AleaSoft Energy Forecasting, February 23, 2026. In the third week of February, prices in most major European markets declined, except in the Iberian market where they recovered compared to the previous week, although they remained among the lowest in Europe. Most markets registered their lowest daily prices since the beginning of the year. Photovoltaic energy production increased and, in Italy, wind and solar energy production set new records for a February day. Electricity demand decreased in most markets. Gas and CO2 futures reached their lowest settlement prices since January 2026 and May 2025, respectively, while Brent futures reached their highest level since July.

Solar photovoltaic and wind energy production

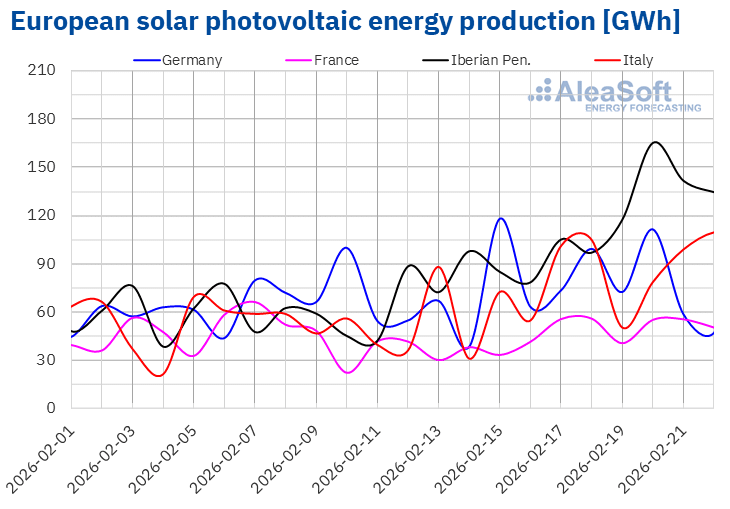

In the week of February 16, solar photovoltaic energy production increased in the main European markets compared to the previous week. The Portuguese market registered the largest increase, 95%, marking its third consecutive week of growth. In the Spanish market, photovoltaic energy production also grew for the third consecutive week, rising 69% this time. In the Italian market, production climbed 62%, extending its upward streak to four weeks. The French market increased 39%, reversing the previous week’s downward trend. The German market registered the smallest increase, 5.4%.

The Italian market set a new all‑time high for solar photovoltaic energy production in a February day on Sunday, February 22, reaching 110 GWh.

During the week of February 23, according to AleaSoft Energy Forecasting’s solar energy forecasts, production will increase in the German, Italian and Spanish markets.

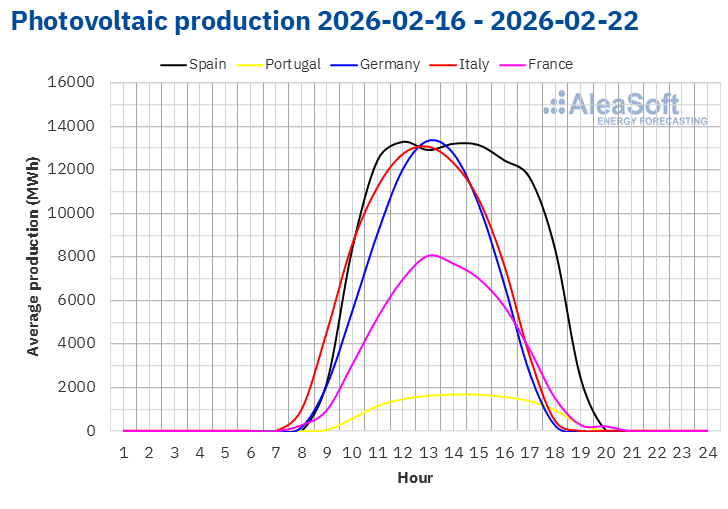

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica and TERNA.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica and TERNA. Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica and TERNA.

