AleaSoft Energy Forecasting, September 15, 2025. In the second week of September, prices in most major European electricity markets increased, although the weekly average remained below €75/MWh. Several exceeded €100/MWh on some days, with Germany leading as it registered its highest daily price since February, €142.45/MWh, on September 9. That market also exceeded €400/MWh in one hour on September 8. The increase in demand and in gas and CO2 prices drove the markets, with CO2 futures registering their highest settlement price since February. Spain and Portugal registered all‑time highs in photovoltaic energy production for a day in September.

Solar photovoltaic and wind energy production

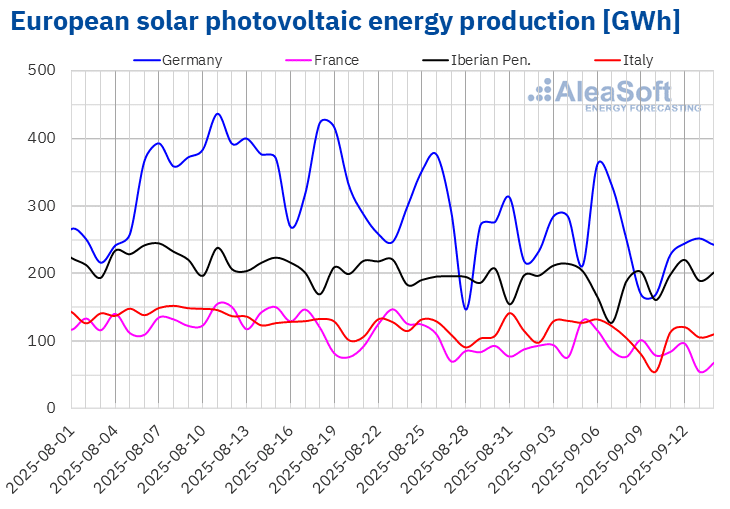

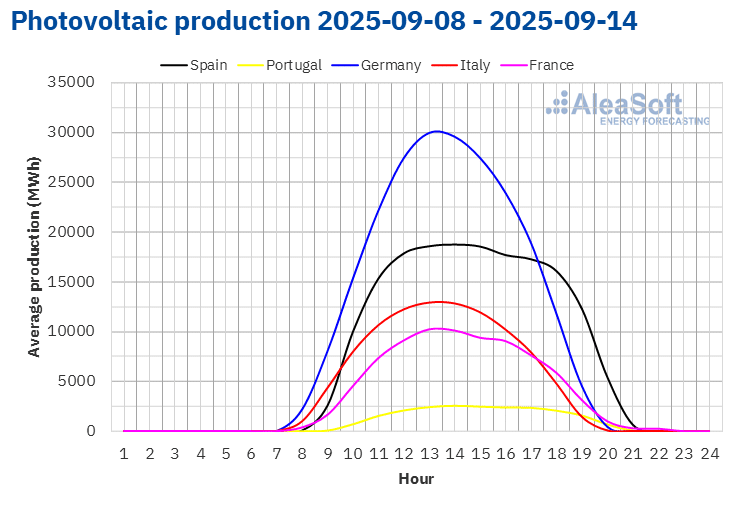

In the week of September 8, solar photovoltaic energy production increased in the Iberian markets compared to the previous week. The Portuguese market registered the largest rise, 13%, after two weeks of decreases. The Spanish market registered an increase of 2.3%, maintaining the upward trend for the second consecutive week. During the week, both Spain and Portugal reached all‑time highs in solar photovoltaic energy production for a day in September. Portugal registered its record on Tuesday, September 9, with 25 GWh, while Spain reached it on Friday, September 12, with 193 GWh.

However, in the French, German and Italian markets, solar photovoltaic energy generation decreased compared to the first week of September. France registered the smallest drop, 18%, while Italy and Germany decreased their production by 19% in both cases. Germany accumulated four consecutive weeks of declines.

For the week of September 15, AleaSoft Energy Forecasting’s solar energy forecasts anticipate increases in solar photovoltaic energy production in the German, Italian and Spanish markets.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA. Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.

