AleaSoft, October 8, 2020. The European electricity markets prices continued to fall in the second week of October due to the increase in wind energy production. In most markets, the average of the first four days of the week was below €40/MWh. In general, this trend will continue during the weekend, but a recovery is expected in the third week of the month as the wind energy production will decline in some markets. The Brent, gas and coal futures rose in the first days of the week.

Photovoltaic and solar thermal energy production and wind energy production

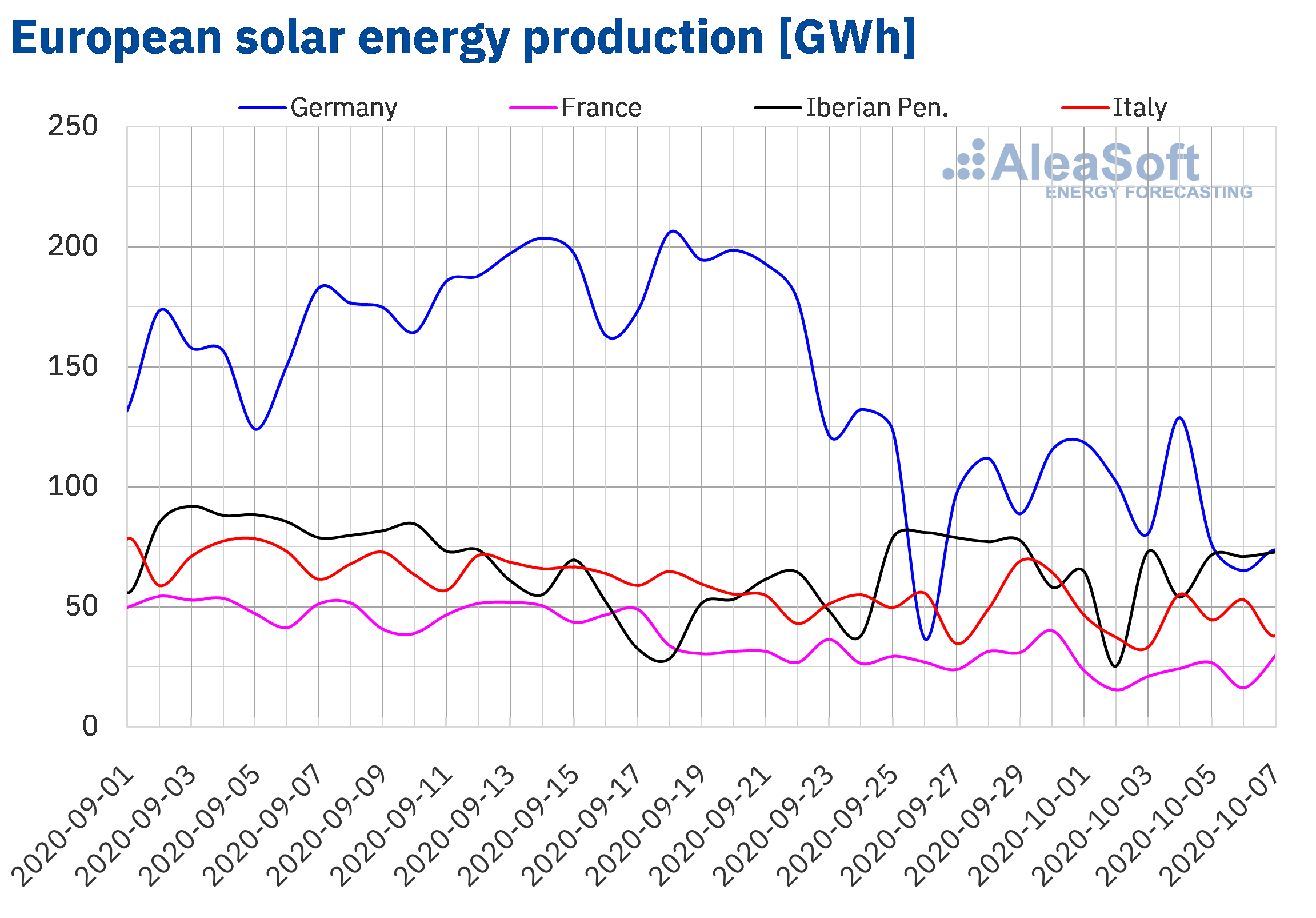

The solar energy production from October 5 to 7 performed unevenly in the electricity markets of Europe compared to the average of the previous week. In Germany the fall was 33%, registering daily values below the minimum of the previous week. On the other hand, the solar energy production in the Italian and French markets fell by 11% and 9.1% respectively. A different behaviour was registered in the Iberian Peninsula, where the generation with this technology increased by 17%.

