AleaSoft, July 27, 2020. In the fourth week of July, the prices of most European electricity markets fell. On Sunday, July 26, there were hours with negative prices in Germany and Belgium. The increase in solar and wind energy production and the drop in demand in most of the markets favoured the decline. However, in the MIBEL market, the prices rose as the demand increased and the renewable energy production decreased. The downward price trend is expected to continue in the last week of July.

Photovoltaic and solar thermal energy production and wind energy production

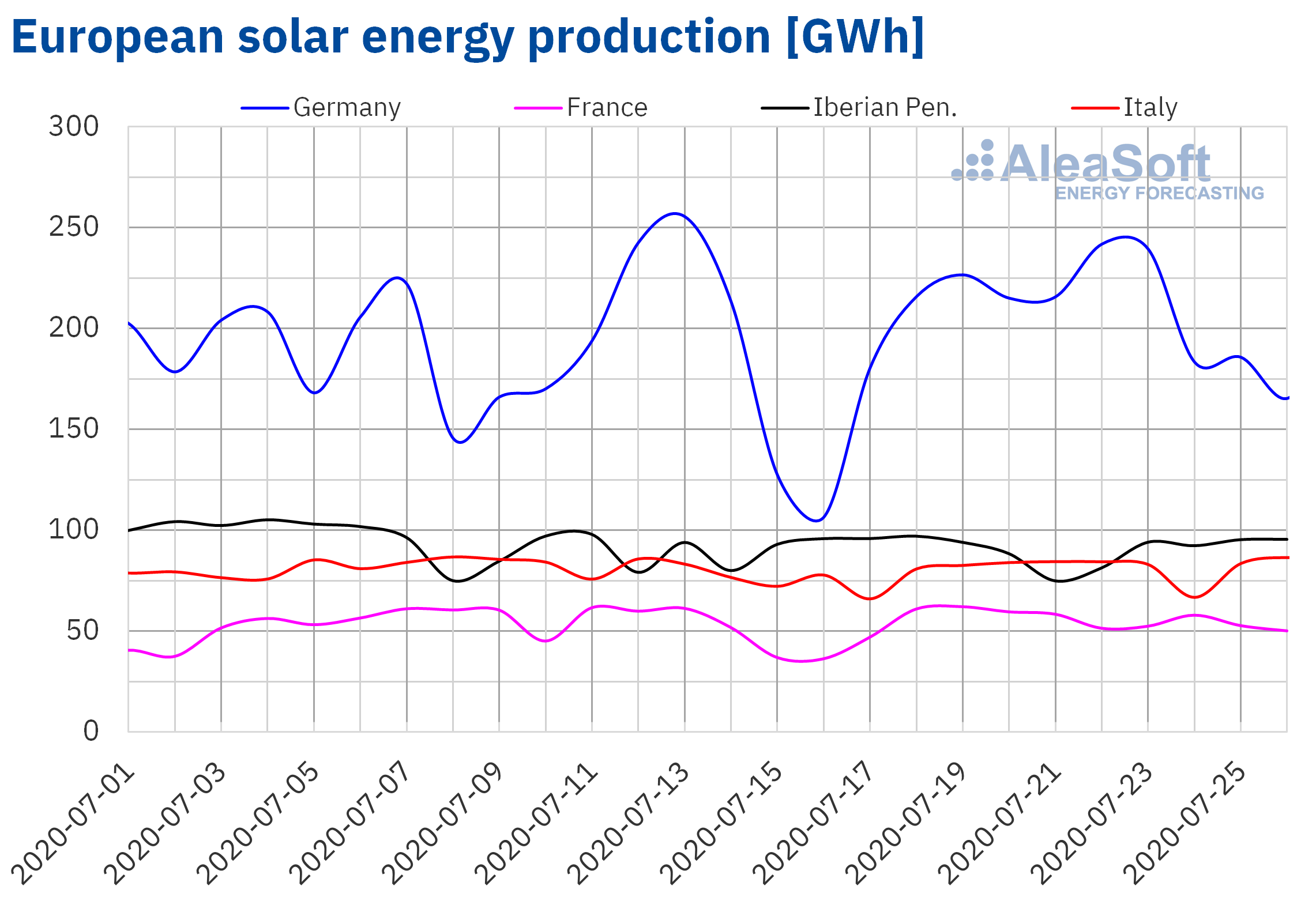

The solar energy production of Europe registered increases in most European markets during the fourth week of July compared to the week of July 13. In Germany, France and Italy the increases were between 6.2% and 9.1%. On the other hand, in the Iberian Peninsula there was a decrease of 4.3%.

During the first 26 days of July, the solar energy production was higher than that of the same days of July 2019 in all the analysed European markets. The most notable increases were those of Spain and Portugal, with values of 61% and 34% respectively. In the case of Germany, France and Italy, the increases were 2.1%, 5.6% and 13% respectively.

The AleaSoft‘s solar energy production forecasting indicates that, at the end of the fifth week of July, the solar energy production of Germany will be higher than that of the week of July 20, while in Spain and Italy the production will be lower.

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA.

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA. Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA.