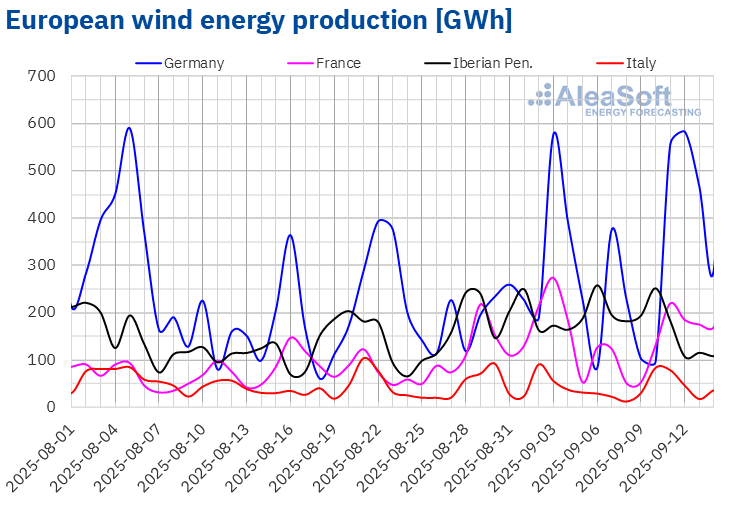

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.In the second week of September, wind energy production increased in most major European markets compared to the previous week. Portugal registered the largest rise, 14%, while Italy registered the smallest increase, 4.7%. Germany maintained the upward trend for the second consecutive week and increased its production by 12%. On the other hand, in the French and Spanish markets, generation with this technology decreased, interrupting the streak of increases of the previous two weeks in France and the previous three in Spain. France registered the smallest drop, 11%, while Spain decreased its production by 25%.

For the third week of September, AleaSoft Energy Forecasting’s wind energy forecasts anticipate an increase in the German market and declines in the French, Italian, Spanish and Portuguese markets.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.Electricity demand

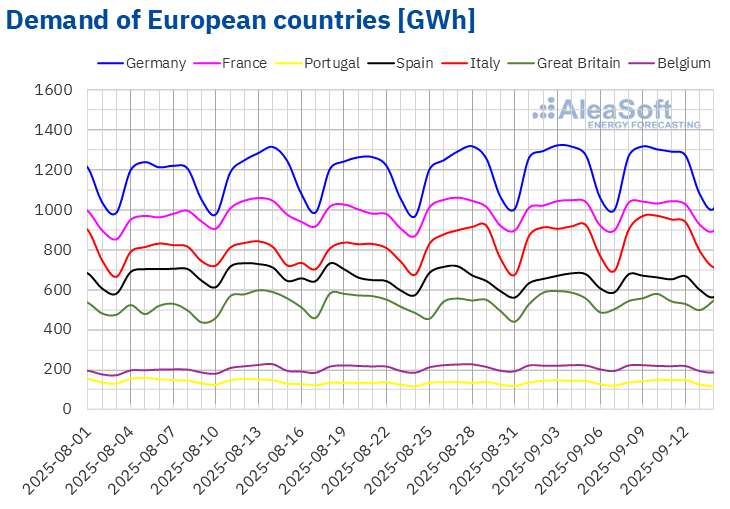

In the second week of September, electricity demand increased in most major European markets compared to the previous week. The Italian market registered the largest rise, 4.1%, chaining four weeks of growth. In the German, French and Portuguese markets, demand increased by 0.2%, 0.3% and 0.8%, respectively. Germany and Portugal extended the upward trend for the third consecutive week.

On the other hand, in the Spanish, British and Belgian markets, demand decreased compared to the first week of September. The Spanish market registered the smallest drop, 0.4%, maintaining the downward trend for the second consecutive week. In the British market, demand decreased by 1.1%. Belgium registered the largest decline, 1.4%, after six weeks of increases.

Average temperatures were lower than those of the previous week in most analyzed markets. Great Britain registered the largest drop, 2.4 °C, while the Iberian Peninsula registered the most moderate decreases, 0.1 °C in Portugal and 0.4 °C in Spain. France, Belgium and Germany registered declines of 1.3 °C, 1.6 °C and 1.7 °C, respectively. Italy maintained average temperatures similar to those of the previous week.

