AleaSoft Energy Forecasting, December 22, 2025. In the third week of December, prices in most major European electricity markets rose slightly compared to the previous week, in many cases exceeding an average of €85/MWh. Higher demand due to colder temperatures and rising gas and CO₂ prices drove this trend, in a context of higher wind energy production and lower photovoltaic energy production. Brent futures registered their lowest settlement price since February 2021, while CO₂ futures reached their highest level since at least October 2024.

Solar photovoltaic and wind energy production

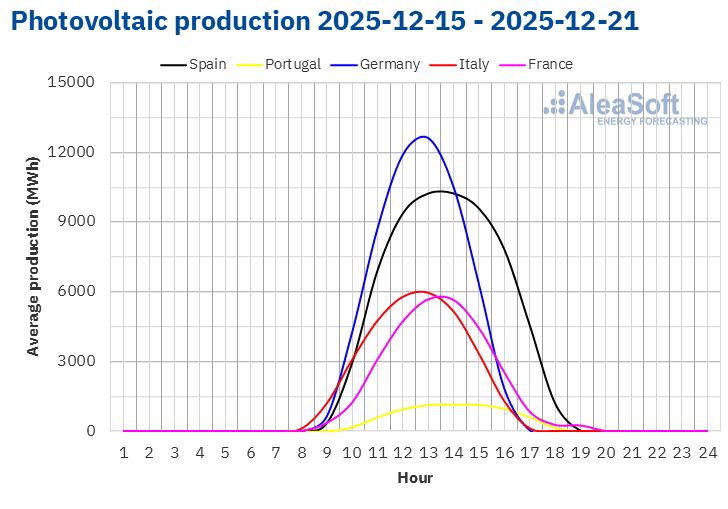

In the week of December 15, solar photovoltaic energy production decreased in most major European electricity markets compared to the previous week. The Italian market registered the largest drop, 41%. The French and Spanish markets followed it with declines of 26% and 19%, respectively. The Portuguese market registered the smallest decrease, 6.7%. The Spanish and Portuguese markets maintained their downward trend for the fourth consecutive week. The German market was the exception to the declines. In this market, the upward trend continued for the third consecutive week and solar energy production increased by 30%.

During the week of December 22, according to AleaSoft Energy Forecasting’s solar energy forecasts, production will increase in the Spanish and Italian markets, while it will decline in the German market.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica and TERNA.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica and TERNA. Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica and TERNA.

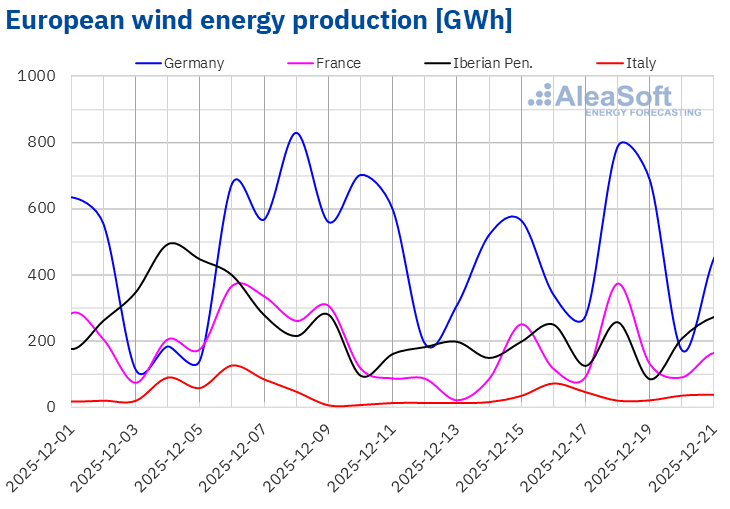

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica and TERNA.During the third week of December, wind energy production increased in most major European markets compared to the previous week. The Italian market registered the largest increase, 132%, reversing the downward trend of the previous two weeks. The French and Spanish markets followed it with increases of 26% and 9.3%, respectively. The Portuguese market registered the smallest increase, 7.9%. The German market was the exception. After one week of upward trend, wind energy production decreased by 12% in this market.

In the week of December 22, according to AleaSoft Energy Forecasting’s wind energy forecasts, production from this technology will increase in the German, French and Italian markets. By contrast, wind energy production will decrease in the Portuguese market, while in the Spanish market it will remain at levels similar to those of the previous week.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica and TERNA.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica and TERNA.

