AleaSoft Energy Forecasting, February 16, 2026. In the second week of February, prices in most major European electricity markets followed a downward trend, although in many cases the weekly average was above €90/MWh. The Nordic market registered the highest weekly average, something unprecedented since at least 2018, and on February 10 it reached its highest price since 2022. The Iberian market remained decoupled from the rest of Europe, with daily prices below €5/MWh in most sessions. Regarding renewable energy production, the Italian market set the highest photovoltaic energy production for a February day and the French market registered the highest wind energy production for a February day. Meanwhile, CO₂ futures fell to their lowest level since May 2025.

Solar photovoltaic and wind energy production

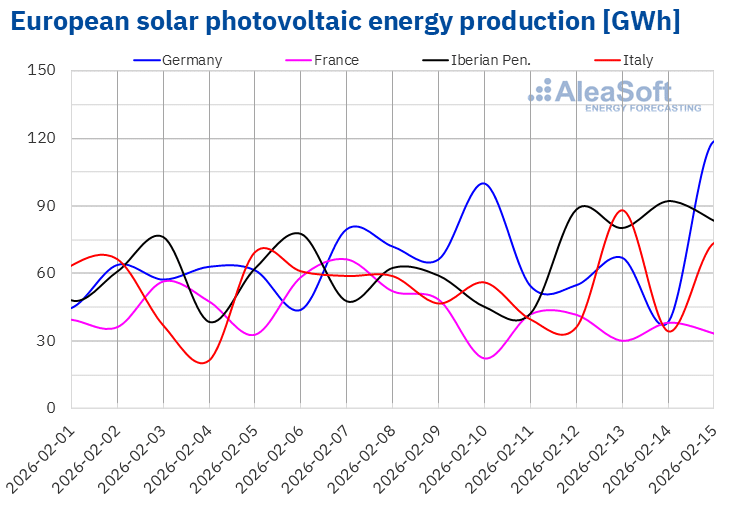

In the week of February 9, solar photovoltaic energy production increased in most major European electricity markets compared to the previous week. The Spanish market registered the largest increase, 16%, and extended the upward trend from the previous week. The German market rose for a second consecutive week, this time by 13%. In Portugal, photovoltaic energy production also increased for a second week, by 5.0%. The Italian market registered the smallest increase, 0.4%, and continued the positive trend of the last two weeks. In contrast, in the French market, production from this technology fell by 27% after three weeks of increases.

The Italian market set a new all‑time high for photovoltaic energy production for a February day, generating 89 GWh on Friday, February 13.

During the week of February 16, according to AleaSoft Energy Forecasting’s solar energy forecasts, production will increase in the German, Italian and Spanish markets.

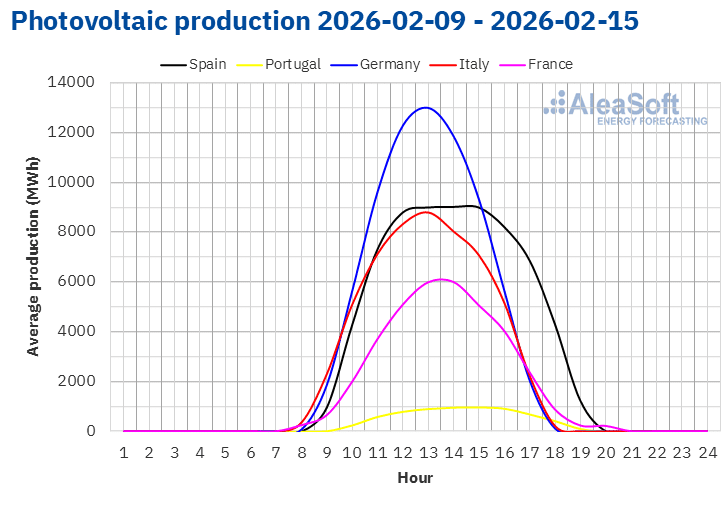

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica and TERNA.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica and TERNA. Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica and TERNA.