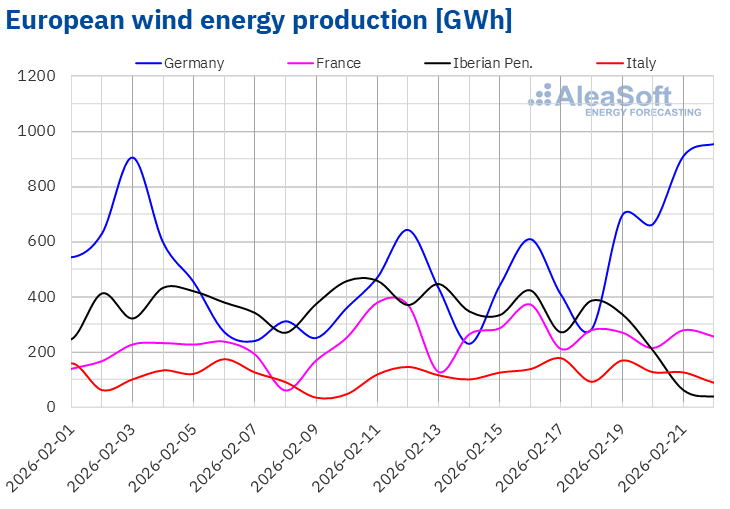

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica and TERNA.During the week of February 16, wind energy production increased 60% in the German market, after two weeks of declines. In the Italian market, production rose 33%, reversing the previous week’s downward trend. In the French market, wind energy production increased for the third consecutive week, although it showed the smallest growth, 1.7%. In contrast, wind energy production decreased in the Iberian Peninsula, falling 56% in Portugal and 33% in Spain.

On Tuesday, February 17, the Italian market set a new all‑time high for wind energy production in a February day, reaching 178 GWh.

In the week of February 23, according to AleaSoft Energy Forecasting’s wind energy forecasts, production from this technology will decrease in the main European markets.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica and TERNA.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica and TERNA.Electricity demand

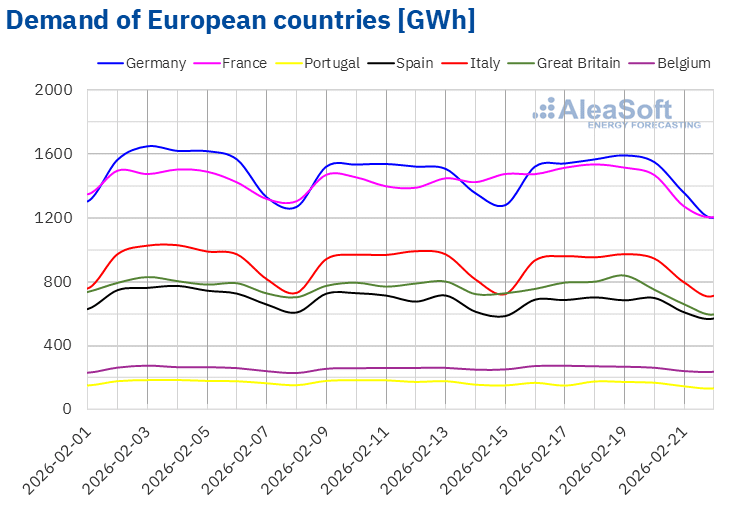

In the week of February 16, electricity demand decreased in most major European electricity markets compared to the previous week. The Portuguese market registered the largest drop, 7.7%, marking its second consecutive week of declines. The Carnival Tuesday holiday on February 17 supported this decrease in demand. The British, Spanish and Italian markets followed, with declines of 3.4%, 2.5% and 1.7%, respectively. The French market reversed the previous week’s upward trend and registered a decrease of 0.8%. In contrast, demand increased 1.5% in the Belgian market and 0.7% in the German market, after two weeks of declines in the latter.

At the same time, average temperatures were milder than the previous week in Great Britain, France and Belgium, with increases ranging from 0.2 °C in Great Britain to 0.7 °C in Belgium. Meanwhile, average temperatures decreased in Portugal, Germany, Italy and Spain, with drops ranging from 0.6 °C in Portugal to 1.0 °C in Spain.

