AleaSoft Energy Forecasting, March 6, 2026. In electricity markets, many fundamental models fail not because of the physical operation of the system, but because they do not reproduce the real equilibrium that ultimately determines the price. A hybrid approach that combines a fundamental structure with statistical models, Artificial Intelligence and Machine Learning makes it possible to capture temporal dynamics, non‑linearities and regime changes, improving the price signal and its distribution for investment and hedging decisions.

In wholesale electricity markets, the main challenge for many fundamental models is not to calculate a technically correct “merit order”, but to reproduce the market equilibrium that ultimately determines prices in the long term. The key lies in the fact that, in a marginalist market, the price is not equivalent to the cost, but rather the result of aggregated supply and demand curves, the marginal technology that sets the price, the degree of scarcity in each hour and, above all, prices that in the long term allow investment in new generation plants to be profitable while keeping costs affordable for consumers.

When a model is limited to calculating a merit order hour by hour, or every 15 minutes, it tends to underestimate scarcity episodes, hourly spreads, distribution tails, regime changes that explain a large part of the observed behaviour and, more importantly, it loses the long‑term perspective necessary to forecast prices that allow the market to remain sustainable.

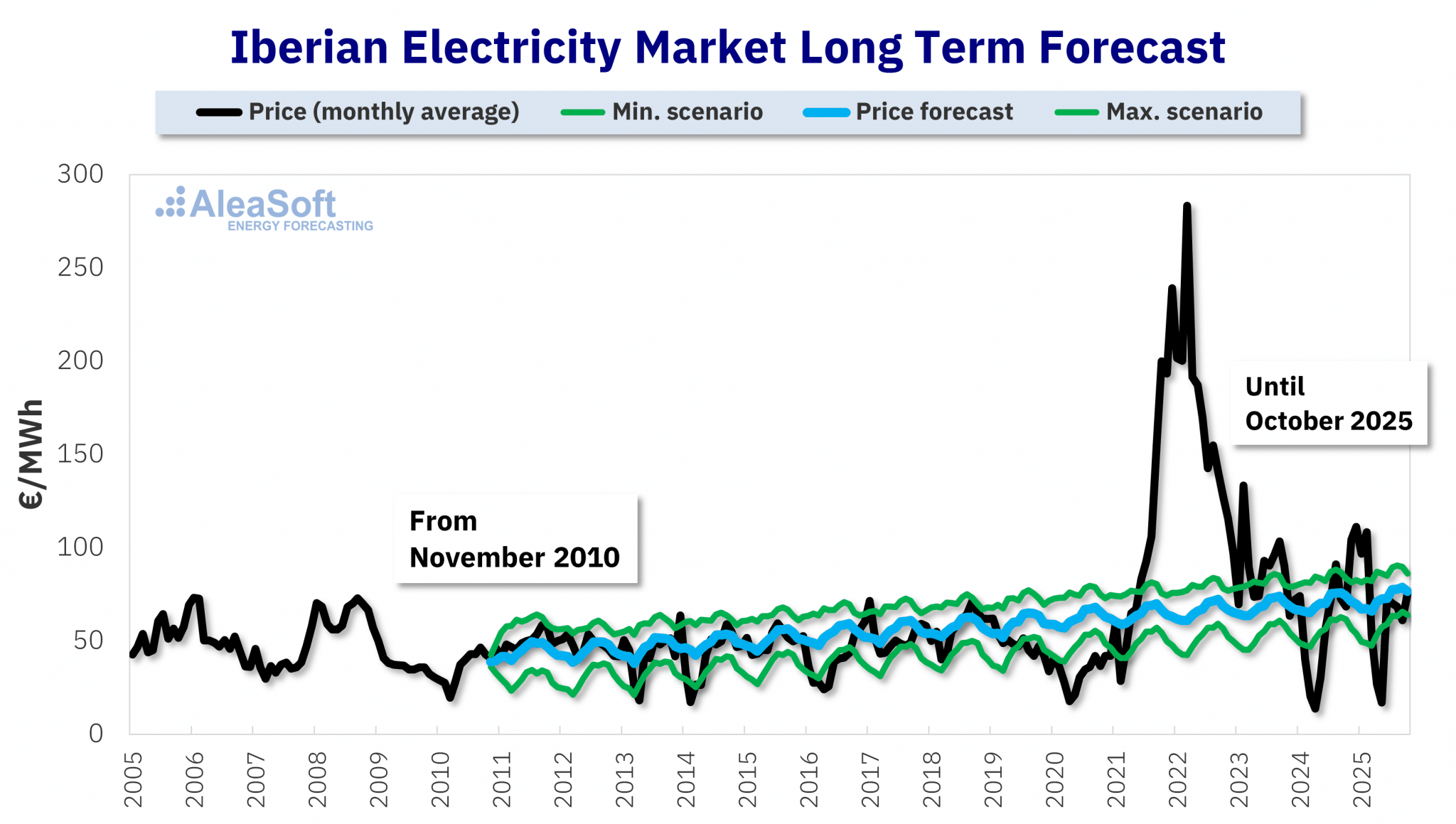

15 year price forecast carried out in October 2010 for the Iberian electricity market.