For the week of September 15, AleaSoft Energy Forecasting’s demand forecasts anticipate increases in demand in the British, Spanish and French markets, while the Italian, Portuguese, German and Belgian markets will register declines.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE, TERNA, National Grid and ELIA.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE, TERNA, National Grid and ELIA.European electricity markets

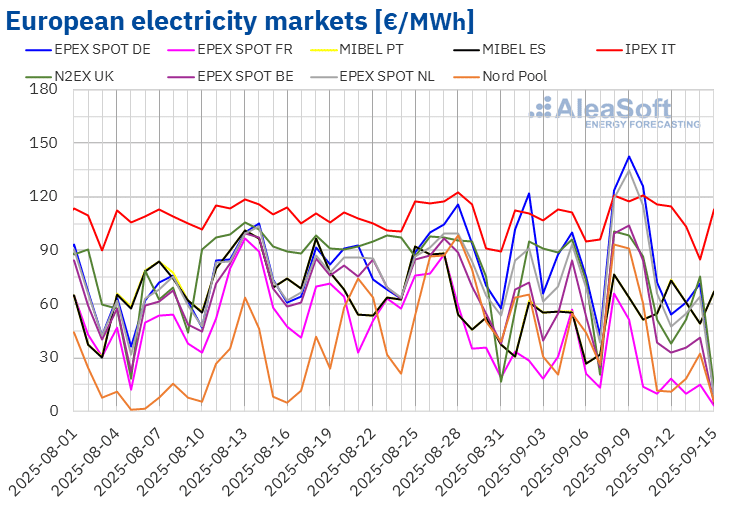

In the second week of September, average prices in most major European electricity markets increased compared to the previous week. The exceptions were the N2EX market of the United Kingdom and the EPEX SPOT market of France, whose averages fell by 3.8% and 8.5%, respectively. The IPEX market of Italy and the Nord Pool market of the Nordic countries registered the smallest price increases, both at 4.4%. In contrast, the MIBEL market of Portugal and Spain reached the largest percentage price increases, 35% and 36%, respectively. In the rest of the markets analyzed at AleaSoft Energy Forecasting, prices rose between 9.5% in the EPEX SPOT market of Germany and 19% in the EPEX SPOT market of the Netherlands.

In the week of September 8, weekly averages remained below €75/MWh in most European electricity markets, despite the price increases. The exceptions were the Dutch, German and Italian markets, with averages of €85.92/MWh, €92.99/MWh and €111.16/MWh, respectively. The French market registered the lowest weekly average, €26.36/MWh. In the rest of the markets analyzed at AleaSoft Energy Forecasting, prices were between €45.55/MWh in the Nordic market and €71.64/MWh in the British market.

As for daily prices, on Saturday, September 13, the French market reached the lowest average of the second week of September among the analyzed markets, €9.69/MWh. At the beginning of the third week of September, on Monday, September 15, most European electricity markets registered daily prices below €15/MWh. The French market registered the lowest price again, €3.38/MWh. This was the lowest price in the French market since June 9. On September 15, the Belgian, British and Dutch markets reached their lowest prices since May, while the German market registered its lowest price since January 2.

On the other hand, in the second week of September, the German, Belgian, British, Italian and Dutch markets registered daily prices above €100/MWh. On September 9, the German market reached the highest daily average of the week, €142.45/MWh. This was its highest price since February 18. In addition, on September 8, between 19:00 and 20:00, the German market registered a price of €413.66/MWh, the highest hourly value since July 1.

In the week of September 8, the rise in weekly gas and CO2 emission allowance prices, the drop in solar energy production and the increase in demand in most markets contributed to the increase in European electricity market prices. The fall in wind energy production on the Iberian Peninsula also contributed to the price increase in the MIBEL market.

AleaSoft Energy Forecasting’s price forecasts indicate that, in the third week of September, prices will fall in most European electricity markets, influenced by the increase in solar energy production and the decline in demand in some markets. In addition, wind energy production will rise significantly in Germany.

Source: Prepared by AleaSoft Energy Forecasting using data from OMIE, , Nord Pool and GME.