For the week of February 23, according to AleaSoft Energy Forecasting’s demand forecasts, demand will decrease in the German, French, Italian, British and Belgian markets. In contrast, Spain and Portugal will register an increase.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica, TERNA, National Grid and ELIA.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica, TERNA, National Grid and ELIA.European electricity markets

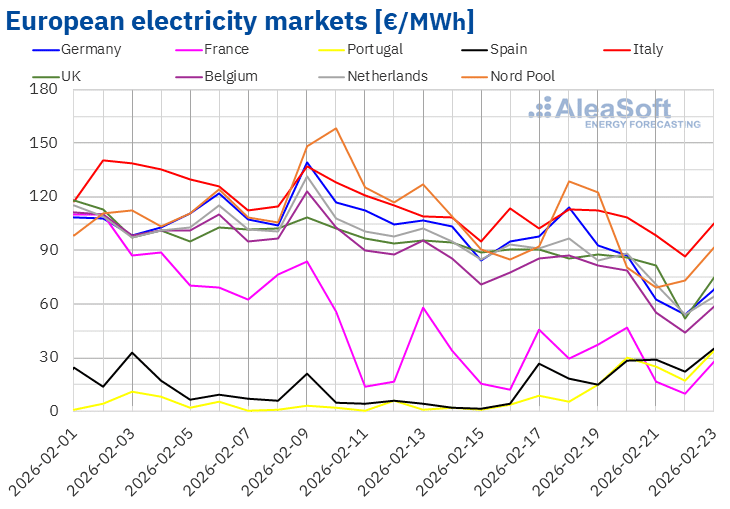

Prices in most major European electricity markets rebounded slightly in the first days of the third week of February but declined again in the second half of the week. As a result, weekly average prices in most markets fell compared to the previous week. The Iberian market stood as the exception, with increases of 230% in Spain and 581% in Portugal. The Italian market registered the smallest decline, 9.8%. In contrast, the Nordic and French markets registered the largest percentage price drops, 26% and 28%, respectively. In the rest of the markets analyzed at AleaSoft Energy Forecasting, prices fell between 16% in the United Kingdom and 22% in the Belgian market.

In the week of February 16, weekly averages stayed below €90/MWh in most European electricity markets. The Nordic and Italian markets stood as exceptions, with averages of €93.02/MWh and €104.82/MWh, respectively. The Portuguese, Spanish and French markets registered the lowest weekly averages, €14.86/MWh, €20.57/MWh and €28.32/MWh, respectively. In the remaining markets analyzed at AleaSoft Energy Forecasting, prices ranged from €72.82/MWh in the Belgian market to €86.13/MWh in the German market.

Regarding daily prices, on Monday, February 16, the Portuguese market reached the lowest average of the week among the analyzed markets, €3.50/MWh. That same day, the Spanish market also registered a price below €5/MWh. On Sunday, February 22, the French market reached €9.56/MWh, its lowest daily price since October 6, 2025. On February 22, the Italian market reached €86.34/MWh, its lowest price since October 27, 2025. In the Belgian market, the price was €43.92/MWh on February 22, the lowest in this market since November 2, 2025. On Sunday, the German, British and Dutch markets registered their lowest prices since January 2, €53.86/MWh, €51.84/MWh and €54.37/MWh, respectively. Meanwhile, on Saturday, February 21, the Nordic market reached €69.07/MWh, its lowest price since January 3.

On the other hand, the German, Italian and Nordic markets registered daily prices above €100/MWh in at least one session during the third week of February. In the Italian market, daily prices exceeded €105/MWh in most sessions, while the Nordic market reached the highest daily average of the week among the analyzed markets, €128.91/MWh, on February 18.

During the week of February 16, lower gas and CO2 emission allowance prices, higher solar energy production and lower demand in most markets drove European electricity market prices down. Increased wind energy production in Germany, France and Italy also contributed to the price declines. In contrast, lower wind energy production in the Iberian Peninsula pushed prices up in Spain and Portugal.

AleaSoft Energy Forecasting’s price forecasts indicate that prices will increase in most European electricity markets during the fourth week of February, influenced by lower wind energy production. However, lower demand may push prices down in the German and Belgian markets. The significant increase in solar energy production in the German market will also contribute to this trend.

Source: Prepared by AleaSoft Energy Forecasting using data from OMIE, Nord Pool and GME.

