. And this December was the second highest in the last decade and the third in the history of the Iberian market, after 2005 and 2013. That said, the extreme hourly prices of December of 2005 and 2013 were very different from those of 2018. In December 2013, 37 hours recorded a price zero, and the maximum hourly price was 112.00 €/MWh; and in December 2015 the maximum hourly price reached 125.00 €/MWh. While, in December 2018, the hourly prices were much less extreme: the minimum price was 45.15 €/MWh and the maximum price was 71.97 €/MWh.

Among the causes of this high price for December are the price of CO2 emission rights, three times higher than in December 2017, and a renewable production 3.6% lower than in December of the previous year.

Sources: Prepared by AleaSoft with data from OMIE.

The demand for electricity in mainland Spain in the month of December was 21.2 TWh. Comparing this data with that of December 2017, the demand fell by 4.3% despite the fact that December 2018 had one holiday less. But, on the other hand, this December recorded much milder temperatures, 1.5 °C higher on average than December 2017, and this was the main cause of the decline in electricity demand.

Wind energy was 25.1% lower than in December 2017. Solar energy also decreased, 3.7% for photovoltaics and 1.5% for solar thermal. The most outstanding data of the production by technologies is, undoubtedly, that of the hydroelectric power plants, which, with respect to the previous December, increased by 100.5%, clearly showing the end of the drought period.