AleaSoft Energy Forecasting, December 1, 2025. In the last week of November, weekly prices remained above €95/MWh in most major European electricity markets, with exceptions in the Iberian, French and Nordic markets. In addition, several markets reached the highest daily levels of recent months. Wind energy production increased in most markets, while photovoltaic energy production declined. On November 28, TTF gas futures reached the lowest settlement price since May 2024 and CO2 futures reached the highest since early February.

Solar photovoltaic and wind energy production

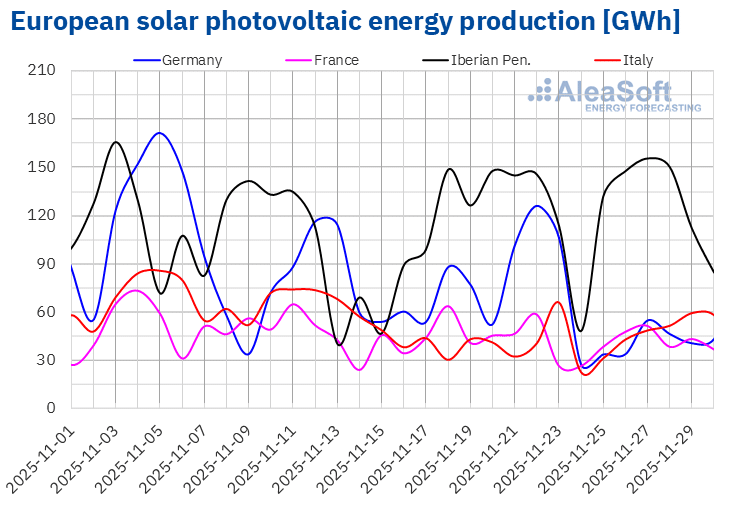

In the week of November 24, solar photovoltaic energy production decreased in most major European electricity markets compared to the previous week. The German market registered the largest decrease, 54%. The French and Spanish markets followed it, with decreases of 13% and 10%, respectively. The Portuguese market registered the smallest decline, 8.0%. The Italian market was the exception, reversing the negative trend of the previous two weeks with a 5.7% increase in solar energy production. All markets reversed the previous week’s trend, as it had been upward for Germany, France, Portugal and Spain and downward for Italy.

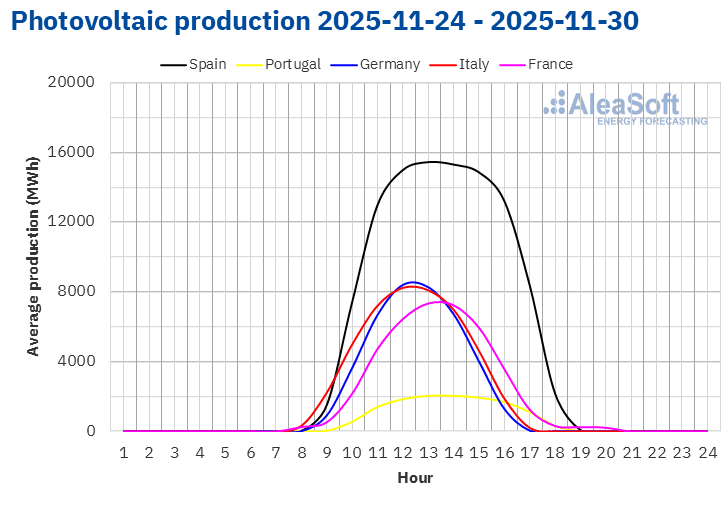

On the 24th, production fell in all analyzed markets, marking the lowest solar energy production day of the month for Germany and Italy. Even so, the month of November ended as a record month for photovoltaic energy production compared to the same period in previous years in the main markets.

During the week of December 1, according to AleaSoft Energy Forecasting’s solar energy forecasts, the downward trend will continue in Spain. In Italy, production from this technology will also fall, while in Germany production will increase.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA. Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.

