AleaSoft, September 30, 2020. On October 1, the new hydrological year 2020‑2021 begins and the 2019‑2020 closes definitively, characterised by a recovery in hydroelectric energy production. This new cycle begins with a relatively optimistic autumn for most European electricity markets with the notable exception of the peninsulas in the south of the continent, where the autumn is expected to be especially dry.

The hydroelectric energy production in the hydrological year 2019‑2020

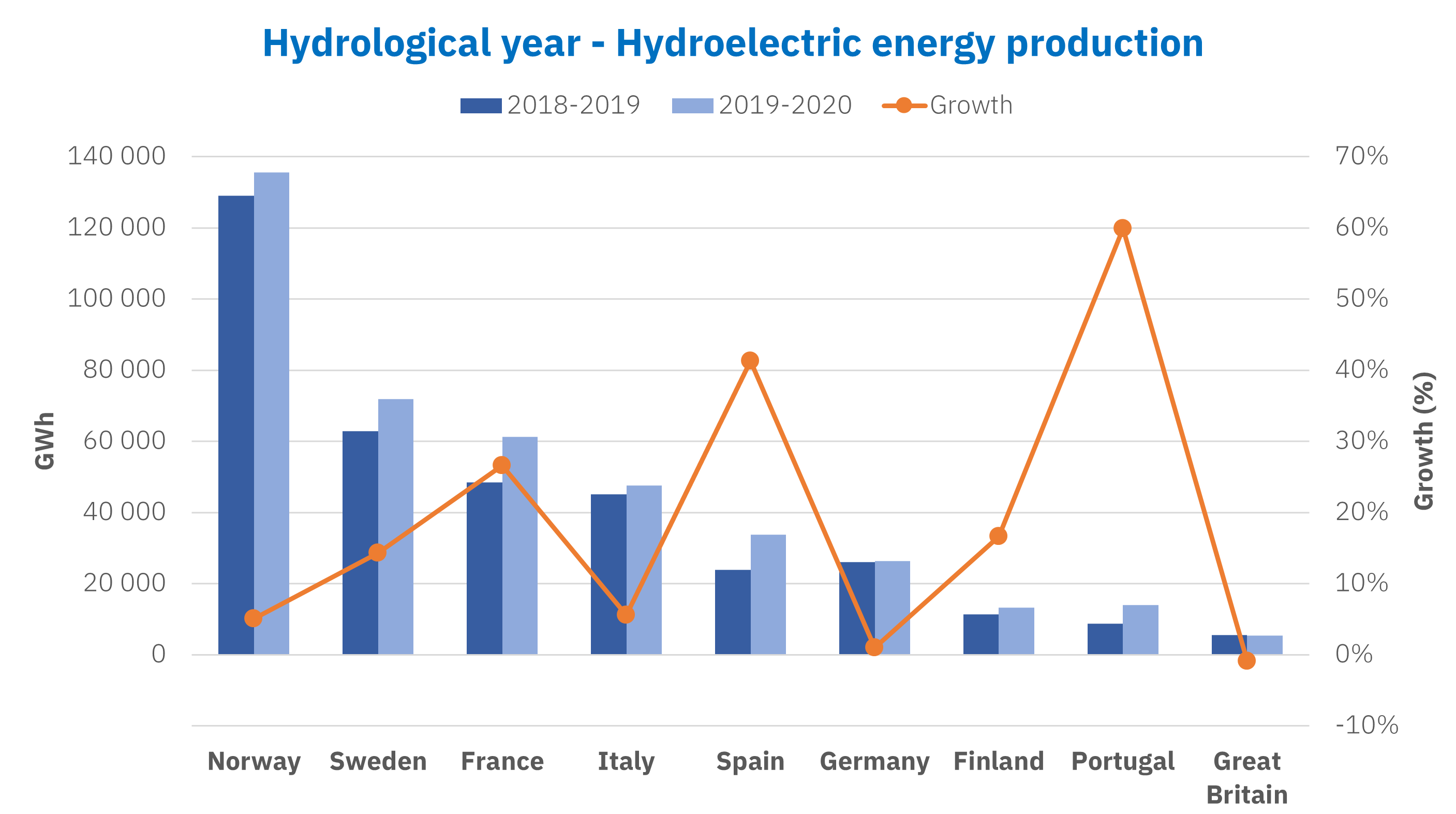

The hydrological year that is ending, which has elapsed from October 1, 2019 to September 30, 2020, has meant a recovery in hydroelectric energy production in the vast majority of the European electricity markets compared to the previous hydrological year, 2018‑2019.

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA.

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA.The increase in hydroelectric energy production in the Iberian Peninsula, of 60% in Portugal and 41% in Spain, stands out, followed by France with an increase of 27%. At the other extreme we find Germany, with an increase in production with this technology of only 1%, and Great Britain, with a drop of 1%.

The impact on the electricity markets price

The hydroelectric energy production is one of the factors with the greatest impact on the electricity markets prices. However, the consequences of the COVID‑19 pandemic on the energy demand and the gas and oil prices masked the depressor effect of the rise in hydroelectric energy on the electricity markets prices.