In the comparison of the seven elapsed days of October 2020 with the same period of 2019, a recovery was observed in Germany and the Iberian Peninsula, where there were increases of 23% and 18% respectively. While, in the cases of France and Italy, there were falls of 16% and 8.4%.

The AleaSoft‘s solar energy production forecasting indicates that at the end of the second week of October the production totals for Germany and Italy will be lower than those of the previous week.

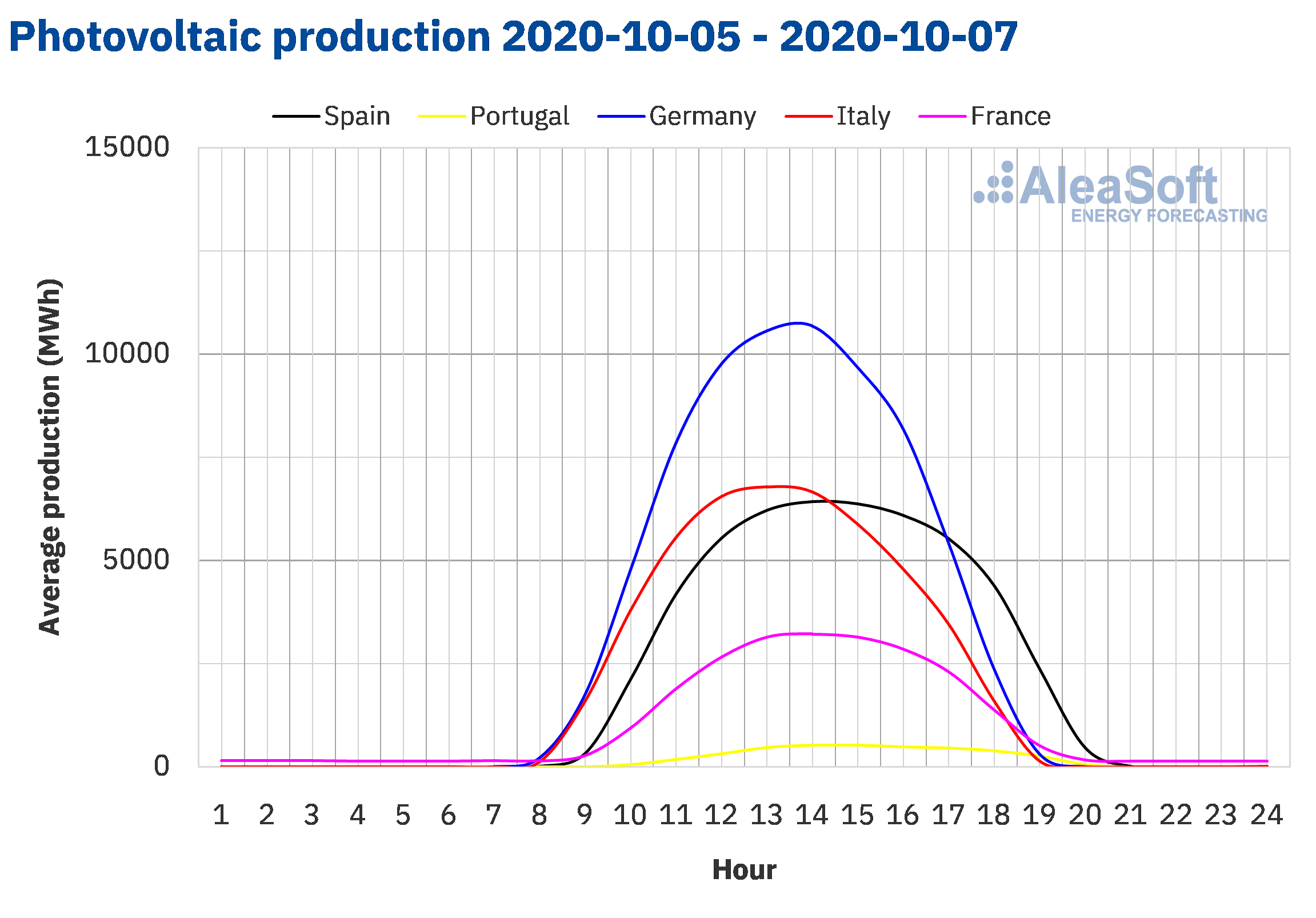

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA.

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA. Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA.