Source: Prepared by AleaSoft Energy Forecasting using data from OMIE, , Nord Pool and GME.Brent, fuels and CO2

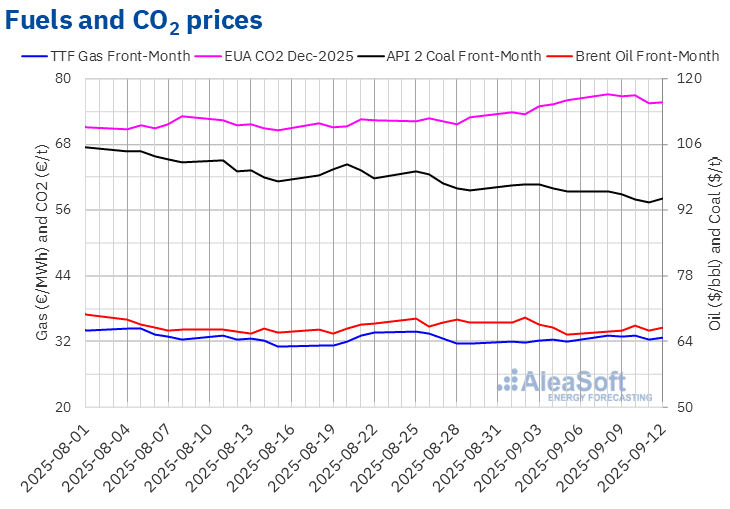

Brent oil futures for the Front‑Month in the ICE market registered their weekly minimum settlement price, $66.02/bbl, on Monday, September 8. This value exceeded that of the previous Friday and marked the start of a series of increases in the following sessions. As a result, on September 10 these futures registered their weekly maximum settlement price, $67.49/bbl. In the last sessions of the second week of September, prices remained below $67/bbl. On Friday, September 12, the settlement price was $66.99/bbl. According to data analyzed at AleaSoft Energy Forecasting, this price was 2.3% higher than the previous Friday.

The escalation of geopolitical tensions exerted upward pressure on Brent oil futures prices in the second week of September. However, concerns about demand evolution and production increases planned by OPEC+ limited the rises.

As for TTF gas futures in the ICE market for the Front‑Month, on Monday, September 8, the settlement price was €33.06/MWh, 3.4% higher than the last session of the previous week. On September 10, these futures registered their weekly maximum settlement price, €33.12/MWh. In contrast, on Thursday, September 11, after a 2.4% drop compared to the previous day, they registered their weekly minimum settlement price, €32.32/MWh. On Friday, September 12, the settlement price was €32.66/MWh. According to data analyzed at AleaSoft Energy Forecasting, this price was 2.2% higher than the previous Friday.

In the second week of September, TTF gas futures prices remained above €32/MWh, influenced by rising tensions in the Middle East, as well as between Russia and Ukraine. However, European reserve levels, close to 80%, and the completion of maintenance work in Norway helped prevent prices from reaching €34/MWh.

Regarding CO2 emission allowance futures in the EEX market for the reference contract of December 2025, settlement prices remained above €75/t during the second week of September. On Monday, September 8, they registered their weekly maximum settlement price, €77.16/t. According to data analyzed at AleaSoft Energy Forecasting, this was the highest price since February 18. In contrast, on Thursday, September 11, these futures registered their weekly minimum settlement price, €75.55/t. On Friday, September 12, the price was slightly higher, €75.78/t. This price was 0.3% lower than the previous Friday.

Source: Prepared by AleaSoft Energy Forecasting using data from ICE and EEX.

Source: Prepared by AleaSoft Energy Forecasting using data from ICE and EEX.AleaSoft Energy Forecasting’s analysis on the prospects for energy markets in Europe, batteries and self‑consumption

The 58th webinar in the monthly webinar series of AleaSoft Energy Forecasting will take place on Thursday, September 18. In addition to the evolution of European energy markets, the webinar will analyze the prospects for battery energy storage and self‑consumption. During the webinar, there will also be a presentation of AleaSoft services to improve the strategy, management and planning of retailers.

The analysis table of the webinar in Spanish will feature the participation of Xavier Cugat, BESS Technical Director at Seraphim, Francisco Valverde, independent professional for the renewable energy development, and Alejandro Diego Rosell, energy communicator and consultant, Director of Studies at World Wide Recruitment and Lecturer at EOI.

Source: AleaSoft Energy Forecasting.