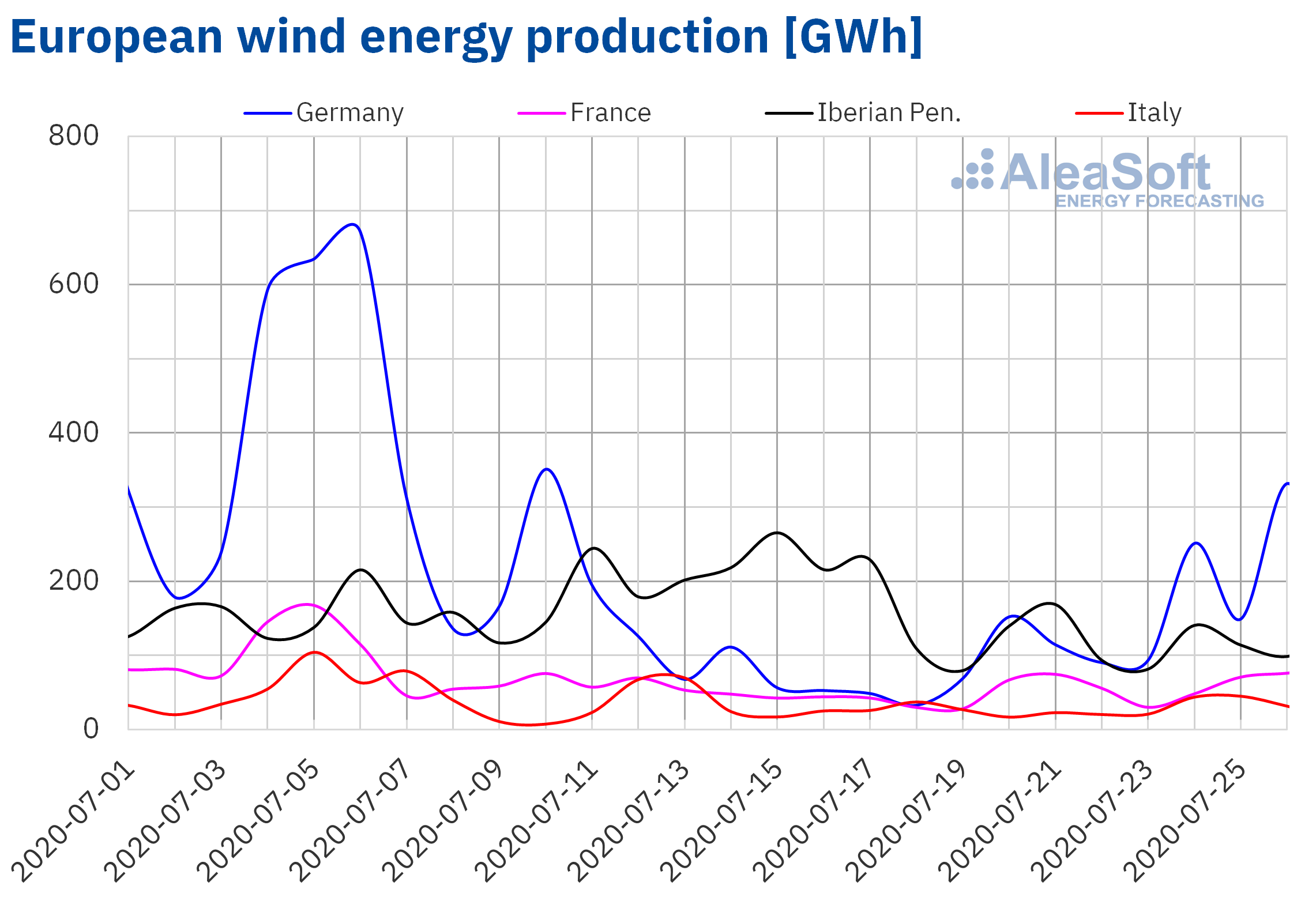

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA.The wind energy production of Germany registered a significant increase, of 169%, during the week of July 20 compared to the third week of July. As for the French market, the generation from this renewable source increased by 46%. However, in Spain and Portugal there were decreases of 40% and 16% respectively and in Italy it fell by 11%.

From July 1 to 26, the production registered increases, in year‑on‑year terms, in most European markets. The largest increases were in Spain, France and Portugal, with values of 34%, 31% and 22% respectively. In Italy the rise was 3.8%, while in Germany the wind energy production decreased by 2.0%.

For the end of the week of July 27 at AleaSoft, the wind energy production is expected to be higher than that of the fourth week of July in the Iberian Peninsula and Germany. On the other hand, a lower wind energy generation is expected for Italy and France.

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA.