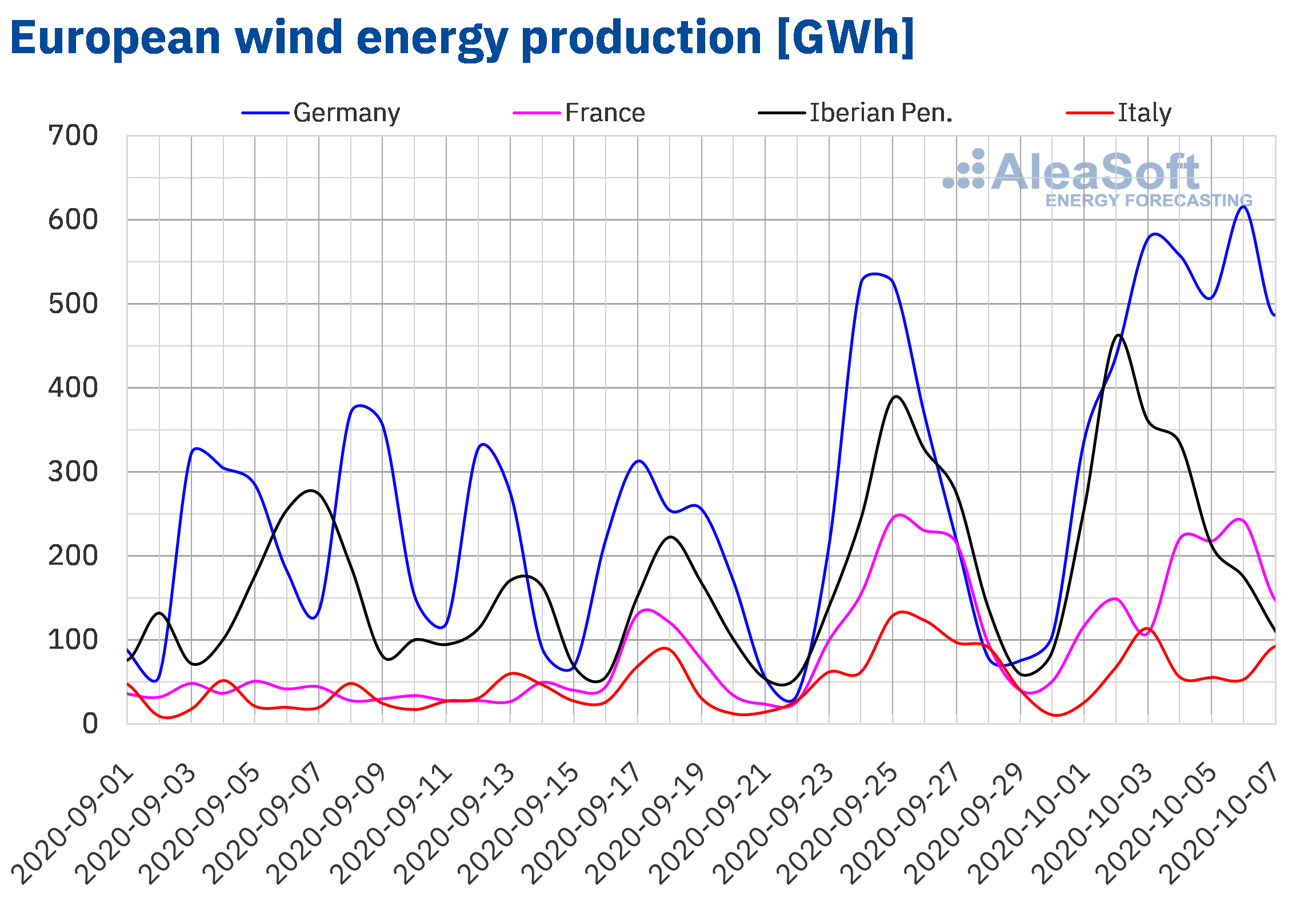

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA.Between Monday and Wednesday of the second week of October, the wind energy production increased in most European markets compared to the average of the previous week. In Germany the rise was 73%, staying upwards for the third consecutive week. The French market registered a recovery of 81%, and the Italian of 16%. On the other hand, in the Iberian Peninsula there was a drop of 32%. This decrease in the Iberian Peninsula was conditioned by the record of maximum daily production for 2020 of Friday, October 2, of the previous week, when in Portugal a value of 99 GWh was registered, which was the highest in 2020 and together with the second highest value of the year in Spain, of 362 GWh, became the highest value of wind energy production in the peninsula for this year. In fact, if the comparison is made with respect to the average of the first three days of the week of September 28, the wind energy production of the Iberian Peninsula increased by 75% during the three analysed days .

In the year‑on‑year comparison for the first seven days of October, the variations behaved upward in most of the analysed European markets. The most significant values occurred in the Iberian Peninsula and Germany, where the increases were 120% and 72% in that order. The French market also had a positive balance, which in this case was 68%. The Italian market registered very similar values, with a difference of only ‑0.1%.

For the end of the week of October 5, the AleaSoft‘s forecasting shows that the production of Germany and France will register increases compared to the previous week. However, the week is expected to end with decreases in production in Italy and the Iberian Peninsula.

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA.