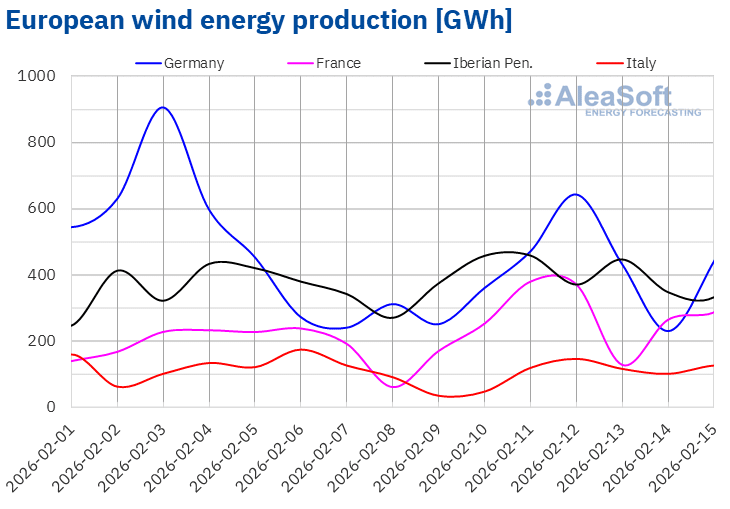

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica and TERNA.During the week of February 9, the French market again registered the largest increase in wind energy production compared to the previous week, for the second consecutive week, with a rise of 38%. The Spanish and Portuguese markets reversed the previous week’s downward trend, increasing by 8.6% and 6.0%, respectively. By contrast, the German and Italian markets showed the opposite trend. In Germany, wind energy production fell by 17% and continued the previous week’s decline, while in Italy it dropped by 15% after three consecutive weeks of increases.

The French market set a new all-time high for wind energy production for a February day on the 11th, generating 380 GWh.

In the week of February 16, according to AleaSoft Energy Forecasting’s wind energy forecasts, production from this technology will increase in the Italian and German markets, while it will decrease in the Portuguese, Spanish and French markets.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica and TERNA.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica and TERNA.Electricity demand

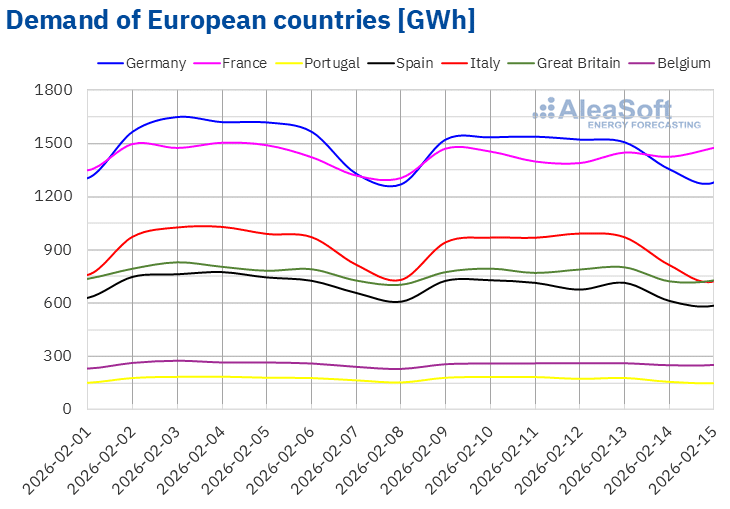

In the week of February 9, electricity demand decreased in most major European markets compared to the previous week. The Spanish market registered the largest drop, 5.2%, and extended its decline for a third consecutive week. In Germany, Italy and Great Britain, demand fell for a second consecutive week by 3.4%, 2.4% and 0.9%, respectively. The Portuguese market reversed the previous week’s upward trend with a 1.6% decline. Demand in Belgium stayed similar to the previous week, while French demand rose by 0.5% and reversed the previous week’s decline.

Less cold average temperatures in most analyzed markets drove the demand decrease. Temperatures rose between 0.5 °C in France and 2.5 °C in Germany. However, average temperatures fell 0.1 °C in Great Britain and 1.6 °C in Belgium.