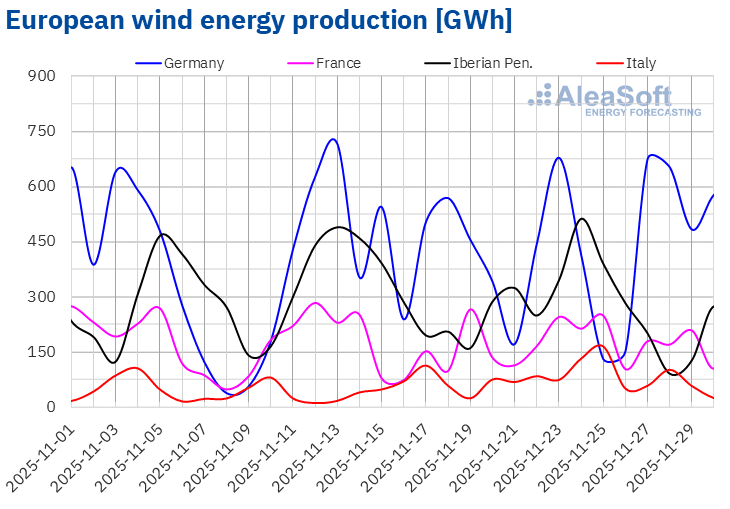

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.During the week of November 24, wind energy production increased in most major European markets compared to the previous week. The Portuguese market registered the largest rise, 22%. The Italian, Spanish and French markets followed it with week‑on‑week increases of 19% and 4.0% for the last two markets, respectively. In contrast, the German market registered a 2.5% decrease.

On the 24th and 25th, unlike solar energy production, wind energy production was high, with those days becoming the highest‑production days of the month for Spain and Italy, respectively. Germany was the exception, registering its second‑lowest monthly level on the 25th. November wind energy production increased in almost all major European markets compared to the same period of the previous year, except in Portugal.

In the week of December 1, according to AleaSoft Energy Forecasting’s wind energy forecasts, the upward trend will continue in the Iberian markets, but will reverse with declines in the French and Italian markets, while Germany will register its second consecutive week of decreases.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.Electricity demand

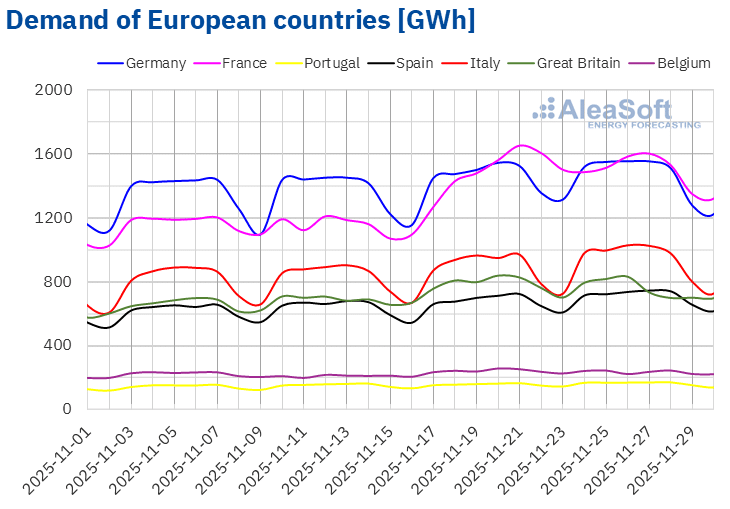

In the week of November 24, electricity demand increased in the main European markets located further south and decreased in those further north. In the Italian, Spanish and Portuguese markets, demand rose by 5.3%, 4.3% and 4.0%, respectively. In the British and Belgian markets, declines were 3.9% and 3.2%. France and Germany were in an intermediate situation, with France registering a 1.1% drop in demand and Germany a 0.2% increase. These declines reversed the upward trend observed in all markets the previous week.

During the week, average temperatures were milder than the previous week in all analyzed markets except Italy. The largest temperature increases occurred in northern markets, with rises of around 3.0 °C in Germany, Belgium and the United Kingdom. In contrast, in Spain and Portugal increases were 0.2 °C and 0.4 °C, respectively. Finally, Italy registered a decrease in average temperatures of 2.0 °C.