Source: Prepared by AleaSoft Energy Forecasting using data from OMIE, Nord Pool and GME.Brent, fuels and CO2

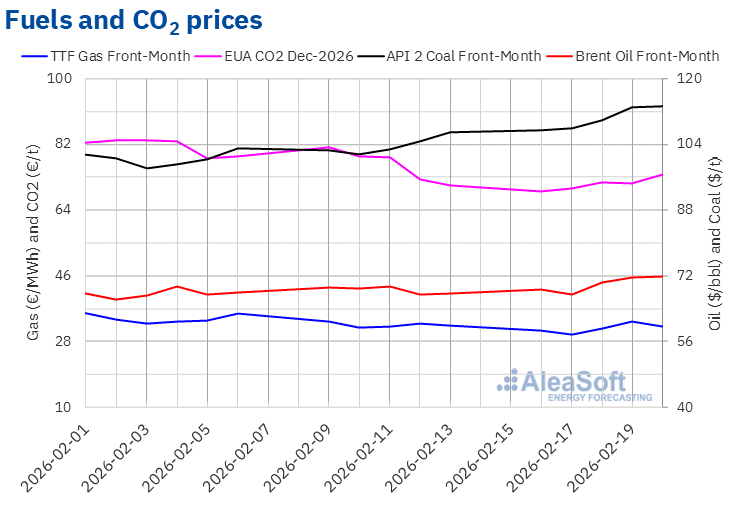

During the third week of February, settlement prices of Brent oil futures for the Front‑Month in the ICE market followed a mostly upward trend. However, on Tuesday, February 17, prices fell and reached the weekly minimum settlement price, $67.42/bbl. Due to price increases during the week, these futures reached their weekly maximum settlement price, $71.76/bbl, on Friday, February 20. According to data analyzed at AleaSoft Energy Forecasting, this price stood 5.9% above the previous Friday’s level and marked the highest level since July 31, 2025.

Rising tensions in the Middle East supported Brent oil futures prices during the third week of February. However, expectations surrounding the second round of negotiations between the United States and Iran, peace talks between Russia and Ukraine, as well as the possibility that OPEC+ may resume production increases in April, contributed to the price decline on Tuesday, February 17. The lack of progress in those negotiations, along with increased tensions in the Middle East, supported further price increases during the remainder of the week.

As for TTF gas futures in the ICE market for the Front‑Month, they reached their weekly minimum settlement price, €29.82/MWh, on Tuesday, February 17. According to data analyzed at AleaSoft Energy Forecasting, this price marked the lowest level since January 10. In the following sessions, settlement prices exceeded €31/MWh. On Thursday, February 19, these futures reached their weekly maximum settlement price, €33.52/MWh. However, on Friday, February 20, the settlement price fell to €32.03/MWh, 1.4% below the previous Friday’s level.

Milder temperature forecasts in Europe and higher temperatures in the United States, which increased liquefied natural gas availability for export, pushed settlement prices below the previous week’s levels during the first sessions of the third week of February, dropping below €30/MWh on Tuesday. However, concerns about potential supply disruptions linked to rising tensions between the United States and Iran drove prices higher in the second half of the week. Even so, Friday’s settlement price still remained slightly below the previous Friday’s level.

Regarding CO2 emission allowance futures in the EEX market for the reference contract of December 2026, they reached their weekly minimum settlement price, €69.16/t, on Monday, February 16. According to data analyzed at AleaSoft Energy Forecasting, this price marked the lowest level since May 2, 2025. During the rest of the third week of February, settlement prices stayed above €70/t and increased in most sessions. As a result, on Friday, February 20, these futures reached their weekly maximum settlement price, €73.79/t, which was 4.4% above the previous Friday’s level.

Source: Prepared by AleaSoft Energy Forecasting using data from ICE and EEX.

Source: Prepared by AleaSoft Energy Forecasting using data from ICE and EEX.AleaSoft Energy Forecasting’s analysis on the prospects for energy markets in Europe and battery storage

On Thursday, February 12, AleaSoft Energy Forecasting held its 63rd monthly webinar. Tomás García, Senior Director, Energy & Infrastructure Advisory at JLL, participated for the fifth time in the monthly webinar series. The main topics analyzed during the webinar include the evolution and prospects of European energy markets, insights from recent BESS transactions in Spain and the key valuation drivers for stand‑alone BESS projects in Spain. The company published an excerpt from the analysis table of the webinar in Spanish on its YouTube channel, AleaSoft Energy Forecasting, as well as on Spotify and iVoox.

Source: AleaSoft Energy Forecasting.