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA.Electricity demand

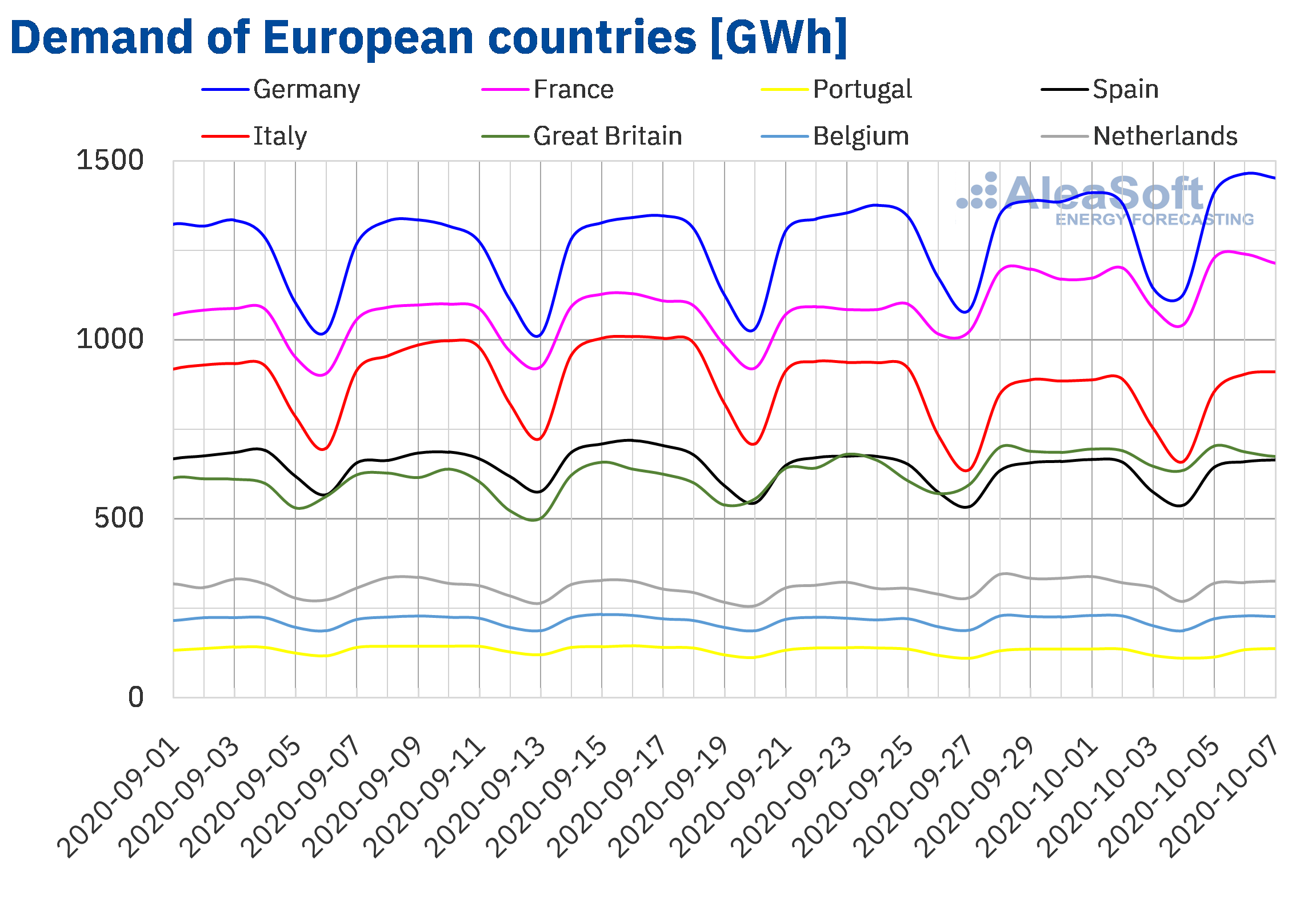

From Monday to Wednesday of the second week of October, the electricity demand behaved heterogeneously compared to the first three days of the previous week in the European electricity markets. In the markets of Spain, Italy and Germany, where the average temperatures of the three days increased slightly compared to the same period of the previous week, the maximum difference being 1 °C, there were increases in demand of between 0.9% of Spain and 4.9% of Germany. In the case of France, the average temperatures were 0.5 °C lower than those of the same period of the first week of October and the demand increased by 3.4%.

On the other hand, in the markets of Great Britain, Belgium, Portugal and the Netherlands, the demand from Monday, October 5, to Wednesday, October 7, fell between 0.4% and 4.3%. In these countries, the average temperatures also fell between 0.2 °C and 2.0 °C, the exception being Great Britain where the average temperatures were very similar to those of the first three days of the week of September 28.

The analysis of the evolution of the demand of the different European markets, together with other variables of interest, can be carried out at the AleaSoft’s observatories.

At AleaSoft, it is expected that, at the end of the second week of October, in most markets the demand will be greater compared to that of the previous week, while in the markets of Belgium, Great Britain and the Netherlands it will continue to be lower.