For the week of December 1, according to AleaSoft Energy Forecasting’s demand forecasts, demand will increase in the Belgian, British and Italian markets. Conversely, demand will fall in the German, French, Spanish and Portuguese markets.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE, TERNA, National Grid and ELIA.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE, TERNA, National Grid and ELIA.European electricity markets

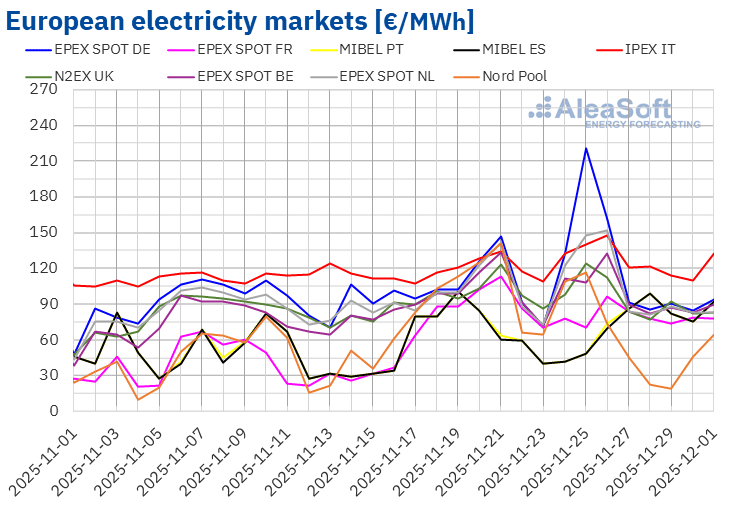

In the fourth week of November, prices in most major European electricity markets remained at similar levels to the previous week, with the highest values registered in the first days of the week. In many markets, the weekly average fell slightly compared to the previous week. The exceptions were the IPEX market of Italy and the EPEX SPOT market of the Netherlands and Germany, which registered increases of 6.4%, 6.8% and 18% respectively. In the MIBEL market of Portugal and Spain, price variations were minimal, with declines of only 0.05% in Portugal and 0.2% in Spain. In contrast, the Nord Pool market of the Nordic countries registered the largest percentage price drop, 38%. In the remaining markets analyzed at AleaSoft Energy Forecasting, prices fell between 1.1% in the EPEX SPOT market of Belgium and 8.5% in the EPEX SPOT market of France.

In the week of November 24, weekly averages remained above €95/MWh in most European electricity markets. Exceptions were the Nordic, Spanish, Portuguese and French markets, with averages of €61.63/MWh, €71.58/MWh, €72.22/MWh and €79.77/MWh, respectively. Italy reached the highest weekly average, €126.63/MWh. In the remaining markets analyzed at AleaSoft Energy Forecasting, prices ranged from €95.49/MWh in the N2EX market of the United Kingdom to €123.57/MWh in the German market.

Regarding daily prices, the Nordic market registered the lowest average of the week among analyzed markets, €19.19/MWh, on Saturday, November 29. Spain and Portugal also registered prices below €50/MWh in the early sessions of the fourth week of November, while daily prices remained above €65/MWh in the rest of the markets.

Most markets analyzed at AleaSoft Energy Forecasting registered prices above €100/MWh in some sessions of the fourth week of November, except the Spanish, French and Portuguese markets. In Italy, daily prices exceeded €110/MWh throughout the entire week. However, Germany reached the highest daily average of the week, €220.52/MWh, on Tuesday, November 25, its highest price since January 21. On November 26, the Italian and Dutch markets registered their highest prices since the second half of February, €147.32/MWh and €151.69/MWh, respectively. The British market registered a price of €124.29/MWh on November 25, matching the average reached on March 13.

In the week of November 24, the increase in wind energy production in the Iberian Peninsula and France helped to keep weekly averages below €80/MWh in these markets. In France, falling demand also contributed to lower prices, which was also the case in the Belgian and British markets. Conversely, rising demand in Germany and Italy drove prices higher. The drop in both solar and wind energy production in Germany contributed to this market registering the highest percentage price increase.

AleaSoft Energy Forecasting’s price forecasts indicate that in the first week of December, prices will fall in most major European electricity markets, influenced by lower demand in some markets. The increase in wind energy production in the Iberian Peninsula and the rise in solar energy production in Germany could contribute to price declines in the German, Spanish and Portuguese markets. In contrast, falling wind energy production in France and Italy will support price increases in those markets.

Source: Prepared by AleaSoft Energy Forecasting using data from OMIE, , Nord Pool and GME.

