AleaSoft Energy Forecasting, September 1, 2025. In the fourth week of August, weekly prices in most major European electricity markets were below €85/MWh. During the week, the markets showed mixed performance. The British and French markets registered daily prices below €20/MWh, while in Germany and Italy they exceeded €100/MWh. Demand grew, photovoltaic energy production fell and wind energy production increased, in a context where TTF gas showed a downward trend, although on average it increased compared to the previous week, CO2 remained stable and Brent settled slightly higher.

Solar photovoltaic and wind energy production

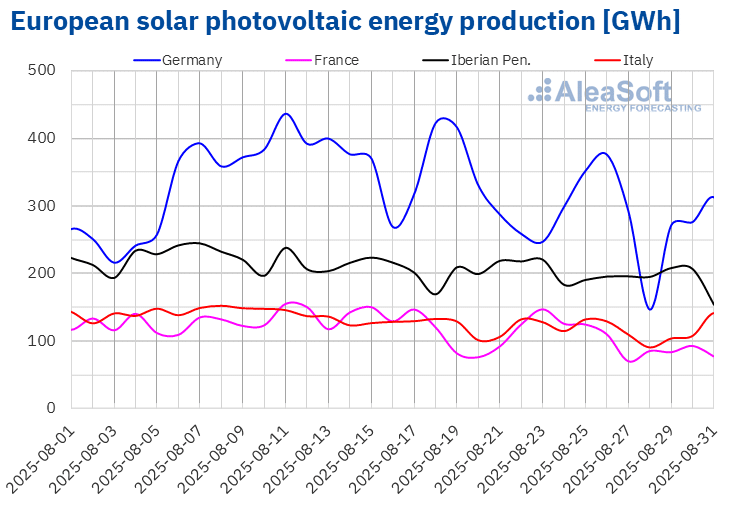

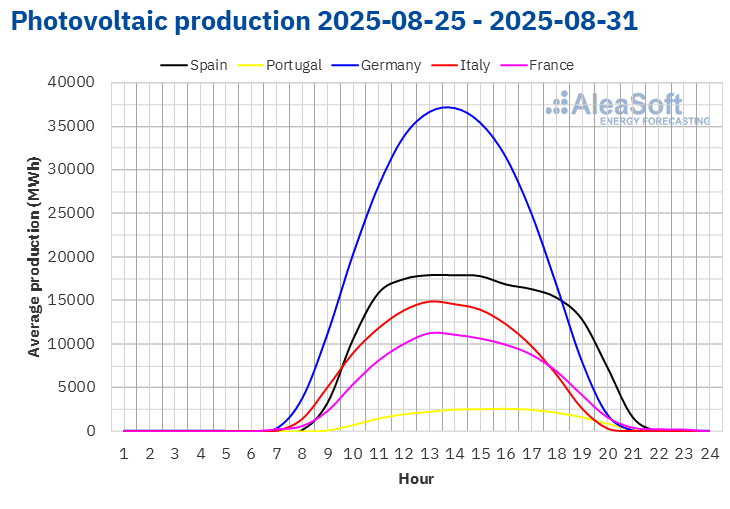

During the week of August 25, solar photovoltaic energy production decreased in the main European electricity markets compared to the previous week. The French and German markets registered the largest declines, 16% and 10% respectively, marking their second consecutive week of declines. The Italian and Spanish markets registered the smallest declines, 3.5% and 4.5%, respectively, and accumulated three weeks of declines. The Portuguese market reduced its production by 9.9%, after having registered increases in the previous week.

For the week of September 1, AleaSoft Energy Forecasting’s solar energy forecasts indicate that solar photovoltaic energy production will increase in the Spanish market and decrease in the German and Italian markets.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA. Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.