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA.Electricity demand

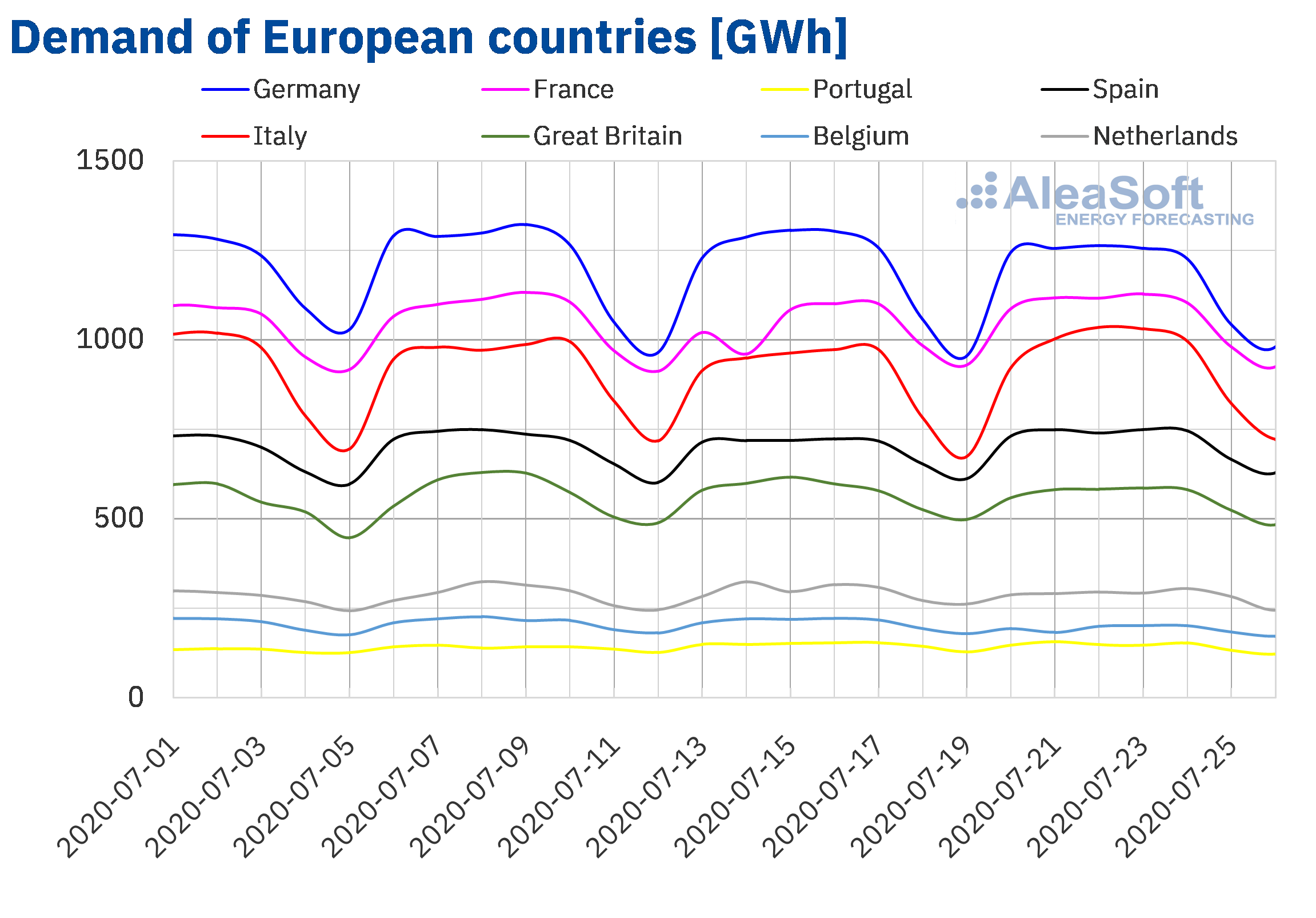

The electricity demand decreased in most European markets during the week of July 20 compared to the third week of the same month. In Belgium the decrease was 8.7% due to the effect of the holiday of Tuesday, July 21, the National Holiday of Belgium. Other markets where declines in demand were registered were those of Great Britain, the Netherlands and Germany, with variations ranging between ‑3.0% and ‑1.5%. The exceptions were the markets of Spain, France and Italy, where the demand increased by 3.1%, 3.9% and 4.9% respectively. In these markets the increase in demand was due to warmer temperatures during the week, at least 1.2 °C above those of the week of July 13. In the case of France, it was also related to the effect of the holiday of Tuesday, July 14, National Day of France, on the demand of the third week of July.

At AleaSoft, the electricity markets observatories are available, which allow monitoring the demand of the main electricity markets in Europe, together with other variables.

The AleaSoft‘s demand forecasting indicates that for the week of July 27 the demand will fall in a large part of the European markets compared to the week of June 20, while in France and Spain it will be higher again.

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE, TERNA, National Grid and ELIA.

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE, TERNA, National Grid and ELIA.European electricity markets