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE, TERNA, National Grid and ELIA.

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE, TERNA, National Grid and ELIA.Mainland Spain, photovoltaic and solar thermal energy production and wind energy production

In Mainland Spain, the electricity demand increased by 0.9% during the first three days of the week compared to the same period of the previous week and the average temperatures were very similar to those registered between Monday, September 28, and Wednesday, September 30. The AleaSoft‘s demand forecasting indicates that at the end of the week the demand will be very similar to that registered in the first week of October, with a slight increase.

The average solar energy production of Spain increased by 18% from Monday to Wednesday of the week of October 5 compared to the average of the week of September 28. Comparing year‑on‑year, from October 1 to 7, the production with this technology, which includes the solar thermal and photovoltaic technologies, increased by 20%. At the end of the week of October 5, at AleaSoft the total solar energy production is expected to exceed that of the previous week.

The average values of the wind energy production decreased by 30% compared to the previous week. However, if compared to the first three days of the week of September 28, the production increased by 71%. From the year‑on‑year point of view, during the first seven days of October a significant increase was also observed, reaching to double the production registered in this period of 2019, with an increase of 125%. The AleaSoft‘s wind energy production forecasting indicates that in Spain the production will fall at the end of the week of October 5.

The unit II of the Ascó nuclear power plant began a scheduled shutdown to carry out its 26th refuelling on 3 October. The recharge is expected to conclude on November 5. This factor, together with the drop in production at the Cofrentes power plant during October 5, led to a 6.1% decrease in the average nuclear energy production of the first three days of the week compared to the previous week.

Sources: Prepared by AleaSoft using data from REE.

Sources: Prepared by AleaSoft using data from REE.The level of the hydroelectric reserves is currently 10 317 GWh, according to data from the Hydrological Bulletin of the Ministry for Ecological Transition and Demographic Challenge number 40. This value represents a drop of only 0.4% compared to the previous bulletin and 45% of total reserve capacity.