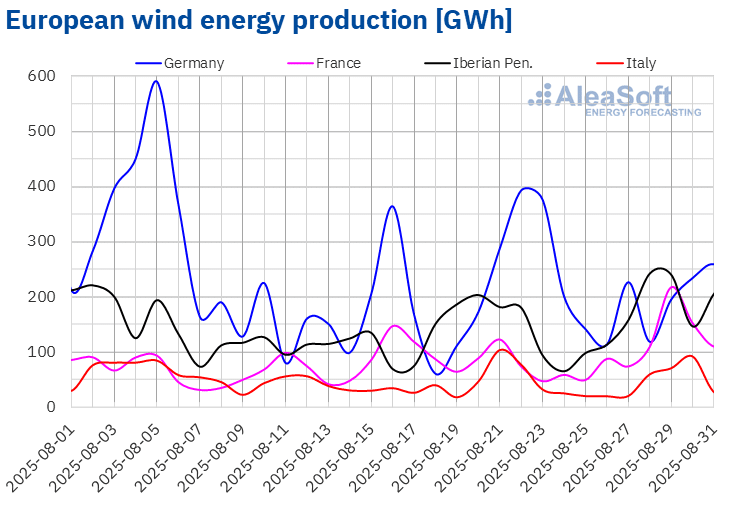

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.In the fourth week of August, wind energy production increased in most major European electricity markets compared to the previous week. France registered the largest increase, 47%. The Iberian Peninsula registered increases of 8.0% in Spain and 32% in Portugal, continuing the upward trend for the second and third consecutive weeks, respectively. In contrast, the German and Italian markets reduced their generation with this technology. The German market registered the largest decline, 20%, while the Italian market cut its energy production by 9.5%.

During the week, the French market reached its third‑highest daily wind energy production for an August month, on Friday, August 29, when it generated 218 GWh.

For the first week of September, according to AleaSoft Energy Forecasting’s wind energy forecasts, wind energy generation will increase in the German, Spanish and French markets. In contrast, production using this technology will decrease in the Portuguese and Italian markets.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE and TERNA.Electricity demand

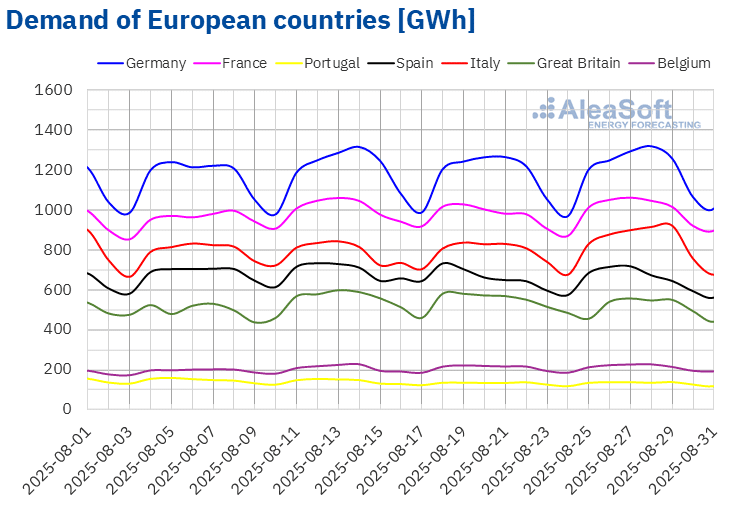

In the last week of August, electricity demand increased in most major European markets compared to the previous week. The Italian market registered the largest increase, 6.3%, followed by 3.2% in the French market and 2.1% in the German market. The Spanish market showed the smallest increase, 0.7%, while demand grew by 0.9% in Portugal and 1.5% in Belgium. The Italian market registered its second consecutive week of increases and the Belgian market maintained its upward trend for the fifth consecutive week. However, in the British market, demand fell for the second consecutive week, with a 7.0% decline due to the Summer Bank Holiday celebrated in Great Britain on August 25.

Average temperatures showed mixed behavior in the analyzed markets. Spain, Great Britain, Belgium and Germany registered increases ranging from 0.1 °C in Spain to 1.3 °C in Germany. In contrast, France, Portugal and Italy registered decreases ranging from 0.2 °C in France to 0.7 °C in Italy.