For the week of February 16, AleaSoft Energy Forecasting’s demand forecasts indicate increases in Germany, France, Spain, Great Britain and Belgium, while Portugal and Italy will show declines.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica, TERNA, National Grid and ELIA.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica, TERNA, National Grid and ELIA.European electricity markets

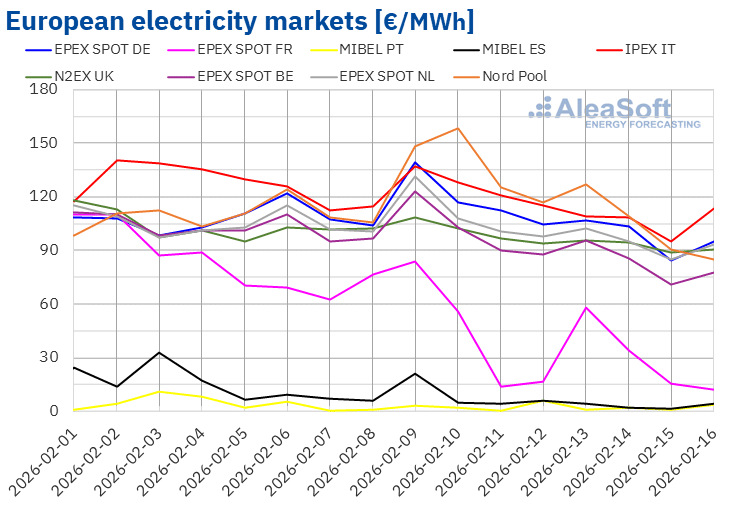

During the second week of February, prices in most major European electricity markets showed a downward trend. As a result, weekly average prices dropped in most markets compared to the previous week. The exceptions were the EPEX SPOT market of Germany and the Nord Pool market of the Nordic countries, which rose 1.9% and 13%, respectively. The EPEX SPOT market of the Netherlands registered the smallest decrease, 0.9%. By contrast, the EPEX SPOT market of France and the MIBEL market of Portugal and Spain registered the largest percentage price drops, 51%, 52% and 53%, respectively. In the remaining markets analyzed at AleaSoft Energy Forecasting, prices fell between 4.6% in the N2EX market of the United Kingdom and 9.3% in the IPEX market of Italy.

In the week of February 9, despite price decreases, weekly averages exceeded €90/MWh in most European electricity markets. The exceptions were Portugal, Spain and France, with averages of €2.18/MWh, €6.24/MWh and €39.60/MWh, respectively. In contrast, the Nordic market registered the highest weekly average, €125.08/MWh. In the rest of the markets analyzed at AleaSoft Energy Forecasting, prices ranged between €93.62/MWh in Belgium and €116.21/MWh in Italy.

Regarding daily prices, Spain and Portugal registered prices below €5/MWh in most sessions of the second week of February. On February 11, Portugal registered the lowest average of the week among the analyzed markets, €0.34/MWh. This was its lowest daily price since April 6, 2024. On February 15, Spain reached its lowest price since April 17, 2024, €1.55/MWh. In France, prices fell below €20/MWh in some sessions of the second week of February. On February 11, the price was €13.61/MWh, the lowest in this market since October 24, 2025. In the third week of February, on Monday, the 16th, the price was even lower, €12.13/MWh, although it remained above the price registered on October 23, 2025.

On the other hand, the German, Belgian, British, Italian, Dutch and Nordic markets registered daily prices above €100/MWh in some sessions of the second week of February. In Italian and the Nordic markets, daily prices exceeded €120/MWh during the first three days of the week. The Nordic market reached the highest daily average of the week among the analyzed markets, €158.53/MWh, on Tuesday, February 10. This was its highest daily price since December 23, 2022.

In the week of February 9, falling gas and CO₂ allowance prices, rising solar energy production and lower demand in most markets contributed to the decline in European electricity market prices. In the Iberian Peninsula, high hydroelectric energy production also pushed prices downward, while increased wind energy production in Spain, France and Portugal further contributed to the price decline.

AleaSoft Energy Forecasting’s price forecasts indicate that prices will fall in most major European electricity markets in the third week of February. A notable increase in wind and solar energy production in markets such as Germany and Italy will drive this behavior. However, higher demand and lower wind energy production in the Iberian Peninsula will push prices upward in the MIBEL market.

Source: Prepared by AleaSoft Energy Forecasting using data from OMIE, , Nord Pool and GME.