European electricity markets

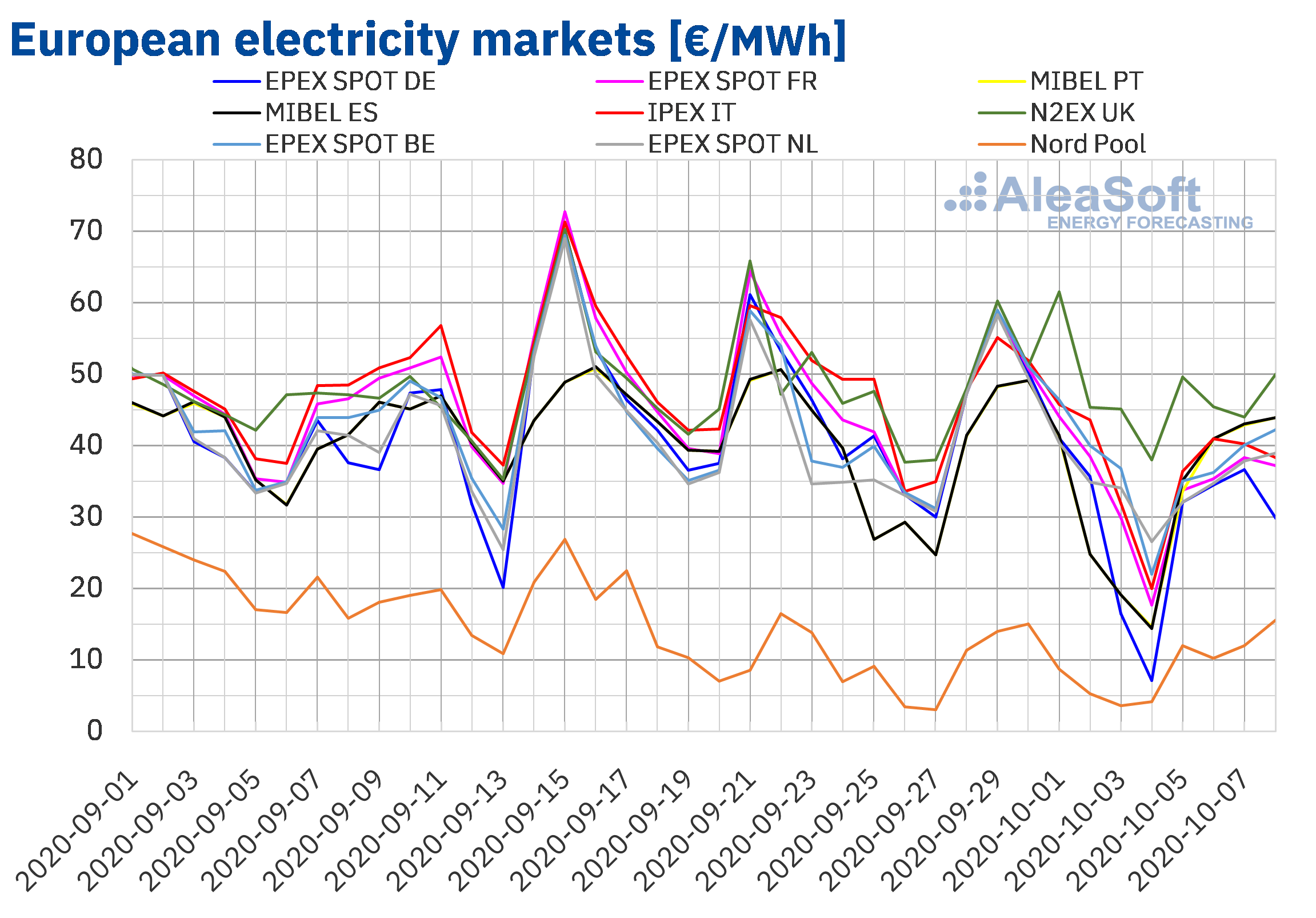

The first four days of the week of October 5, the prices fell in almost all the European electricity markets analysed at AleaSoft compared to the same period of the previous week. The exception was the Nord Pool market of the Nordic countries with a 1.5% price increase. On the other hand, the greatest drop in prices, of 33%, was that of the EPEX SPOT market of Germany. While the MIBEL market of Spain and Portugal and the N2EX market of Great Britain registered the smallest price drops, of 10% and 14% respectively. In the rest of the markets, the decreases were between 22% of the IPEX market of Italy and 28% of the EPEX SPOT market of France.

As a consequence of these price variations, the average for the first four days of the second week of October was below €40/MWh in almost all the analysed European markets, except in the MIBEL and N2EX markets. The highest average price of this period, of €47.25/MWh, was reached in the latter market. On the other hand, the lowest average, of €12.46/MWh, was that of the Nord Pool market, followed by that of the German market, of €33.25/MWh.

The European electricity markets prices began the week of Monday, October 5, quite coupled. The exceptions were the British market, with prices higher than those of the rest, and the market of the Nordic countries, with lower prices. But from October 6 to 8, the coupling decreased.

During the first four days of the second week of October, the daily prices exceeded €40/MWh in the MIBEL, IPEX and N2EX markets and in the EPEX SPOT market of Belgium. The highest daily price, of €49.99/MWh, was reached on Thursday, October 8, in the British market. On the other hand, in the Nord Pool market there were the lowest daily prices, which were between €10.25/MWh of Tuesday, October 6, and €15.59/MWh of Thursday, October 8.

Regarding the hourly prices, in the first four days of the week of October 5, negative hourly prices were not reached in the analysed electricity markets. On the other hand, the highest hourly price, of €88.17/MWh, was reached at the hour 20 of Monday, October 5, in the British market.

Source: Prepared by AleaSoft using data from OMIE, , N2EX, IPEX and Nord Pool.

Source: Prepared by AleaSoft using data from OMIE, , N2EX, IPEX and Nord Pool.The price decreases of the first days of the second week of October were favoured by a significant increase in wind energy production in Europe.

The AleaSoft‘s price forecasting indicates that at the end of the week the prices will continue to be lower than those registered during the week of September 28 in most of the European electricity markets. For the week of October 12, price increases are expected in most of the markets influenced by the decrease in wind energy production.

Iberian market

In the MIBEL market of Spain and Portugal, the average price of the first four days of the week of October 5 decreased compared to the same period of the previous week. The fall was 10% in the Portuguese market and 9.6% in the Spanish. These price drops were the smallest of those registered in the European electricity markets analysed at AleaSoft.

Despite the price drops, the average price from October 5 to 8 was €40.77/MWh in the Spanish market and €40.37/MWh in the Portuguese market. These were the second and third highest prices in the European markets after the one registered in the British market.

On the other hand, the daily prices of the MIBEL market had a growth trend from Monday, October 5, to Thursday, October 8. The minimum price, of €33.64/MWh, was reached on Monday in the Portuguese market. While on October 8 the maximum daily price, of €43.95/MWh, was reached, both in Spain and Portugal.

During the first days of the second week of October, the increase in wind energy production in the Iberian Peninsula and in solar energy production in Spain, compared to the same days of the first week of October, favoured the decrease in prices in this market.

The AleaSoft‘s price forecasting indicates that at the end of the week the prices will be higher than those registered during the week of September 28, while for the next week of October 12 they are expected to fall favoured by an increase in wind energy production.