For the first week of September, AleaSoft Energy Forecasting’s demand forecasts point to a decrease in demand in the Belgian, Spanish and French markets, while the German, British, Italian and Portuguese markets will register increases.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE, TERNA, National Grid and ELIA.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, REE, TERNA, National Grid and ELIA.European electricity markets

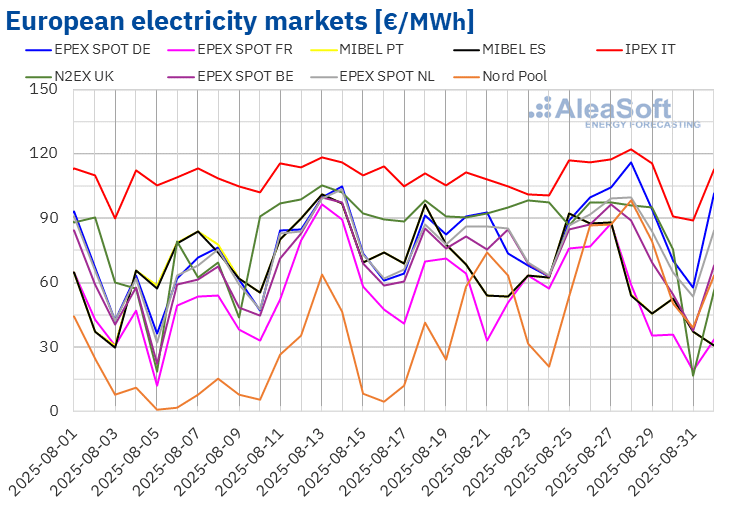

In the fourth week of August, prices in the main European electricity markets showed mixed performance compared to the previous week. The Nord Pool market of the Nordic countries registered the largest percentage increase in the weekly average price, 58%. The IPEX market of Italy and the EPEX SPOT market of the Netherlands and Germany also registered price increases, 3.6%, 4.3% and 12%, respectively. In contrast, the N2EX market of the United Kingdom registered the largest drop, 15%. In the rest of the markets analyzed at AleaSoft Energy Forecasting, prices fell between 3.0% in the EPEX SPOT market of Belgium and 5.0% in the EPEX SPOT market of France.

In the week of August 25, weekly averages were below €85/MWh in most European electricity markets. The exceptions were the German and Italian markets, whose averages were €90.19/MWh and €109.82/MWh, respectively. The French market registered the lowest weekly average, €55.56/MWh. In the rest of the markets analyzed at AleaSoft Energy Forecasting, prices ranged from €65.37/MWh in the MIBEL market of Spain to €82.77/MWh in the Dutch market.

Regarding daily prices, on Sunday, August 31, the British market reached the lowest average of the week among the analyzed markets, €16.57/MWh. This price was the lowest in the British market since May 26. On August 31, the French market also registered a price below €20/MWh, at exactly €18.88/MWh. On the other hand, in the fourth week of August, the German and Italian markets registered daily prices above €100/MWh. On August 28, the Italian market reached the highest daily average of the week, €122.21/MWh. On that day, the Nordic market registered its highest price since March 14, €98.47/MWh.

In the week of August 25, increased wind energy production in the Iberian Peninsula and France favored lower prices in the Spanish, French and Portuguese markets. Falling demand in the British market contributed to lower prices in that market. On the other hand, the increase in weekly gas and CO2 emission allowance prices, as well as the increase in demand, led to price rises in other markets. In the case of the German and Italian markets, moreover, wind and solar energy production fell.

AleaSoft Energy Forecasting’s price forecasts indicate that, in the first week of September, prices will fall in most European electricity markets, influenced by increased wind energy production and lower demand in some markets. In addition, solar energy production will increase in Spain.

Source: Prepared by AleaSoft Energy Forecasting using data from OMIE, , Nord Pool and GME.