Electricity demand

In the week of December 15, electricity demand increased in most major European markets compared to the previous week, reversing the downward trend observed the week before. The exception was the German market, where demand fell for the second consecutive week, by 3.1%. Meanwhile, the British and Portuguese markets registered the sharpest increases, 4.9% and 7.0%, respectively. By contrast, after three weeks of declines, the French market registered the smallest increase, 1.2%. In the remaining markets, increases ranged from 1.3% in the Belgian market to 2.7% in the Spanish market.

In the third week of December, average temperatures were colder than in the previous week in most analyzed markets. Germany registered the largest drop, 3.4 °C, while France registered the smallest decrease, 0.9 °C. Great Britain and Italy were the exceptions, as average temperatures increased by 0.4 °C and 0.9 °C, respectively.

For the week of December 22, according to AleaSoft Energy Forecasting’s demand forecasts, demand will decline in the main European markets.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica, TERNA, National Grid and ELIA.

Source: Prepared by AleaSoft Energy Forecasting using data from ENTSO-E, RTE, REN, Red Eléctrica, TERNA, National Grid and ELIA.European electricity markets

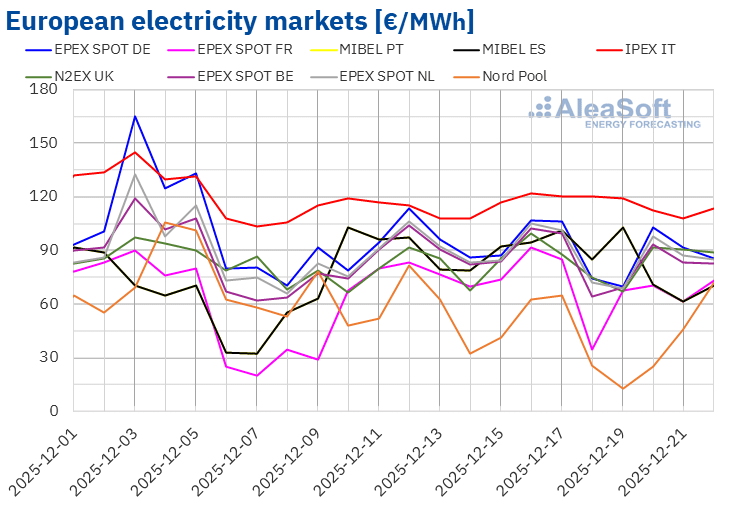

In the third week of December, average prices in most major European electricity markets increased compared to the previous week. The exception was the Nord Pool market of the Nordic countries, which registered a 32% decline. The EPEX SPOT market of Germany registered the smallest price increase, 1.4%, while the N2EX market of the United Kingdom registered the largest percentage increase, 11%. In the rest of the markets analyzed at AleaSoft Energy Forecasting, prices rose between 2.2% in the EPEX SPOT market of Belgium and 9.9% in the EPEX SPOT market of France.

In the week of December 15, weekly averages were above €85/MWh in most European electricity markets. The exceptions were the Nordic market and the French market, with averages of €39.60/MWh and €69.13/MWh, respectively. The IPEX market of Italy registered the highest weekly average, €116.90/MWh. In the rest of the markets analyzed at AleaSoft Energy Forecasting, prices ranged between €85.11/MWh in the Belgian market and €91.35/MWh in the German market.

Regarding daily prices, on Friday, December 19, the Nordic market registered the lowest average of the week among the analyzed markets, €12.54/MWh. This was the only analyzed market that registered daily prices below €30/MWh during the third week of December.

On the other hand, most of the markets analyzed at AleaSoft Energy Forecasting registered daily prices above €100/MWh in some sessions of the third week of December, except for the British, French and Nordic markets. In the Italian market, daily prices exceeded €105/MWh throughout the entire third week of December. This market registered the highest daily average of the week, €121.83/MWh, on Tuesday, December 16.

In the week of December 15, rising gas prices and CO₂ emission allowance prices, as well as increased demand in most markets, led to higher prices in European electricity markets. In the case of the German market, in addition, wind energy production decreased.

AleaSoft Energy Forecasting’s price forecasts indicate that, in the fourth week of December, prices will fall in the main European electricity markets, influenced by lower demand in most markets. In addition, wind energy production will increase in most markets, while solar energy production will rise in the Italian market and in the MIBEL market of Spain.

Source: Prepared by AleaSoft Energy Forecasting using data from OMIE, , Nord Pool and GME.