Electricity futures

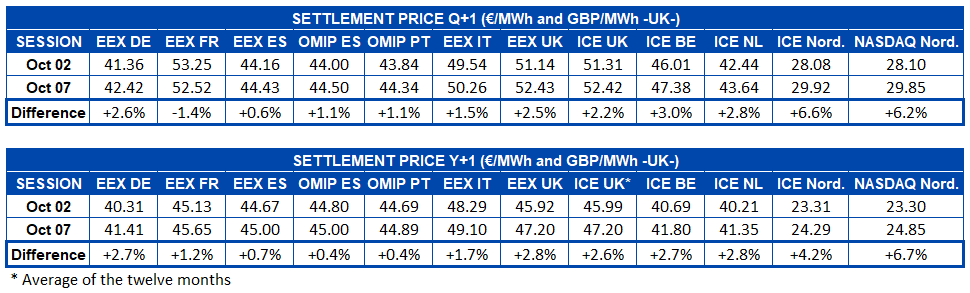

The electricity futures prices for the product of the first quarter of 2021 rose in most of the markets analysed at AleaSoft in the session of Wednesday, October 7, compared to that of Friday of the previous week. The greatest variations were registered in the ICE market of the Nordic countries with an increase of 6.6% and in the NASDAQ market of the same region with 6.2%. The exception was the EEX market of France where the settlement price of the last session was below that of Friday, October 2, by 1.4%. In the rest of the markets there were increases of between 0.6% and 3.0%.

The behaviour of the electricity futures prices for the calendar year 2021 was similar in all markets, the 6.7% increase compared to Friday, October 2, in the NASDAQ market of the Nordic countries standing out. In the ICE market of the Nordic countries the settlement price increased by 4.2%, while in the EEX market of Spain and the OMIP market of Spain and Portugal the variation was 0.4% and 0.7% respectively. In the rest of the markets, the prices increased between 1.2% and 2.8%.

