AleaSoft Energy Forecasting, March 20 2026. Interview by Sergio Matalucci of pv magazine, with Antonio Delgado Rigal, PhD in Artificial Intelligence, founder and CEO of AleaSoft Energy Forecasting.

How does the current geopolitical situation change in the business plans of hydrogen investments?

Geopolitics has reinforced the strategic value of hydrogen in Europe, but it has also made business plans much more demanding. It is no longer enough to announce capacity or ambitious projects: investors are now looking for real demand, solid offtake agreements, access to competitive renewable electricity prices, and a clear regulatory framework.

Hydrogen is seen not only as a decarbonisation opportunity, but also as a tool for energy security, reindustrialisation, and reducing external dependence.

In which country is this more visible? Why?

Probably Germany. It is the clearest case because the gas crisis following Russia’s invasion of Ukraine made the cost of depending on fossil fuel imports much more evident, and this has pushed the country to turn hydrogen into a central role of its industrial and energy security strategy.

The German Government approved a specific import strategy aimed at covering between 50% and 70% of its hydrogen demand in 2030 through imports, while it is also deploying a 9,040 km of hydrogen pipelines.

Do you expect these considerations to change?

Yes, but not in the essentials. If the conflict lasts longer than expected or energy tensions reappear, these considerations will become even stronger. If the geopolitical situation stabilises, the sense of urgency will probably ease, but this new investment approach will not disappear. Europe has already incorporated hydrogen into a logic of competitiveness, energy security and industrial policy, as reflected in the Clean Industrial Deal and the strengthening of the European Hydrogen Bank.

At the same time, demand will remain the main filter. The IEA insists that the key uncertainty is not only geopolitical, but also the lack of firm offtake and predictable revenues. So the intensity of the momentum may change, but not the priority given to more bankable projects.

Of course, all these considerations depend on the length of the conflict, right? What, in your opinion, would be a duration that would make hydrogen investments even more interesting?

Yes, to some extent, but rather than setting an exact duration, what really matters is that the market perceives the shock as non-temporary. If the conflict lasts only a few months, many investments will continue to wait. If it extends for two or three years, with several winters and a time horizon already compatible with final investment decisions, hydrogen starts to be seen as a much more solid investment. From that point on, it is not only decarbonisation that matters, but also protection against gas price volatility, external dependence and the risk of new supply tensions. For hydrogen to become clearly more attractive from an investment perspective, the key factor is not a single episode, but a persistent tense geopolitical scenario.

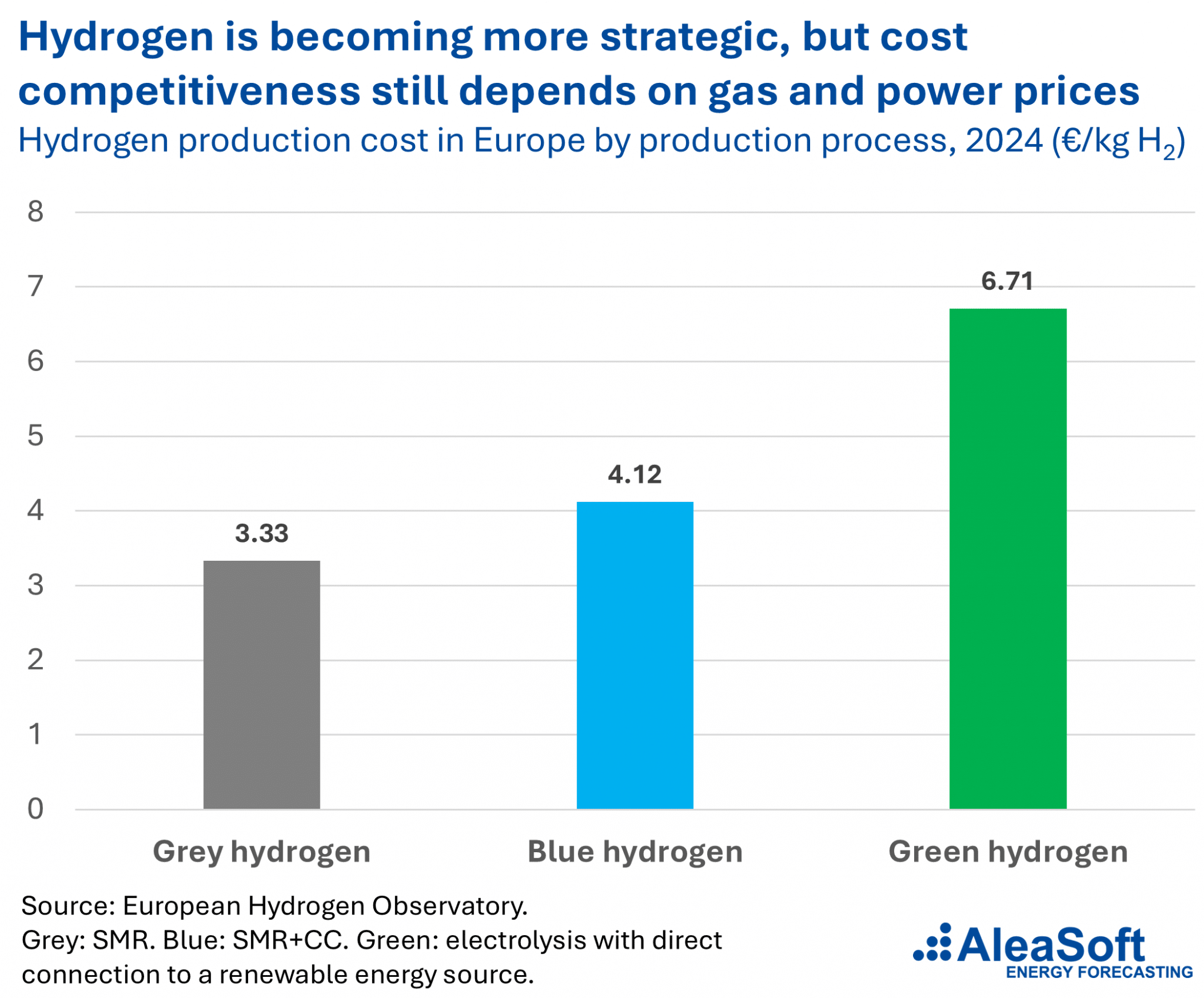

Do you see now green hydrogen being more competitive vis-a-vis grey and blue hydrogen? When would green hydrogen be more convenient than blue hydrogen? At which gas prices?