Source: Prepared by AleaSoft Energy Forecasting using data from OMIE, , Nord Pool and GME.Brent, fuels and CO2

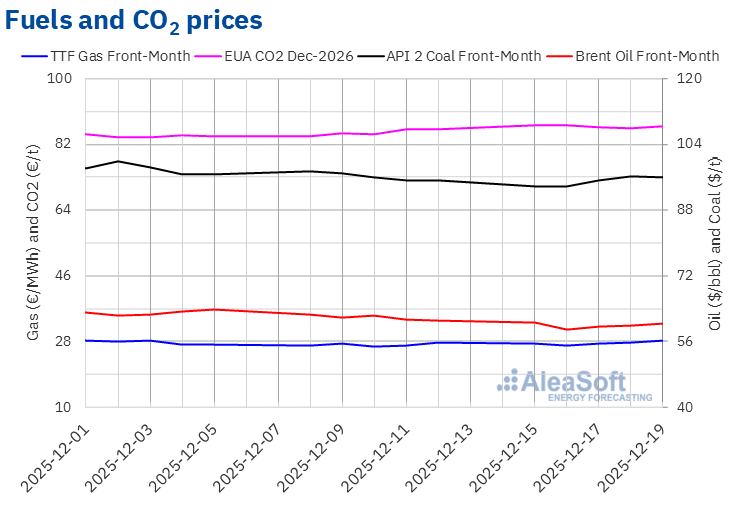

Brent oil futures for the Front‑Month in the ICE market reached their weekly maximum settlement price, $60.56/bbl, on Monday, December 15. This price was already 0.9% lower than that of the last session of the previous week. The downward trend continued until Tuesday, December 16. On that day, these futures registered their weekly minimum settlement price, $58.92/bbl. According to data analyzed at AleaSoft Energy Forecasting, this price was the lowest since February 5, 2021. By contrast, prices began to rise on December 17. As a result of these increases, on Friday, December 19, the settlement price was $60.47/bbl. Nevertheless, this price was still 1.1% lower than that of the previous Friday.

The possibility that the end of the war in Ukraine could lead to increased oil supply from Russia, in a context where global supply levels are already high, exerted downward pressure on Brent oil futures prices in the early sessions of the third week of December. In addition, economic data from China raised concerns about demand evolution, also contributing to the price decline. However, tensions between the United States and Venezuela, as well as Ukrainian attacks on Russian oil infrastructure, contributed to the subsequent recovery in prices.

As for TTF gas futures in the ICE market for the Front‑Month, on Tuesday, December 16, they registered their weekly minimum settlement price, €26.76/MWh. However, in the last three sessions of the week, prices increased. As a result, on Friday, December 19, these futures reached their weekly maximum settlement price, €28.16/MWh. According to data analyzed at AleaSoft Energy Forecasting, this price was 1.7% higher than that of the previous Friday.

In the third week of December, high gas flows from Norway and abundant liquefied natural gas supply continued to exert downward pressure on TTF gas futures prices. The possibility that the end of the war in Ukraine could result in the lifting of sanctions on Russian gas also pushed prices lower. However, forecasts of lower temperatures and reduced wind energy production in January, as well as the shutdown of one of the liquefaction trains at the Freeport export plant on Tuesday, contributed to the price recovery in the last sessions of the week.

Regarding settlement prices of CO2 emission allowance futures in the EEX market for the reference contract of December 2026, they remained above €86/t during the third week of December. On Tuesday, December 16, these futures reached their weekly maximum settlement price, €87.36/t. According to data analyzed at AleaSoft Energy Forecasting, this price was the highest at least since October 1, 2024. Subsequently, prices declined. On Thursday, December 18, these futures registered their weekly minimum settlement price, €86.50/t. By contrast, on Friday, December 19, the settlement price was slightly higher, €87.05/t. This price was 1.2% higher than that of the previous Friday.

Source: Prepared by AleaSoft Energy Forecasting using data from ICE and EEX.

Source: Prepared by AleaSoft Energy Forecasting using data from ICE and EEX.AleaSoft Energy Forecasting’s analysis on the prospects for European energy markets, storage and demand

The 62nd edition of AleaSoft Energy Forecasting’s monthly webinar series will take place on Thursday, January 15. Speakers from PwC Spain will participate for the sixth consecutive year in the January webinar. This webinar will analyze the evolution and prospects from 2026 onward of European energy markets, energy storage and hybridization, as well as the growth in electricity demand driven by Data Centers and industry electrification. In addition, the webinar will address the current state of regulation on PPA and renewable energy, as well as the evolution of virtual PPA and FPA (Flexibility Purchase Agreements).

Source: AleaSoft Energy Forecasting.