Brent, fuels and CO2

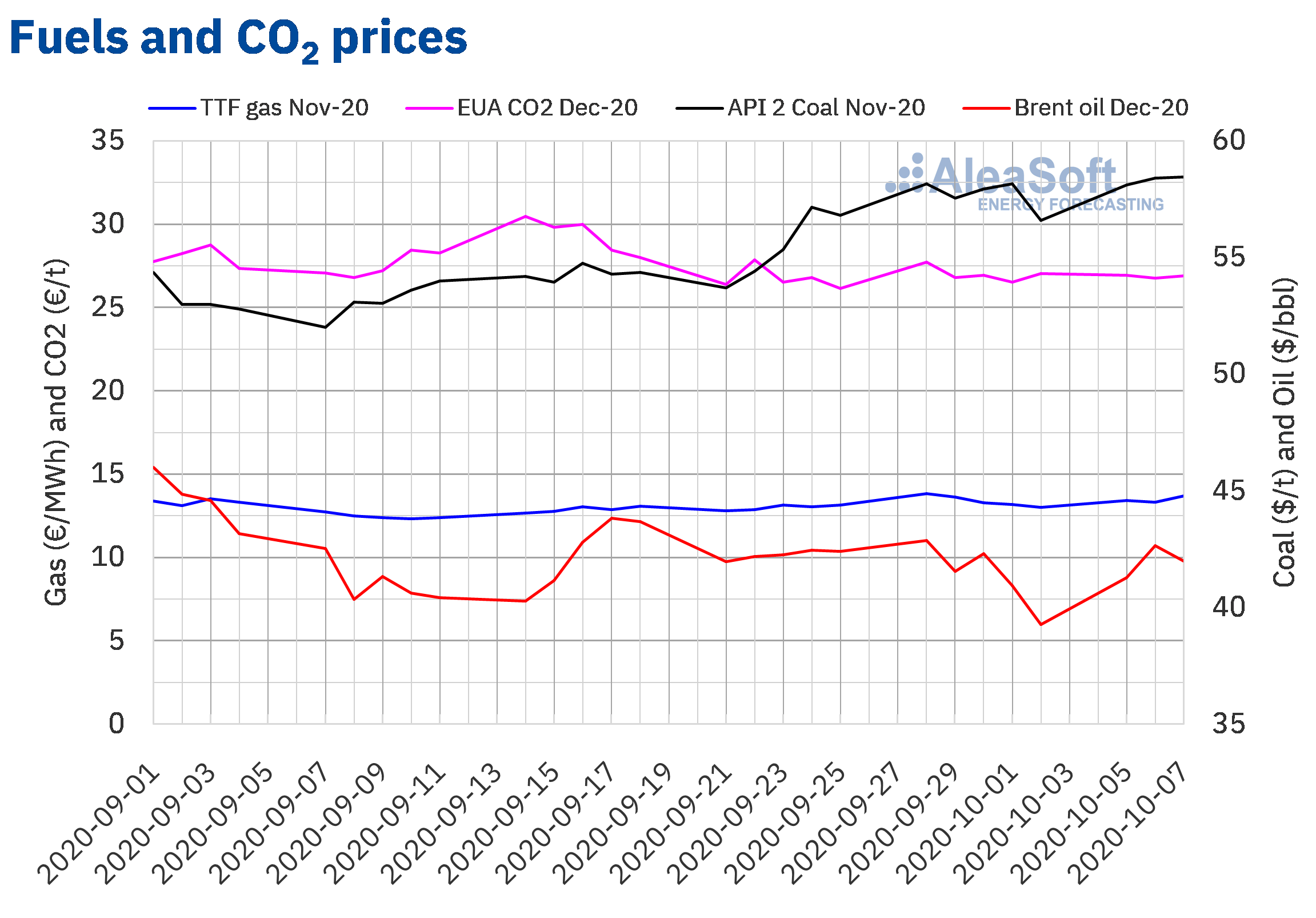

The Brent oil futures for the month of December 2020 in the ICE market began the second week of October with price increases, recovering from the decreases of the previous week. Thus, the settlement price of Tuesday, October 6, was $42.65/bbl, 2.6% higher than that of the previous Tuesday. However, on Wednesday, October 7, there was a decrease of 1.5% and the settlement price was $41.99/bbl.

In the first days of the second week of October, the decline in production in Norway, due to the strikes, and in the Gulf of Mexico, due to the Hurricane Delta, allowed the prices to recover. The price drop of Wednesday was influenced by the US president’s decision to postpone negotiations on new stimulus for the country’s economy until after the November 3 elections. However, later on, he showed favourable to this type of measures, which would support the recovery of the demand.

On the other hand, the effects of the decrease in production in Norway and the Gulf of Mexico may extend in the coming days, favouring the recovery of the prices. In fact, in the intraday session of Thursday, October 8, the prices were above $42/bbl most of the time.

On the other hand, the TTF gas futures prices in the ICE market for the month of November 2020, on Monday, October 5, began to recover from the decreases of the previous week. On Tuesday there was a slight decline of 0.8%. But on Wednesday, October 7, the recovery continued until reaching a settlement price of €13.71/MWh. This price was 3.2% higher than that of the same day of the previous week, but it continued to be lower than €13.82/MWh of Monday, September 28.

Regarding the TTF gas prices in the spot market, the first four days of the second week of October had a generally upward trend. As a result, the index price of Thursday, October 8, was €13.16/MWh. This price is the highest since the first fortnight of December 2019.

As for the API 2 coal futures prices in the ICE market for the month of November 2020, the first three days of the second week of October they increased. As a result, the settlement price of Wednesday, October 7, was $58.45/t. This price was 0.9% higher than that of the same day of the previous week and the highest since January.

Regarding the CO2 emission rights futures prices in the EEX market for the reference contract of December 2020, the first three days of the week of October 5 remained stable below €27/t. The settlement prices ranged between €26.78/t of Tuesday and €26.94/t of Monday.

Source: Prepared by AleaSoft using data from ICE and EEX.

Source: Prepared by AleaSoft using data from ICE and EEX.AleaSoft analysis of the recovery of the energy markets at the end of the economic crisis

On October 8 AleaSoft celebrates 21 years since its foundation. During this period the company has supported the development of the European energy sector with its forecasting products and services. Since the COVID‑19 pandemic began and its effects began to become visible in the energy markets, at AleaSoft it was taken advantage of the experience to carry out informative work on the effects of the energy markets in this situation and the prospects for recovery at the end of the economic crisis caused by the pandemic. Precisely, coinciding with the anniversary of the company, its CEO, Antonio Delgado Rigal, will participate in a webinar organised by APPA Renovables to talk about the long‑term electricity market price curves for renewable energy financing. In addition, on October 29, the second part of the webinar “Energy markets in the recovery from the economic crisis” is being organised to discuss the present and future of the energy markets, but also the renewable energy projects financing in these times of uncertainty due to the coronacrisis, and the importance of the forecasting in the audits and the portfolio valuation, topics that were also covered in the first part of the webinar. On this occasion, there will also be the presence of two invited speakers from the consulting firm Deloitte, Pablo Castillo Lekuona, Senior Manager of Global IFRS & Offerings Services and Carlos Milans del Bosch, Partner of Financial Advisory.

Another tool that was developed at AleaSoft to report on the evolution of the energy markets are the observatories, which allow monitoring the main variables of the European electricity, fuels and CO2 markets through comparative graphs of the recent weeks.

At AleaSoft we continue with the enthusiasm of the first day to face the new stage of energy transition and the renewable energy revolution. To support the sector in achieving these objectives, especially in the current moments of uncertainty due to the economic crisis, the mid and long‑term price curves are periodically updated taking into account the data on the evolution of the economy and the recovery scenarios from the economic crisis.

Source: AleaSoft Energy Forecasting.