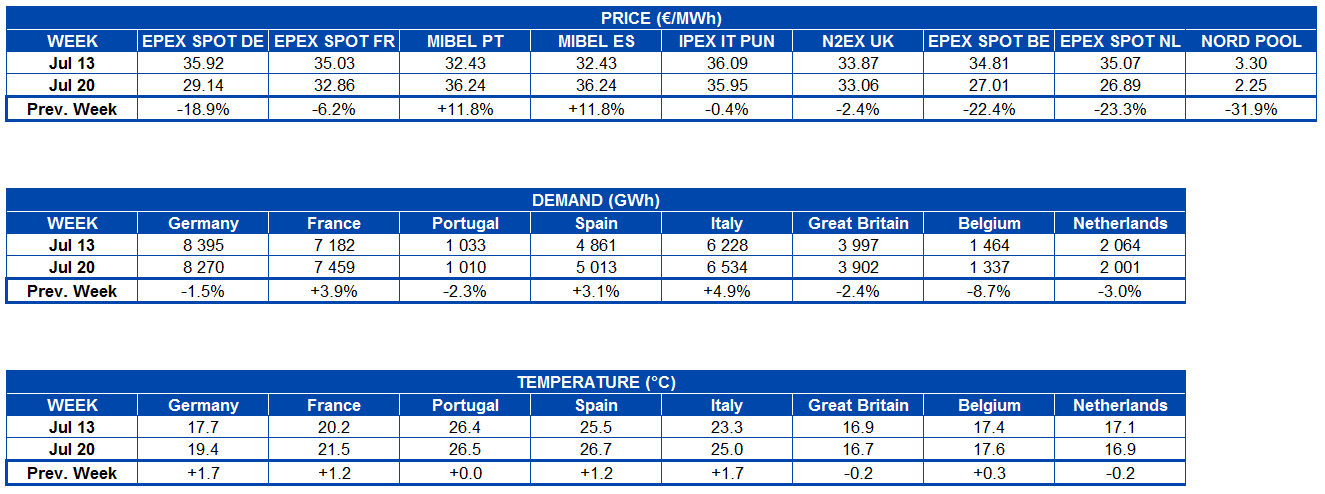

The week of July 20, the prices were lower than those of the week of July 13 in the vast majority of the analysed European electricity markets. The exception was the MIBEL market of Spain and Portugal, where there was an increase of 12%. As for the declines, the market with the largest drop in prices, of 32%, was the Nord Pool market of the Nordic countries, followed by the EPEX SPOT market of the Netherlands and Belgium, with drops of 23% and 22% respectively. While the market where the prices decreased less, by 0.4%, was the IPEX market of Italy. In the rest of the markets, the price drops were between 2.4% of the N2EX market of Great Britain and 19% of the EPEX SPOT market of Germany.

During the fourth week of July, the European market with the lowest average price, of €2.25/MWh, was the Nord Pool market. The average prices of the markets of the Netherlands, Belgium and Germany were €26.89/MWh, €27.01/MWh and €29.14/MWh respectively. In the rest of the analysed markets, the average prices of the week of July 20 were above €30/MWh. The reached values were between €32.86/MWh of the French market and €36.24/MWh of the MIBEL market.

Regarding the daily prices, on Wednesday, July 22, the price exceeded €40/MWh in the MIBEL market. While on July 23, the markets with daily prices above €40/MWh were the MIBEL and the IPEX. That day the highest daily price of the week, of €42.06/MWh, was reached in the Italian market.

In contrast, on Saturday, July 25, the prices were lower than €30/MWh in almost all markets, except in the MIBEL and N2EX markets. On Sunday, July 26, the daily prices were below €30/MWh in all analysed European electricity markets.

The lowest daily prices of the fourth week of July were reached in the Nord Pool market. The prices in this market were between €3.13/MWh of Monday, July 20, and €1.72/MWh of Sunday, July 26. On that day, daily prices lower than €15/MWh were also reached in the German and Belgian markets.

On the other hand, on Sunday, July 26, negative hourly prices were reached in the markets of Germany and Belgium. The lowest hourly price, of ‑€44.97/MWh, was that of the hour 15 in the German market, which was the lowest in this market since the hourly prices reached during the first Sunday of July.

Source: Prepared by AleaSoft using data from OMIE, EPEX SPOT, N2EX, IPEX and Nord Pool.

Source: Prepared by AleaSoft using data from OMIE, EPEX SPOT, N2EX, IPEX and Nord Pool.The increase in solar and wind renewable energy production in most Europe favoured the price drops of the fourth week of July in most of the analysed markets. The electricity demand also decreased in a large part of the markets, which also helped to lower the prices. However, the wind and solar energy production decreased in the Iberian Peninsula, causing price increases in the MIBEL market.

The AleaSoft’s price forecasting indicates that the week of July 27 the prices will drop in most European markets, including the MIBEL market, where the wind energy production is expected to recover. However, the prices are expected to rise in the IPEX market as a consequence of the fall in wind and solar energy production.

