AleaSoft Energy Forecasting, November 17, 2025. In the second week of November, prices fell in most major European electricity markets compared to the previous week, driven by an increase in wind energy production and a decline in gas prices. On November 13, TTF gas futures registered their lowest settlement price since May 2024, €30.46/MWh. Electricity demand rose in most major European markets, while solar photovoltaic energy production declined.

Solar photovoltaic and wind energy production

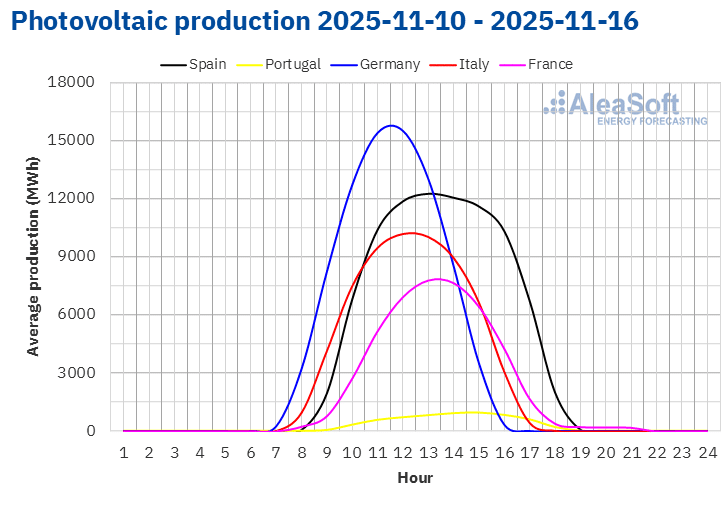

In the week of November 10, solar photovoltaic energy production decreased in the main European markets compared to the previous week. The Portuguese market registered the largest decline, 45%, while the Italian market showed the smallest, 11%. The French, Spanish and German markets registered decreases of 18%, 21% and 27%, respectively.

For the week of November 17, according to AleaSoft Energy Forecasting’s solar energy forecasts, photovoltaic energy production will increase in the Spanish market, but it will fall in the Italian and German markets.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica and TERNA.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica and TERNA. Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica and TERNA.

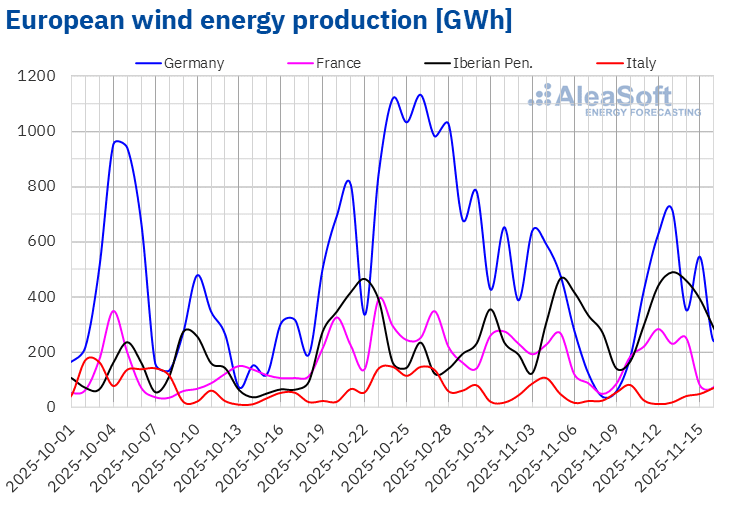

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica and TERNA.In the second week of November, wind energy production increased in most major electricity markets in Europe compared to the previous week. The Iberian Peninsula markets registered their second consecutive week of growth. The Portuguese market registered the largest increase, 53%, while the Spanish market registered the smallest rise, 17%. In the French and German markets, generation from this technology rose by 29% and 40%, respectively. In contrast, the Italian market maintained its downward trend for the third consecutive week, with an 18% drop.

For the third week of November, according to AleaSoft Energy Forecasting’s wind energy forecasts, wind energy generation will increase in the Italian and German markets, while it will decrease in the Iberian and French markets.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica and TERNA.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica and TERNA.

