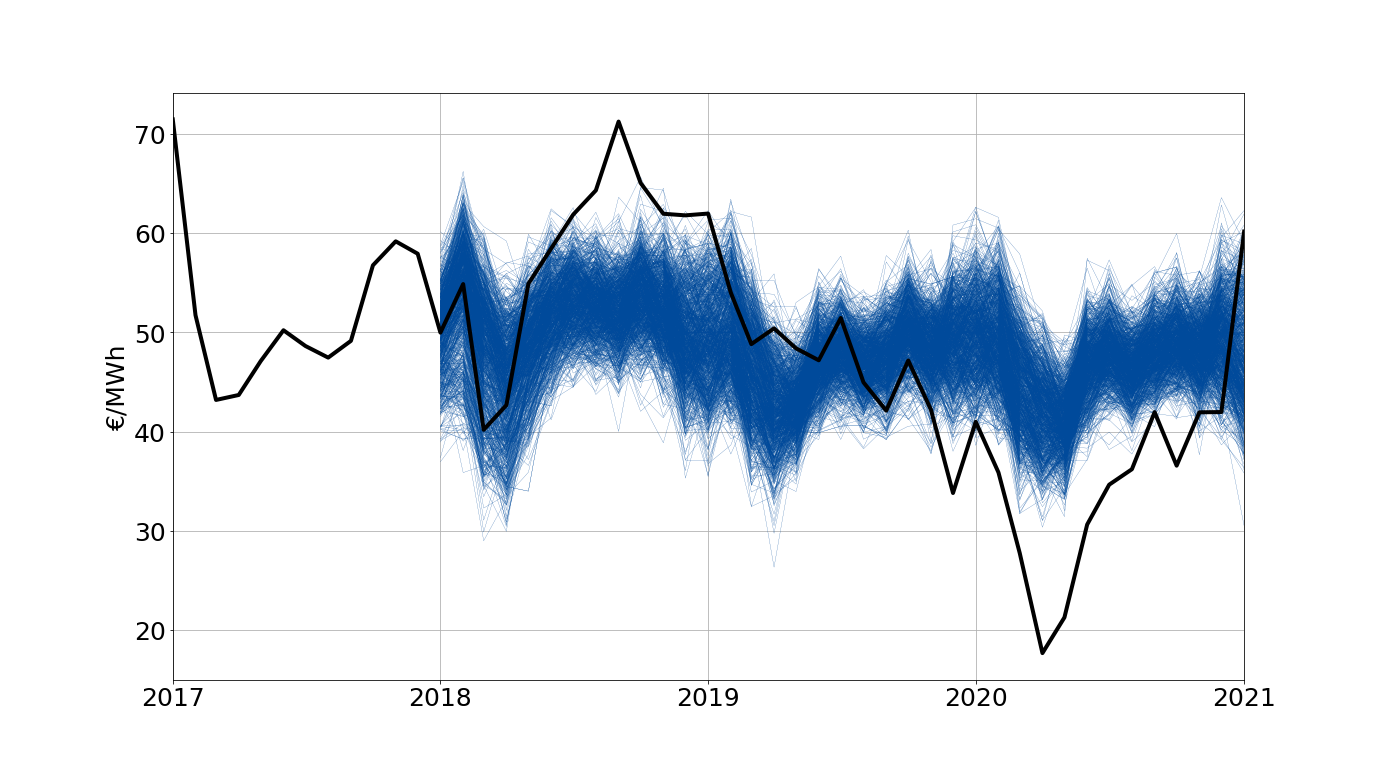

AleaSoft makes price forecasts for European markets in the medium term. The price forecasts have an hourly granularity, a 3-year horizon, and include probability distributions (forecasts with stochasticity) for each period (month, quarter and year) within the forecast horizon.

Forecasts with price stochasticity allow us to analyse the impact of the stochasticity of the explanatory variables on the medium-term price forecasts, and are a basic tool for risk management and the calculation of Values-at-Risk.

Price forecasts are calculated using data from the distributions of the explanatory variables and their associated probabilities. The main variables26 that are obtained stochastically are the following:

- Temperature.

- Demand (obtained from the stochastic forecasts of temperature).

- Production wind.

- Production 42solar.

- Production hydraulic.

- Price of Coal.

- Price of Gas.

- Price of rights emissions of CO2.

For each of them, their intrinsic variability is estimated based on their values historical.

A sufficiently high number of random forecasts is calculated for each of the explanatory variables consistent with each other. With these simulations of the variables, the corresponding simulations of the market price are calculated, and from these the percentiles of the price distribution are calculated.

Stochasticity will be generated using all the recorded data available at that time.

The shipment will include the probability distributions for each monthly, quarterly and annual product being currently trading in the futures markets within the forecast horizon. For each period, the distribution will include a reference to the latest prices traded in the stock markets. futures.