Electricity futures

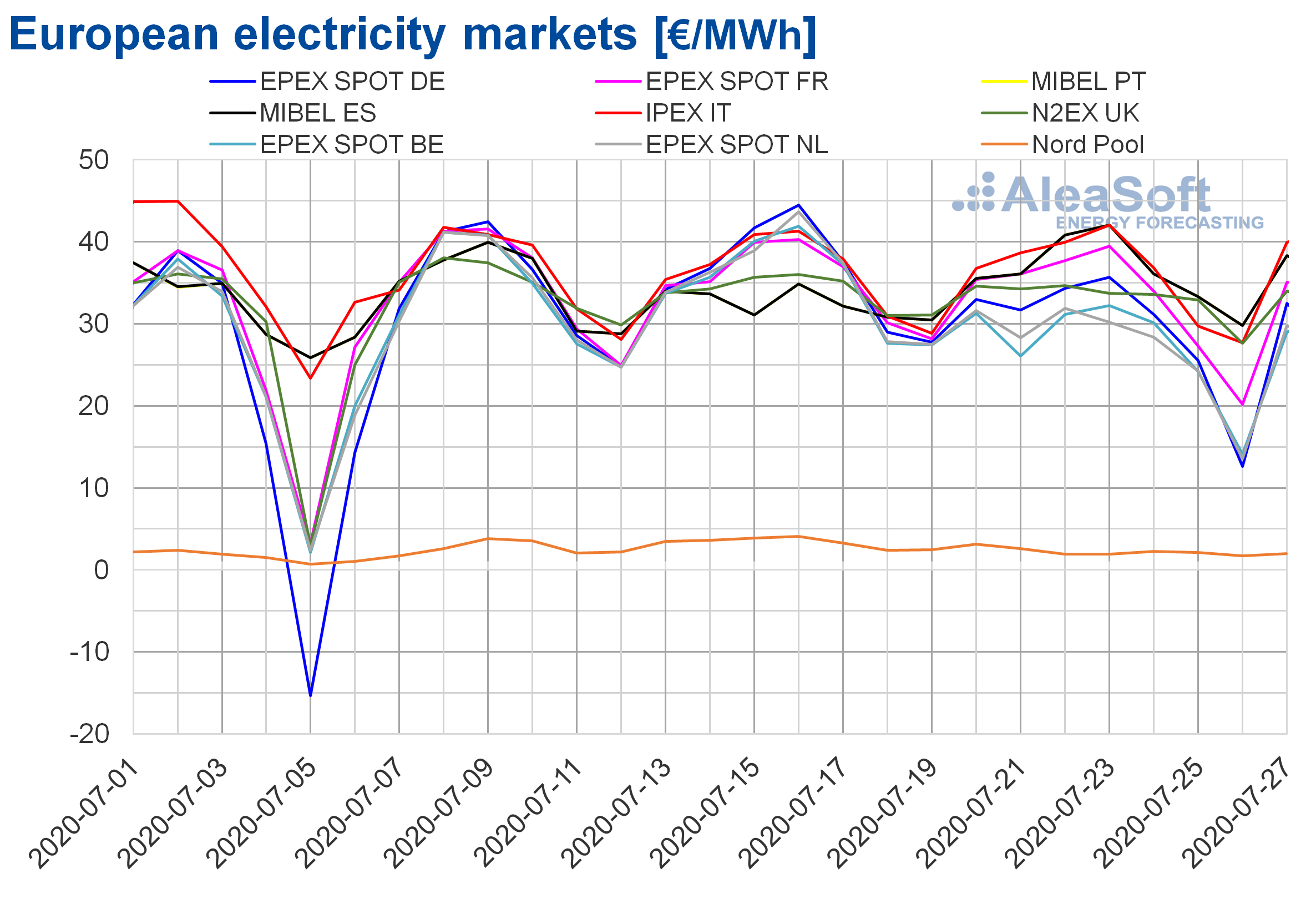

During the week of July 20, the downward trend in the European electricity futures markets continued. The Iberian Peninsula was the region with the least decrease, with a reduction compared to the session of July 17 of 2.5% in the EEX market of Spain and 2.9% in the OMIP market, both for Spain and for Portugal. On the other hand, the ICE market of the Nordic countries was the one that registered the greatest decrease, of 14%. In absolute terms, the most important drop was in the EEX market of France, with a difference of €5.10/MWh.