In many of the main European markets, the average price of this hydrological year was the lowest in the last “hydrological decade”, that is, in the last ten hydrological years. These markets include the Iberian MIBEL, the French and Belgian EPEX SPOT, the Italian IPEX, the British N2EX and the Nord Pool of the Nordic countries.

The autumn that awaits us

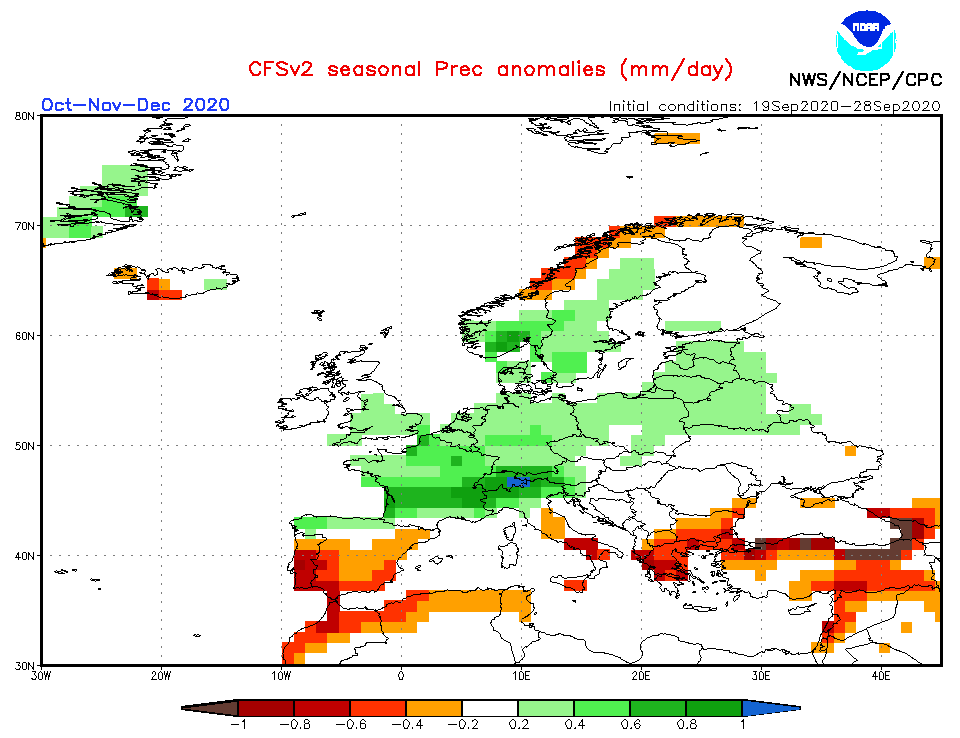

The seasonal forecasting indicates that, the hydrological year that begins, it will do so with a relatively rainy autumn in Europe. In the largest part of the centre and the north of the continent and of the British Isles, the rainfall is expected to be above the historical average for this time of year. The clear exceptions are the southernmost peninsulas of the continent: the Greek, the Italic and the Iberian.

Source: Climate Prediction Center de la NOAA.

Source: Climate Prediction Center de la NOAA.The State Meteorological Agency in Spain (AEMET) forecasts an autumn, from October to December, drier than usual with a probability of 50%, compared to probabilities of 30% and 20% that it will be normal or rainy, respectively. The exception would be the Mediterranean coast, where the probability of a dry autumn would be slightly lower, of 40% versus 35% and 25% for a normal or wet season, respectively. The temperature forecasting points to a little extreme autumn with values higher than the historical average for this season of the year.

This autumn the hydroelectric energy production will modulate the recovery of the prices in the European markets, pushing the prices up in the Iberian, Italian and Greek markets, and pushing down the markets of the centre and north of the continent. In any case, the recovery of the economy in each of these countries will also have a very important impact on the pace of the price recovery.

AleaSoft analysis of the recovery of the energy markets at the end of the economic crisis

The recovery of the prices in the electricity markets, and the energy markets in general, and how this affects the financing of the renewable energy projects are some of the topics that will be discussed in the second part of the webinar “Energy markets in the recovery from the economic crisis” that is being organised at AleaSoft and that will take place on October 29. The webinar will also analyse the uncertainty that exists about when and how the recovery from the economic crisis will happen and the importance of the forecasting in the audits and the portfolio valuation. On this occasion, there will be the presence of two invited speakers from the consulting firm Deloitte, Pablo Castillo Lekuona, Senior Manager of Global IFRS & Offerings Services and Carlos Milans del Bosch, Partner of Financial Advisory.

This will be the second part of a series of webinars on the recovery of the markets, the recording of the first part of the webinar is available at webinar@aleasoft.com.

To follow the evolution of the energy markets, the energy markets observatories are also available on the AleaSoft website, a tool that allows monitoring the main European electricity, fuels and CO2 markets with daily updated data. The observatories include comparative graphs for the last weeks, with hourly, daily and weekly information.

Coinciding with the beginning of the hydrological year, at AleaSoft the 21st anniversary of the creation of the company is celebrated. 21 years of experience providing customers with reliable forecasting of the energy markets in Europe.

Source: AleaSoft Energy Forecasting.