Source: Prepared by AleaSoft Energy Forecasting using data from OMIE, , Nord Pool and GME.Brent, fuels and CO2

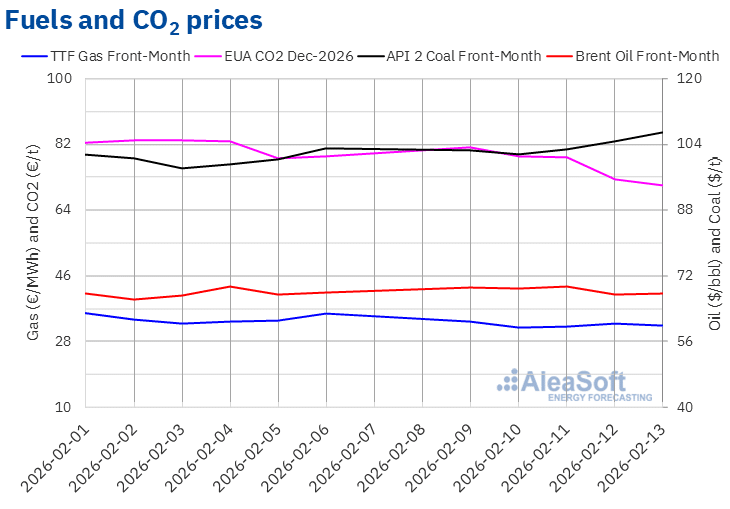

During the second week of February, settlement prices of Brent oil futures for the Front‑Month in the ICE market remained below $70/bbl. On February 11, these futures reached their weekly maximum settlement price, $69.40/bbl. However, after a 2.7% drop from the previous day, on Thursday, February 12, they registered their weekly minimum settlement price, $67.52/bbl. On Friday, February 13, the settlement price rose slightly to $67.75/bbl. According to data analyzed at AleaSoft Energy Forecasting, this price was still 0.4% lower than the previous Friday.

Tensions in the Middle East kept Brent oil futures prices above $68.75/bbl early in the week, but demand concerns limited prices. The International Energy Agency released its monthly report on Thursday, warning about a possible oversupply in 2026 and lowering its oil demand forecasts. Meanwhile, the US president stated negotiations with Iran could last a month, reducing supply fears and adding downward pressure on prices.

As for settlement prices of TTF gas futures in the ICE market for the Front‑Month, they remained stable below €34/MWh during the second week of February. On Monday, February 9, these futures reached their weekly maximum settlement price, €33.50/MWh. This price was already 6.2% lower than the previous Friday. On Tuesday, February 10, they registered their weekly minimum settlement price, €31.85/MWh. During the rest of the week, settlement prices stayed above €32/MWh. On Friday, February 13, the settlement price was €32.50/MWh. According to data analyzed at AleaSoft Energy Forecasting, this price was 8.9% lower than the previous Friday.

Forecasts of milder temperatures exerted downward pressure on TTF gas futures prices in the second week of February. In addition, increased availability of liquefied natural gas from the United States, associated with forecasts of higher temperatures in that country as well, contributed to prices remaining below €34/MWh during the second week of February.

Regarding CO2 emission allowance futures in the EEX market for the reference contract of December 2026, on Monday, February 9, they reached their weekly maximum settlement price, €81.33/t. Prices then moved downward and on Friday, February 13, they reached their weekly minimum settlement price, €70.70/t. According to data analyzed at AleaSoft Energy Forecasting, this price was 10% lower than the previous Friday and the lowest since May 6, 2025.

Source: Prepared by AleaSoft Energy Forecasting using data from ICE and EEX.

Source: Prepared by AleaSoft Energy Forecasting using data from ICE and EEX.AleaSoft Energy Forecasting’s analysis on the prospects for energy markets in Europe and battery storage

On Thursday, February 12, AleaSoft Energy Forecasting held its 63rd monthly webinar. The guest speaker was Tomás García, Senior Director, Energy & Infrastructure Advisory at JLL, who participated for the fifth time in AleaSoft Energy Forecasting’s monthly webinar series. The February webinar analyzed relevant energy sector topics including the evolution and prospects of European energy markets, insights from recent BESS transactions in Spain and the key valuation drivers for stand‑alone BESS projects in Spain.

Source: AleaSoft Energy Forecasting.