Electricity demand

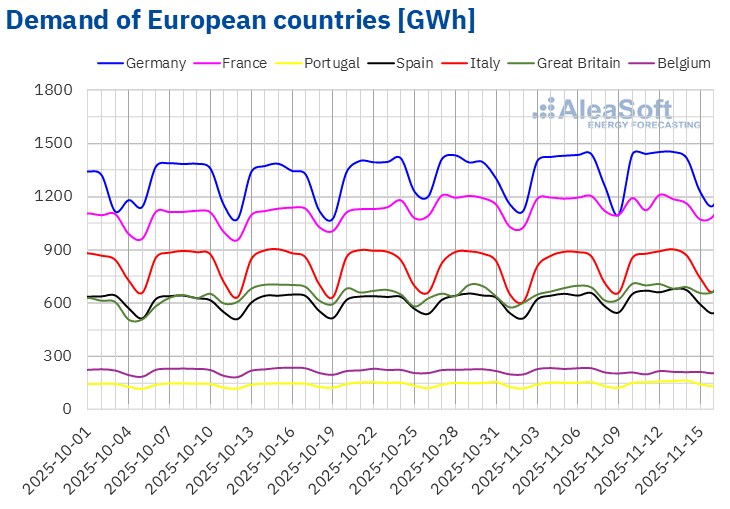

In the week of November 10, electricity demand increased in most major European markets compared to the previous week. The Portuguese market registered the largest rise, 5.8%, while the German market registered the smallest, 1.1%. In the Italian, Spanish and British markets, demand grew by 2.2%, 2.9% and 4.2%, respectively. All markets where demand increased registered their second consecutive week of growth. Meanwhile, demand fell in the French and Belgian markets, by 1.8% and 6.6%, respectively, due to the national holiday on November 11, Armistice Day, in both countries. In the case of the French market, this change reversed a five‑week upward trend.

During the week, most analyzed markets registered higher average temperatures than the previous week. Germany and France registered the largest increases, 1.1 °C and 1.0 °C, respectively. Average temperatures also rose in Italy, Portugal and Spain, by 0.1 °C in the first two markets and 0.3 °C in the latter. In contrast, average temperatures fell in Belgium and Great Britain, by 0.3 °C and 1.7 °C, respectively.

For the third week of November, according to AleaSoft Energy Forecasting’s demand forecasts, electricity demand will increase across all analyzed markets, driven by falling average temperatures across Europe. In the French and Belgian markets, the return to normal working hours following the November 11 holiday will also favor the increase in demand.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica, TERNA, National Grid and ELIA.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica, TERNA, National Grid and ELIA.European electricity markets

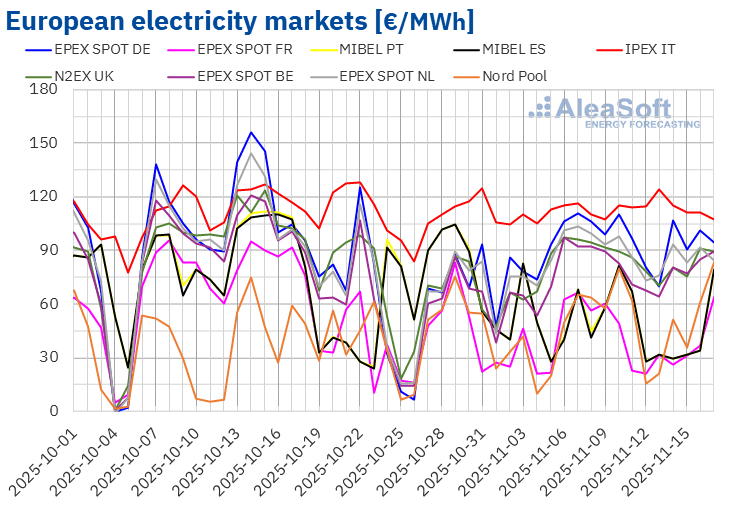

In the second week of November, average prices in most major European electricity markets fell compared to the previous week. The exceptions were the IPEX market of Italy and the Nord Pool market of the Nordic countries, with increases of 3.8% and 6.1%, respectively. Conversely, the EPEX SPOT market of France registered the largest percentage price decline, 34%. In the remaining markets analyzed at AleaSoft Energy Forecasting, prices fell between 1.8% in the EPEX SPOT market of Germany and 19% in the MIBEL market of Portugal.

In the week of November 10, weekly averages were below €85/MWh in most European electricity markets. The exceptions were the Dutch, German and Italian markets, with weekly averages of €85.74/MWh, €93.69/MWh and €115.19/MWh, respectively. The French market registered the lowest weekly average, €31.28/MWh. In the remaining markets analyzed at AleaSoft Energy Forecasting, prices ranged from €43.32/MWh in the Iberian market to €81.54/MWh in the N2EX market of the United Kingdom.

Regarding daily prices, the Nordic market reached the lowest average of the week among the analyzed markets, €15.32/MWh, on November 12. However, on November 10, that market reached its highest price since September 10, €79.85/MWh. On November 17, the average was even higher, €83.06/MWh, although still below the daily price registered on September 9.

During the second week of November, daily prices remained above €110/MWh in the Italian market. The German market also registered prices above €100/MWh on November 10, 14 and 16, although they stayed below €110/MWh. On Thursday, November 13, the Italian market reached the highest daily average of the week, €124.41/MWh.

In the week of November 10, the increase in wind energy production and the decline in gas prices compared to the previous week contributed to lower prices in most European electricity markets. In the French and Belgian markets, electricity demand also decreased. In contrast, rising demand and declining wind energy production contributed to higher prices in the Italian market.

AleaSoft Energy Forecasting’s price forecasts indicate that in the third week of November, prices will rise in the main European electricity markets, driven by increasing electricity demand and falling wind energy production in some markets. However, in the Italian market, the increase in wind energy production will favor lower prices.