As for the price for the next year’s product, the behaviour was very similar. In this case, the EEX market of Great Britain led the declines, with a drop of 4.4% compared to the price of the session of July 17. Once again, the Iberian region was the one with the least variation, with decreases of 1.0% in the OMIP market of Spain and Portugal and 0.6% in the EEX market of Spain. In the rest of the markets, the decreases were between 4.2% and 2.4%.

Brent, fuels and CO2

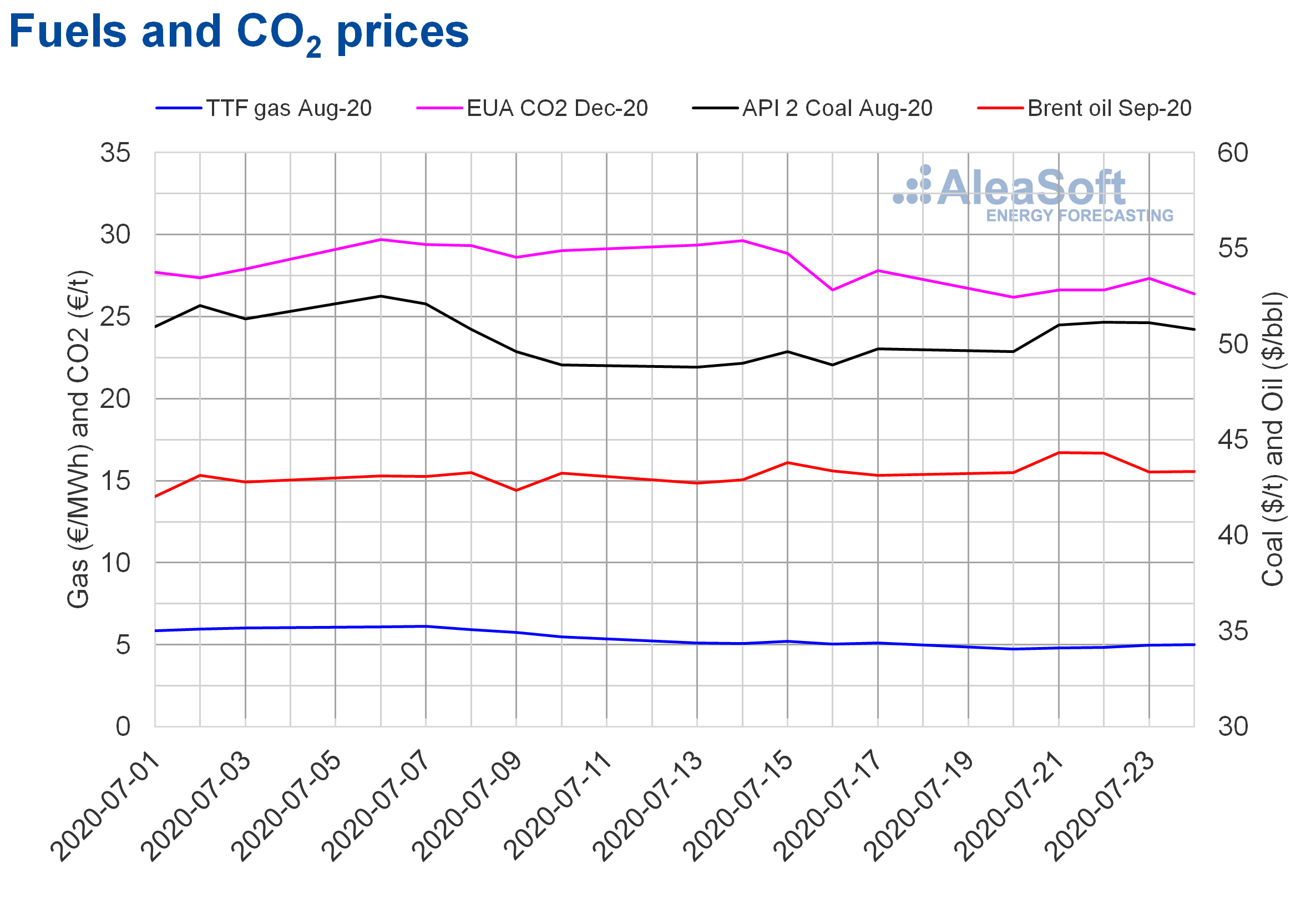

The Brent oil futures prices for the month of September 2020 in the ICE market, the first days of the fourth week of July, increased. As a consequence, on Tuesday, July 21, a settlement price of $44.32/bbl was registered. This price is the highest since early March. But, on Wednesday and Thursday, the prices fell to $43.31/bbl on Thursday, July 23. On Friday, July 24, there was a discreet recovery, reaching a settlement price of $43.34/bbl.

The increase in the number of COVID‑19 infections threatens the recovery in demand, while the production in the United States is recovering and the OPEC+ agreed to start increasing its production in August. This situation is limiting the recovery of the Brent oil futures prices.

As for the TTF gas futures prices in the ICE market for the month of August 2020, on Monday, July 20, they registered a decrease of 7.5% compared to Friday, July 17. That day the settlement price was €4.73/MWh, the lowest since the beginning of June. However, during the week the prices maintained an upward trend and on Friday, July 24, they reached €5.01/MWh.

Regarding the TTF gas in the spot market, on Monday, July 20, the week started with an index price of €4.82/MWh. The following days, the prices fell to €4.61/MWh of Thursday, July 23. But on Friday there was an increase of 6.2% and the maximum index price of the week, of €4.90/MWh, was registered, which was also the highest since €5.17/MWh of Friday, July 10.

