AleaSoft Energy Forecasting, July 16, 2026. Battery storage is consolidating as one of the main drivers of transformation in the Spanish electricity system. Negative prices in solar hours and rising daily spreads are reinforcing its profitability, but the real turning point will come when projects secure financing and operate optimally across the different electricity markets.

In webinar number 68 of AleaSoft Energy Forecasting, held on Thursday, July 9, Oriol Saltó i Bauzà, Associate Partner at AleaSoft, analysed the current situation and outlook for energy storage.

From permits to actually installed capacity

Spain currently has 210 MW of batteries in service, a figure still small compared with the volume of projects under processing. Projects with granted access reach 26 GW, while another 14 GW remain pending. Together, the pipeline totals 40 GW.

These figures show the enormous interest in energy storage, but also the gap between having grid access and building an operational, financeable project. Not every project will reach execution. The quality of the connection point, battery sizing, the revenue strategy, degradation, equipment warranties and the contractual structure will determine which ones can move forward. The challenge is no longer just accumulating permits and access rights, but turning them into assets with solid revenues and manageable risks.

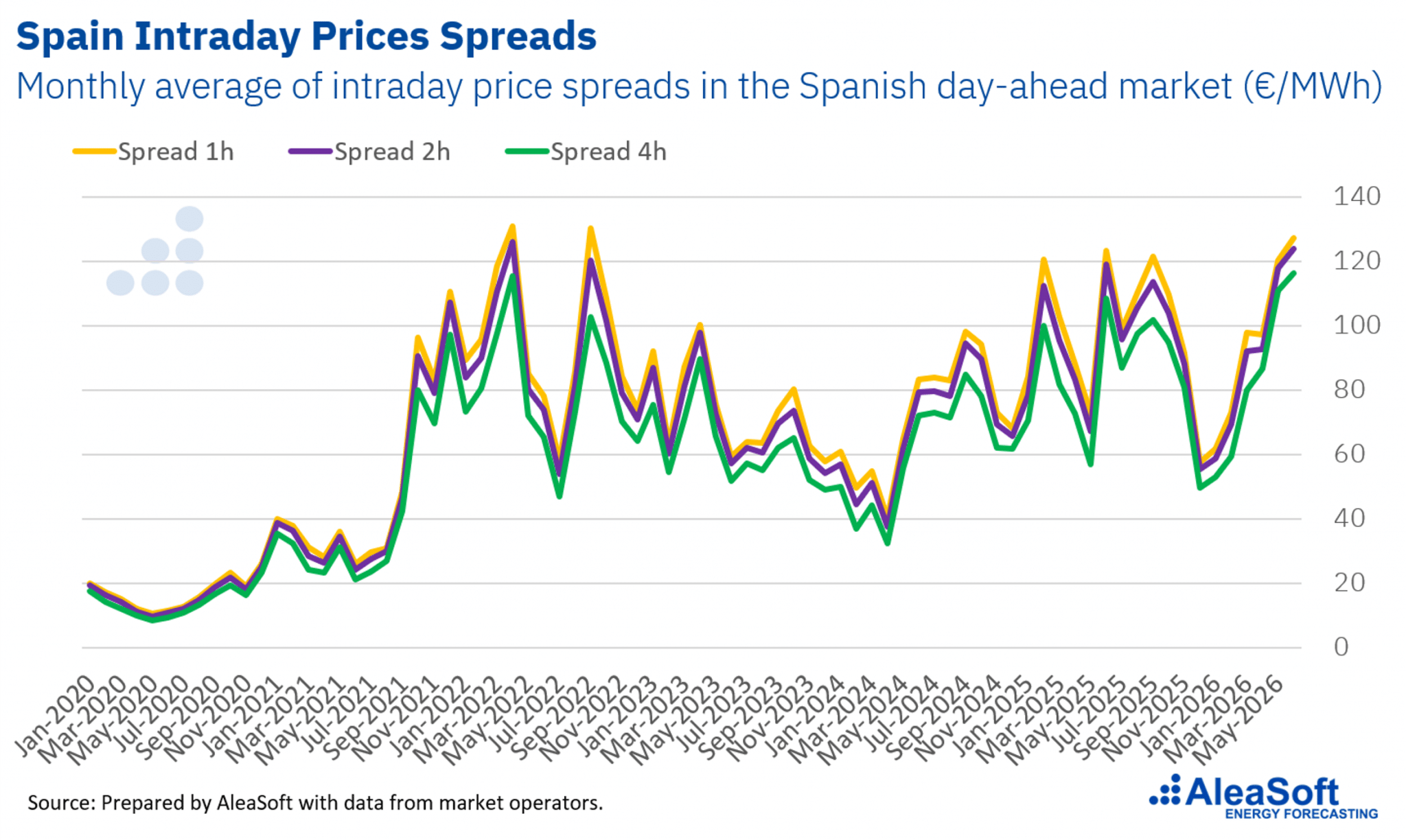

Spreads confirm the opportunity

A battery’s profitability depends less on the average price of electricity than on the difference between the hours with the lowest prices and those with the highest. In June, daily spreads in the Spanish market reached levels above 120 €/MWh for one‑hour and two‑hour spreads, values comparable to those recorded during the 2021 and 2022 energy crisis, although in a different market context.

Taking a simple operation as a reference, with one daily cycle over the past twelve months, a two‑hour battery would have obtained a gross arbitrage margin of approximately 68 000 €/MW, while a four‑hour battery would have reached 123 900 €/MW. In France, the equivalent values were 66 700 €/MW and 117 900 €/MW respectively. Germany showed the highest results, with 88 600 €/MW for two hours and 153 300 €/MW for four hours.

These estimates consider only wholesale market arbitrage. A battery can also participate in the intraday markets, the secondary band, the tertiary band, technical constraints and, in future, capacity mechanisms. This widens the revenue possibilities, but also increases the complexity of the operation.

A battery cannot maximise every service simultaneously without constraints. Each project must define which markets to prioritise, what capacity to reserve for each service and how the strategy will affect the asset’s degradation. Optimisation must therefore not be limited to selecting the cheapest or most expensive hours, but must integrate prices, availability, efficiency, technical warranties and useful life.

Contracted revenues to unlock financing

Financing remains one of the main bottlenecks. Banks particularly value revenues contracted through hybrid PPAs, revenue floors, tolling agreements or capacity mechanisms. The greater the merchant exposure, the lower the leverage and the higher the debt service coverage ratio (DSCR) requirements.