Source: Prepared by AleaSoft Energy Forecasting using data from OMIE, , Nord Pool and GME.

Source: Prepared by AleaSoft Energy Forecasting using data from OMIE, , Nord Pool and GME.Brent, fuels and CO2

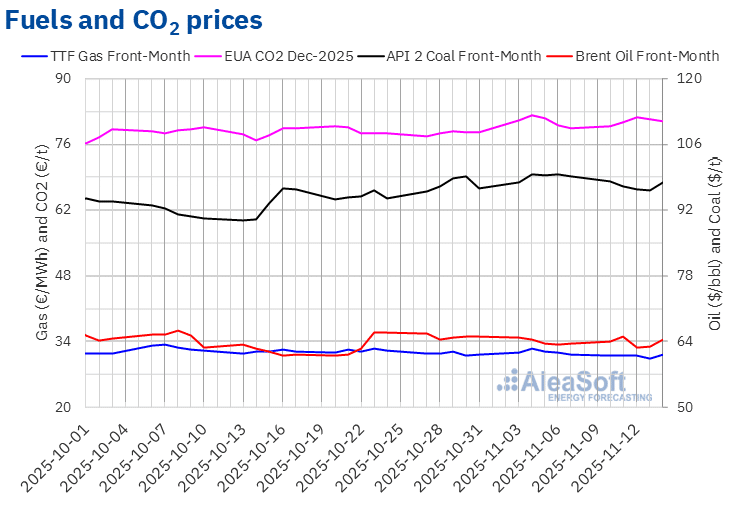

Brent oil futures for the Front‑Month in the ICE market reached their weekly maximum settlement price, $65.16/bbl, on Tuesday, November 11. Conversely, after a 3.8% drop from the previous day, on November 12 these futures registered their weekly minimum settlement price, $62.71/bbl. In the last sessions of the week, prices rose again. On Friday, November 14, the settlement price was $64.39/bbl. According to data analyzed at AleaSoft Energy Forecasting, this price was 1.2% higher than the previous Friday.

Expectations of the end of the United States government shutdown, which could increase the country’s demand, as well as US sanctions on Russian oil companies, helped drive Brent oil futures prices higher at the beginning of the second week of November. However, the International Energy Agency’s production surplus forecasts put downward pressure on prices, which fell in the middle of the week. The Ukrainian attack on Russian oil infrastructure contributed to the rise in prices at the end of the week.

As for TTF gas futures in the ICE market for the Front‑Month, they remained below €31.50/MWh during the second week of November. On Thursday, November 13, these futures registered their weekly minimum settlement price, €30.46/MWh. According to data analyzed at AleaSoft Energy Forecasting, this was the lowest price since May 17, 2024. However, on Friday, November 14, the price increased by 2.6% from the previous day. That day, these futures reached their weekly maximum settlement price, €31.25/MWh, which was 0.2% higher than the previous Friday.

Ample liquefied natural gas supply and high pipeline flows from Norway continued to exert downward pressure on TTF gas futures prices during the second week of November. Liquefied natural gas availability increased due to mild temperatures limiting demand in China. In addition, wind energy production contributed to reducing European gas demand.

In the case of CO2 emission allowance futures in the EEX market for the reference contract of December 2025, on Monday, November 10, they registered their weekly minimum settlement price, €79.96/t. This price was already slightly higher than that of the previous Friday. The upward trend continued until November 12, when these futures reached their weekly maximum settlement price, €81.91/t. In the last sessions of the week, prices declined. On Friday, November 14, the settlement price was €80.94/t. According to data analyzed at AleaSoft Energy Forecasting, this price was still 1.8% higher than the previous Friday.

Source: Prepared by AleaSoft Energy Forecasting using data from ICE and EEX.

Source: Prepared by AleaSoft Energy Forecasting using data from ICE and EEX.AleaSoft Energy Forecasting’s analysis on the prospects for energy markets in Europe and energy storage

On Thursday, November 13, AleaSoft Energy Forecasting held its 60th webinar. In addition to the evolution and prospects of European energy markets for the winter 2025‑2026, the webinar analyzed the prospects for batteries, hybridization and energy storage, as well as AleaSoft services for battery and hybridization projects. In the webinar in Spanish, the guest speaker was Luis Marquina de Soto, president of AEPIBAL, the Business Association of Batteries and Energy Storage.

On Thursday, December 4, AleaSoft Energy Forecasting will hold its next webinar, the 61st edition of its monthly webinar series. This event will focus on the balance of the first year of the five‑year period of batteries, the prospects for the next years of the five‑year period and the strategic vectors of the energy transition, such as renewable energy, demand, grids and storage. The webinar in Spanish will feature the participation of Antonio Hernández García, Partner of Regulated Sectors at EY, Carlos Milans del Bosch, Partner, Corporate Finance Energy at Deloitte, and Oscar Barrero Gil, Partner responsible for Energy Sector at PwC Spain.

Source: AleaSoft Energy Forecasting.