On the other hand, the API 2 coal futures prices in the ICE market for the month of August 2020, the fourth week of July, ranged between $49.60/t of Monday, July 20, and $51.15/t of Wednesday, July 22. This price, in addition to being the maximum of the week, was the highest in the last fifteen days.

As for the CO2 emission rights futures in the EEX market for the reference contract of December 2020, the fourth week of July had lower settlement prices than those of the same days of the third week of July and remained below €27/t. The exception was Thursday, July 23. That day a settlement price of €27.34/t was reached, which was 2.7% higher than that of Thursday, July 16. On the other hand, on Monday, July 20, the minimum settlement price of the week, of €26.18/t, was registered, 11% lower than that of Monday, July 13. No settlement price as low as that was registered since late June.

Source: Prepared by AleaSoft using data from ICE and EEX.

Source: Prepared by AleaSoft using data from ICE and EEX.AleaSoft analysis on the effects on the electricity markets due to the coronavirus crisis

At AleaSoft the webinar “Energy markets in the recovery of the economic crisis” is being organised for September 17. On this occasion, the topics to be discussed will be:

- Evolution of European energy markets in the economic recovery

- Financing of renewable energy projects

- Importance of the forecasting in audits and portfolio valuation

To develop these topics, there will be the following speakers:

- Oriol Saltó i Bauzà, Manager of Data Analysis and Modelling at AleaSoft

- Javier Asensio-Marin, CEO at Vector Renewables

- Pablo Castillo Lekuona, Senior Manager of Global IFRS & Offerings Services at Deloitte

- Carlos Milans del Bosch, Partner of Financial Advisory at Deloitte

To monitor the evolution of the energy markets, the observatories were developed at AleaSoft. This tool includes data of the main variables of the European electricity, fuels and CO2 emission rights markets. The information is updated daily and is shown by comparative graphs of the last weeks.

Source: AleaSoft Energy Forecasting.