Source: Prepared by AleaSoft Energy Forecasting using data from OMIE, , Nord Pool and GME.Brent, fuels and CO2

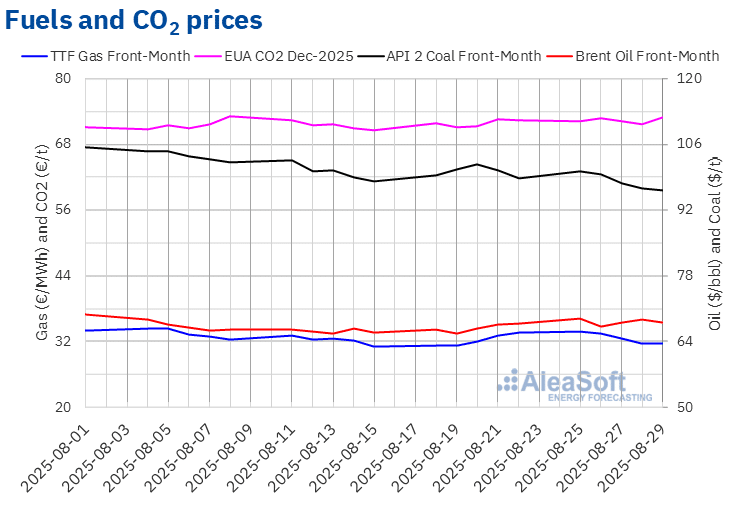

Brent oil futures for the Front‑Month in the ICE market reached their weekly maximum settlement price, $68.80/bbl on Monday, August 25. After falling 2.3% from the previous day, on Tuesday, August 26, these futures registered their weekly minimum settlement price, $67.22/bbl. On August 27, prices rose again and remained above $68/bbl for the rest of the fourth week of August. On Friday, the settlement price was $68.12/bbl. According to data analyzed at AleaSoft Energy Forecasting, this price was 0.6% higher than the previous Friday.

The evolution of the conflict between Russia and Ukraine exerted an upward influence on Brent oil futures prices in the fourth week of August. However, increased OPEC+ production and expectations of lower demand limited price growth. In the first week of September, price evolution will be influenced by expectations for the upcoming OPEC+ meeting, to be held at the end of the week.

As for TTF gas futures in the ICE market for the Front‑Month, they reached their weekly maximum settlement price, €33.77/MWh, on Monday, August 25. Subsequently, prices fell. As a result, on Thursday, August 28, these futures registered their weekly minimum settlement price, €31.56/MWh. On Friday, August 29, the settlement price was slightly higher, €31.62/MWh. According to data analyzed at AleaSoft Energy Forecasting, this price was 5.8% lower than the previous Friday. However, even with price declines during the week, the weekly average settlement price was 1.1% higher than last week.

In the fourth week of August, maintenance work reduced gas flows from Norway. Despite this, European reserves continued to rise because gas consumption was low. The availability of liquefied natural gas, favored by weak demand in Asia, also contributed to the decline in prices. In addition, Russian liquefied natural gas supplies to China could also reduce competition for global liquefied natural gas supplies.

Regarding settlement prices of CO2 emission allowance futures in the EEX market for the reference contract of December 2025, they remained above €72/t for most of the fourth week of August. However, on Thursday, August 28, they registered their weekly minimum settlement price, €71.74/t. In contrast, after a 1.7% increase from the previous day, on Friday, August 29, these futures reached their weekly maximum settlement price, €72.97/t. According to data analyzed at AleaSoft Energy Forecasting, this price was 0.6% higher than the previous Friday.

Source: Prepared by AleaSoft Energy Forecasting using data from ICE and EEX.

Source: Prepared by AleaSoft Energy Forecasting using data from ICE and EEX.AleaSoft Energy Forecasting’s analysis on the prospects for energy markets in Europe, batteries and self‑consumption

The 58th webinar of the monthly webinar series of AleaSoft Energy Forecasting will take place on Thursday, September 18. On this occasion, the webinar will analyze the evolution and prospects of European energy markets, the prospects for battery energy storage, as well as the current situation and prospects for self‑consumption. During the webinar, there will also be a presentation of AleaSoft services for retailers.

The analysis table in the second part of the webinar in Spanish will feature Xavier Cugat, BESS Technical Director at Seraphim, Francisco Valverde, independent professional for the renewable energy development, and Alejandro Diego Rosell, energy communicator and consultant, Director of Studies at World Wide Recruitment and Lecturer at EOI.

Source: AleaSoft Energy Forecasting.