For Spain, the references discussed in the webinar place tolling agreements indicatively between 70 000 €/MW and 100 000 €/MW per year, with possible terms of around ten to twelve years. However, the Spanish market is still emerging and lacks closed deals to consider these figures as consolidated standards.

In financeable structures, the total cost of debt was indicatively estimated at between 4% and 5%, with expected leverage of 60% to 66% once future capacity mechanisms reduce revenue risk. In purely merchant projects, leverage could stand at approximately 45% to 55%. These differences show that contracting part of the revenues can be decisive for securing financing.

The traditional solar PPA, based exclusively on a pay‑as‑produced profile, will need to evolve. Combining photovoltaic generation with batteries makes it possible to shift part of the production towards higher‑value hours, reduce exposure to zero or negative prices and offer profiles closer to buyers’ needs. The result will be more complex contracts, but also better adapted to the producer, the consumer and the financier.

A strategic tool for large consumers

For energy‑intensive consumers, storage is a tool to manage energy costs and reduce risks. A battery can store surplus self‑consumption, charge during low‑price hours and discharge when grid electricity is more expensive. It also allows peak shaving, demand shifting and participation in services such as active demand response (SRAD).

In a real case analysed by AleaSoft, a large consumer with a self‑consumption photovoltaic installation added an optimal 50 MW, 200 MWh battery. The self‑consumption rate rose from 39% to 52%, grid‑sourced consumption fell by 21% and the net economic impact represented a 20% cost reduction, with a payback period of approximately six years.

Bankability as the decisive frontier

Storage already shows signs of profitability. The next stage will be to prove that projects can be financed, built and operated throughout their useful life. The best‑positioned players will not necessarily be those accumulating the most megawatts under processing, but those combining robust forecasts, suitable contracts, realistic financial models and a coherent optimisation strategy.

AleaSoft Energy Forecasting forecasts for storage projects

Spain’s large project pipeline confirms that there will be competition for financing, equipment, optimisers and counterparties. In this environment, hourly price forecasts and long‑term spreads, revenue simulations and financial models will be essential to distinguish a bankable project from a simple access application.

AleaStorage‘s services make it possible to analyse the revenues of standalone and hybrid battery projects, taking into account the different markets, operating scenarios and financing structures. For large consumers, these analyses help determine the optimal storage size and assess its effect on self‑consumption and the electricity bill. Through AleaHub, developers can also search for PPA counterparties, optimisation agreements and tolling agreements.

Source: AleaSoft Energy Forecasting