Source: Prepared by AleaSoft Energy Forecasting using data from OMIE, , Nord Pool and GME.Brent, fuels and CO2

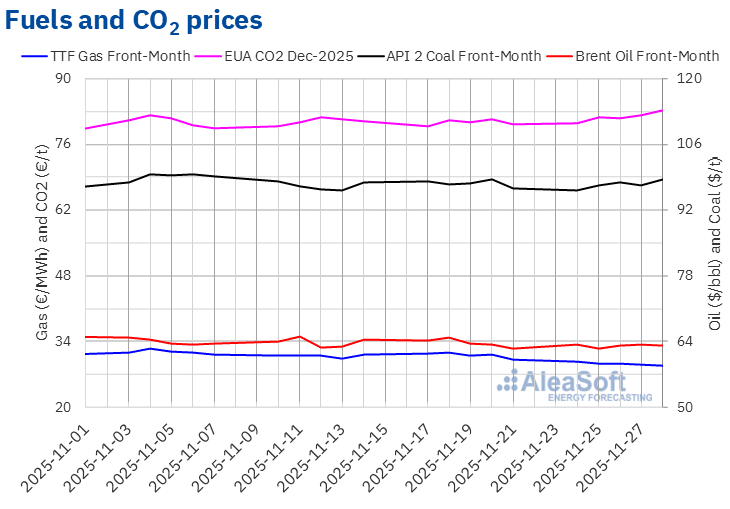

Brent oil futures for the Front‑Month in the ICE market reached their weekly maximum settlement price, $63.37/bbl, on Monday, November 24. After a 1.4% drop compared to the previous day, on Tuesday, November 25, these futures registered their weekly minimum settlement price, $62.48/bbl. According to data analyzed at AleaSoft Energy Forecasting, this was the lowest price since October 22. In the last three sessions of the week, settlement prices remained above $63/bbl. On Friday, November 28, the settlement price was $63.20/bbl, 1.0% higher than the previous Friday.

During the fourth week of November, peace talks for Ukraine continued to exert downward pressure on Brent oil futures prices. Global oil supply could increase if sanctions on Russia were lifted. Expectations surrounding the OPEC+ meeting also influenced price developments. On Sunday, November 30, OPEC+ decided to maintain its plan to pause production increases during the first quarter of 2026.

As for TTF gas futures in the ICE market for the Front‑Month, during the fourth week of November they continued the downward trend that began at the end of the previous week. On Monday, November 25, these futures reached their weekly maximum settlement price, €29.75/MWh. In contrast, as a result of the fall in prices, on Friday, November 28, these futures registered their weekly minimum settlement price, €28.82/MWh. According to data analyzed at AleaSoft Energy Forecasting, this price was 4.6% lower than the previous Friday and the lowest since May 2, 2024.

Negotiations to reach a peace agreement for Ukraine exerted downward pressure on TTF gas futures prices in the fourth week of November. High supply levels and forecasts for milder temperatures in the first half of December also helped keep prices below €30/MWh during the fourth week of November.

Regarding CO2 emission allowance futures in the EEX market for the reference contract of December 2025, on Monday, November 24, they registered their weekly minimum settlement price, €80.60/t. In most sessions of the fourth week of November, prices increased. As a result, on Friday, November 28, these futures reached their weekly maximum settlement price, €83.25/t. According to data analyzed at AleaSoft Energy Forecasting, this price was 3.5% higher than the previous Friday and the highest since February 1.

Source: Prepared by AleaSoft Energy Forecasting using data from ICE and EEX.

Source: Prepared by AleaSoft Energy Forecasting using data from ICE and EEX.AleaSoft Energy Forecasting’s analysis on the progress and prospects of the five‑year period of batteries

The 61st edition of the monthly webinar series of AleaSoft Energy Forecasting will take place on Thursday, December 4. This webinar will focus on the balance of the first year of the five‑year period of batteries, the prospects for the next years of the five‑year period and the strategic vectors of the energy transition, such as renewable energy, demand, grids and energy storage. On this occasion, the webinar in Spanish will feature Antonio Hernández García, Partner of Regulated Sectors at EY, Jaume Pujol Benet, Partner, Financial Advisory at Deloitte, and Oscar Barrero Gil, Partner responsible for the Energy Sector at PwC.

Source: AleaSoft Energy Forecasting.