AleaSoft, March 12, 2020. The consequences of the coronavirus are beginning to be felt in the European electricity demand. According to AleaSoft estimates, in February the demand of Italy was 1.8% lower than expected and the effect has continued to be observed in March. The IMF lowered the growth forecasts for the Spanish economy due to the same reason, so the demand is expected to drop in the coming months. Today the Brent oil price fell again after the WHO declared the global pandemic situation.

Photovoltaic and solar thermal energy production, wind energy production and electricity demand

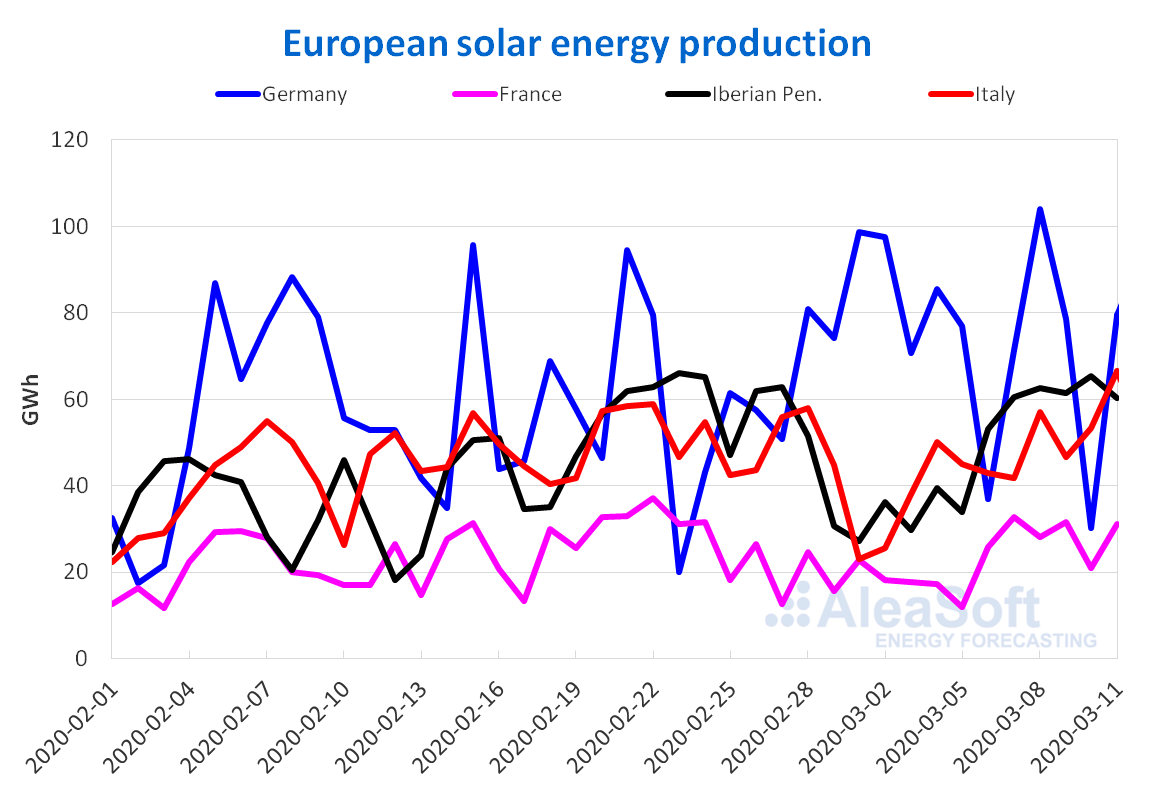

Between Monday and Wednesday of this week, the solar energy production in the Iberian Peninsula registered an increase of 38% compared to the average of the previous week. Similar increases occurred in the markets of France and Italy that generated 29% more this week in both cases. On the other hand, in the German market the production with this technology decreased by 19% this week.

In the year‑on‑year analysis, until the 11th of this month, the solar energy production in the Iberian Peninsula and in the German market increased by 39% and 17% respectively, compared to the same period of the previous year. On the contrary, so far this month the production decreased in the markets of Italy and France by 10% and 4.7% respectively if it is compared to that of the same days of last year.