15 year price forecast carried out in October 2010 for the Iberian electricity market.Source: AleaSoft Energy Forecasting.

Buy and sell bids in electricity markets

Fundamental models replicate the selling bids of producers and the buying bids of consumers and retailers. Each market participant has its own strategy, influenced by factors such as the policy of the corporate group, hedging strategies and long‑term objectives, which vary significantly among agents. Attempting to model their behaviour under common criteria does not adequately reflect the reality.

One of the most critical aspects is the treatment of hydroelectric energy generation. In practice, hydroelectric energy, and partly also other technologies with a strong strategic component, is not offered simply at marginal cost. There is mid‑ and long‑term optimisation based on the value of stored water, expectations, operational constraints and strategic decisions. If the model does not represent this “water economy” and its interaction with the rest of the system, the resulting equilibrium becomes biased and the modelled price deviates, particularly in situations of system stress.

Another relevant aspect is the modelling of demand and flexibility, which is often too deterministic. Net demand, that is, the energy requested from the grid, depends on weather conditions and the calendar, but also on factors such as economic activity and the implicit response of the system, including self‑consumption, pumped storage and industrial interactions. When a fundamental model is rigid, it tends to smooth ramps, fail to reproduce peaks accurately and lose the scarcity signal that ultimately drives prices in the most critical hours.

System frictions complete the picture. A relevant part of real price formation arises from internal congestion, technical constraints, outages and interconnection limits and their effective use. If these elements are introduced through simple approximations or treated in an overly aggregated way, the model may remain technically consistent but become misaligned with the observed market equilibrium. In addition, the regulatory framework and small operational changes often act as triggers for new regimes: changes in rules, tariffs, mechanisms, limits, taxes or operational criteria alter the equilibrium and require recalibrations that, if not carried out quickly, leave the fundamental model poorly explaining the new market environment.

Hybrid models

In view of these limitations, AleaSoft Energy Forecasting considers that the advantage does not lie in ‘using AI for the sake of using AI’, but in combining causal structure with market learning through a hybrid methodology. In this approach, the fundamental model acts as the basis for capturing the main drivers of the market (renewable energy penetration, fuels and CO₂, interconnection, hydro generation, outages), while ensuring consistency in long‑term scenarios associated with energy transition plans, plant closures, new capacity additions, storage, demand and electrification.

The statistical component of hybrid models provides what the fundamental model cannot capture: temporal dynamics. Techniques from the Box‑Jenkins family, such as ARIMA/SARIMA, allow modelling of autocorrelation, hourly, weekly and annual seasonal patterns, and the persistence typically observed in prices and spreads. This makes it possible to capture inertia and recurring patterns, such as wind periods or demand regularities, which an essentially static merit order cannot reproduce.

On this basis, Artificial Intelligence and Machine Learning algorithms are used to capture non‑linearities, interactions and regime changes that are difficult to parameterise. Relationships between variables in energy markets are highly non‑linear and depend on factors such as the level of generation, the hour of the day, demand, the thermal generation mix, hydrological conditions and the level of interconnection. In addition, Neural networks are capable of identifying critical combinations, such as simultaneous increases in CO₂ and gas prices together with a decrease in wind energy generation and low reservoir levels, which can alter the distribution of prices more significantly than any single factor. When trained with appropriate data windows and variables, the model adapts better to structural changes while maintaining consistency with the market equilibrium in the long term.

The ultimate objective is to reproduce the “de facto market equilibrium”: identifying systematic biases in fundamental models and correcting them with statistical and Machine Learning models until obtaining a price that reflects the observed market equilibrium, not only the technical one. For the end user of the forecasts, the impact translates into what matters most for decision‑making: better representation of uncertainty (P10/P90) and hourly volatility, which are key elements in the evaluation of BESS projects, hybridisation, DSCR and covenants, a better estimation of captured prices and solar and wind cannibalisation, and greater consistency in long‑term horizons.

Prospects for energy markets in Europe. Spring 2026

The 64th monthly webinar organised by AleaSoft Energy Forecasting will take place on March 12, 2026, at 10:00 CET and will focus on the analysis of the recent evolution of energy markets in Europe, the prospects for the spring and the key developments that will influence the sector during 2026. The session will address the most relevant regulatory changes, as well as the increasingly important role of energy storage and capacity markets in an electricity system characterised by a growing penetration of renewable energy and increasing price volatility.

In this context, AleaStorage provides advanced solutions to optimise, analyse revenues and structure energy storage projects and hybrid systems associated with renewable energy generation, with the aim of maximising the value and profitability of assets.

The event will once again include the participation of specialists from EY, who will contribute their experience in regulation, financing of renewable energy and storage projects, PPA, self‑consumption and valuation of energy assets and portfolios.

Source: AleaSoft Energy Forecasting.