At present, in general terms, not yet. In Europe, green hydrogen remains, on average, less competitive than both grey and blue hydrogen. ACER places the cost of hydrogen produced by electrolysis at around €6/kg, and renewable hydrogen under RFNBO criteria at close to €8/kg, compared with less than €3/kg for grey hydrogen and around €4/kg for blue hydrogen with CO2 capture. The comparison could be closer in projects with very competitive renewable electricity costs, stable PPAs, and more aggressive regulations on emissions.

In relation to blue hydrogen, the useful benchmark is the gas price. If gas is trading sustained at around €40/MWh, the competitive window for blue hydrogen is already very narrow. For blue hydrogen to maintain a clear long-term advantage, gas prices would need to be around €15/MWh or lower, in addition to CO2 capture rates above 90% and very low methane leakage.

Green hydrogen is not yet cheaper in general terms, but it is becoming increasingly more economically defensible wherever renewables are competitive and gas is no longer low cost.

Experts rightly explain that last week showed that BESS does not just create value during periods of price volatility, it makes power systems more resilient in the face of external shocks. For instance, some analysts mentioned Spain, the UK, Germany, and the Netherlands. Why are these countries more resilient than other? Would this argument apply also in case of countries with a strong green hydrogen production?

These countries are more resilient not simply because they have more batteries, but because they combine several layers of flexibility. The UK has one of the most advanced frameworks for integrating batteries, interconnection and long-duration storage. Germany is adding flexibility not only through storage, but also through demand-side management and new flexible loads, its regulator explicitly stresses that batteries, electric vehicles, heat pumps and electrolyzers are making a growing contribution to security of supply.

In Spain and the Netherlands, the logic is similar. In Spain, after the recent episodes of stress, storage has come to be seen as a critical element of resilience and energy security. In the Netherlands, the main pressure comes from grid congestion and the need to integrate large volumes of variable renewable generation.

These countries have in common that they have more renewables, stronger price signals, more developed markets and regulatory frameworks that allow flexibility to be real operational resilience.

Part of this argument would also apply to countries with strong green hydrogen production in some way. Batteries are especially valuable for fast response over seconds, minutes and hours, whereas hydrogen contributes more over multi-day horizons, industrial backup and seasonal flexibility. A country with large-scale green hydrogen production can be more resilient if its electrolyzers operate flexibly and absorb renewable surpluses, but hydrogen complements batteries, it does not replace them.

How can data pave the way for new investments in hydrogen assets in the Old Continent?

It can when they turn a political ambition into a genuinely financeable asset. In Europe, that means having reliable information on costs, potential demand, access to renewable electricity, available infrastructure and potential buyers. Greater transparency on hydrogen costs is essential to guide investment in production and infrastructure, and the main bottleneck remains turning uncertain demand into bankable offtake.

The European Hydrogen Observatory provides data on production, demand, costs and infrastructure, while the Commission’s Hydrogen Mechanism gathers supply and demand signals to connect buyers and sellers, guide the development of transport and storage, and give the market greater visibility.

The better the data, the lower the uncertainty around location, revenues and the actual use of assets, and the lower that uncertainty, the easier it is for new projects to reach final investment decision.

What’s very specific about Spain?

What is most specific about Spain is that it approaches hydrogen not only as a decarbonisation need, but also as a potential competitive advantage. Spain combines a particularly favourable renewable resource base, a very explicit public strategy, and a highly ambitious target. The PNIEC already envisages close to 12 GW of electrolyzers by 2030. This means that, compared with other European countries that are more dependent on importing energy or hydrogen, Spain aims to produce it with competitively priced renewable electricity and to turn that advantage into industrial policy.

In addition, Spain has a very important geographical singularity. It can act as a connection platform between Iberia’s renewable potential and Europe’s major consumption centres. This is where H2med fits in, designed to link the Iberian Peninsula with central Europe and transport renewable hydrogen from countries with abundant resources, such as Spain and Portugal, to consuming markets like France and Germany. Spain’s case is distinct because it can simultaneously play the role of producer, industrial consumer, and export hub.

And how is the Italian case different?

Italy’s case is different because, compared with Spain, it is less positioned as a large producer-exporter supported by a renewable advantage, and more as a major industrial, logistical and transit market. Its national strategy makes clear that, up to 2030, demand will be driven mainly by European obligations in industry and transport, and Italy also starts from a relevant base of hydrogen consumption in conventional uses, as in Spain, more than 80% of domestic consumption is concentrated in refining. Italy hydrogen is seen as a tool for industrial decarbonisation and for replacing existing fossil-based uses.

The other major difference is geographical. While Spain aims to leverage its renewable abundance to produce at competitive costs, Italy also wants to play the role of an energy bridge between North Africa and demand in central Europe. This is where the Italian H2 Backbone and the SoutH2 Corridor come in, designed to connect supply coming from North Africa and southern Italy with Austria and Germany from 2030 onwards. If Spain is seen more as a potential origin of renewable hydrogen production, Italy is more clearly emerging as an industrial hub and a strategic corridor for imports and transport.