At AleaSoft, the solar energy production at the end of this week is expected to increase in Germany and Italy compared to that of the week of March 2.

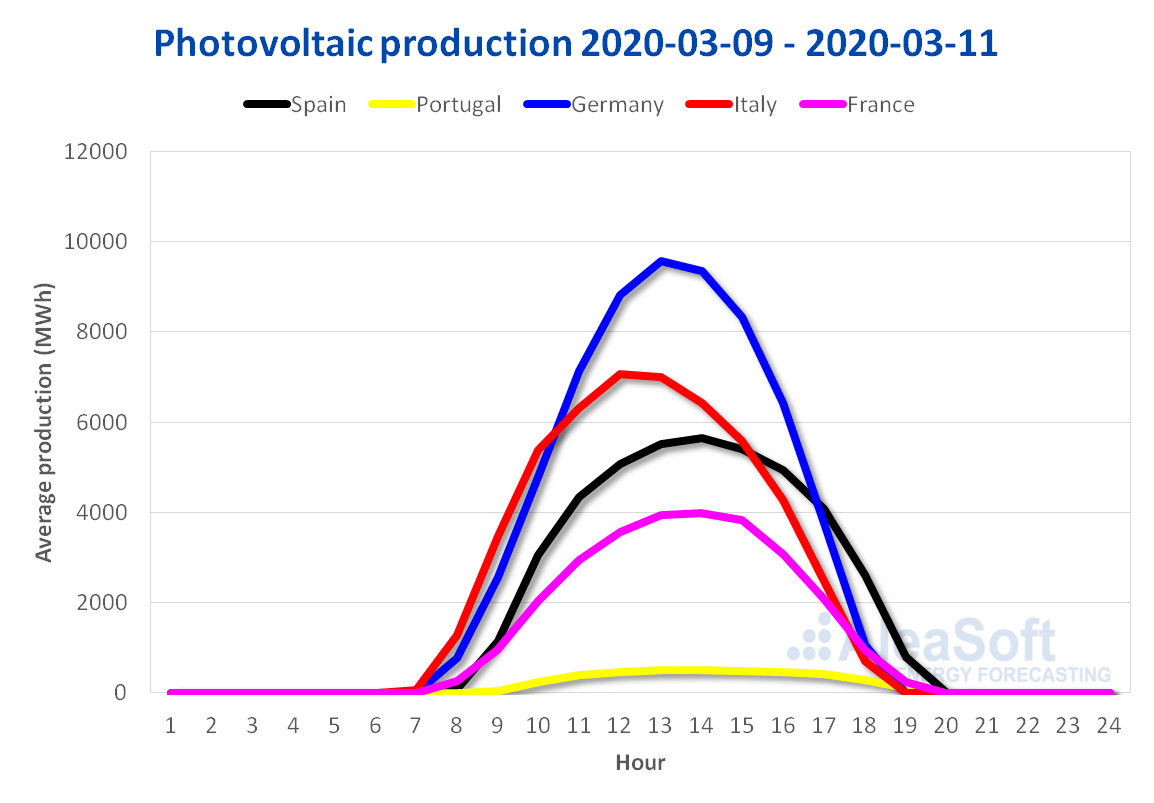

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA.

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA. Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA.

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA.The wind energy production in the German market increased by 75% during the first three days of this week compared to the average of the previous week. The French market also registered an increase in production with this technology of 57%. On the contrary, in the Iberian Peninsula and Italy the wind energy generation from Monday to Wednesday of this week was 56% lower in each case.

During the first 11 days of March, the wind energy production registered year‑on‑year increases of 69% and 15% in the Iberian Peninsula and Italy. On the contrary, in Germany and France it decreased by 26% and 10% respectively.

At AleaSoft, the wind energy production in Germany and France is expected to decrease later this week, but at the end of the week it will be higher than that of last week. On the other hand, in Italy and the Iberian Peninsula at the end of the week, the production will be less than that of last week, although a slight recovery is expected later this week.

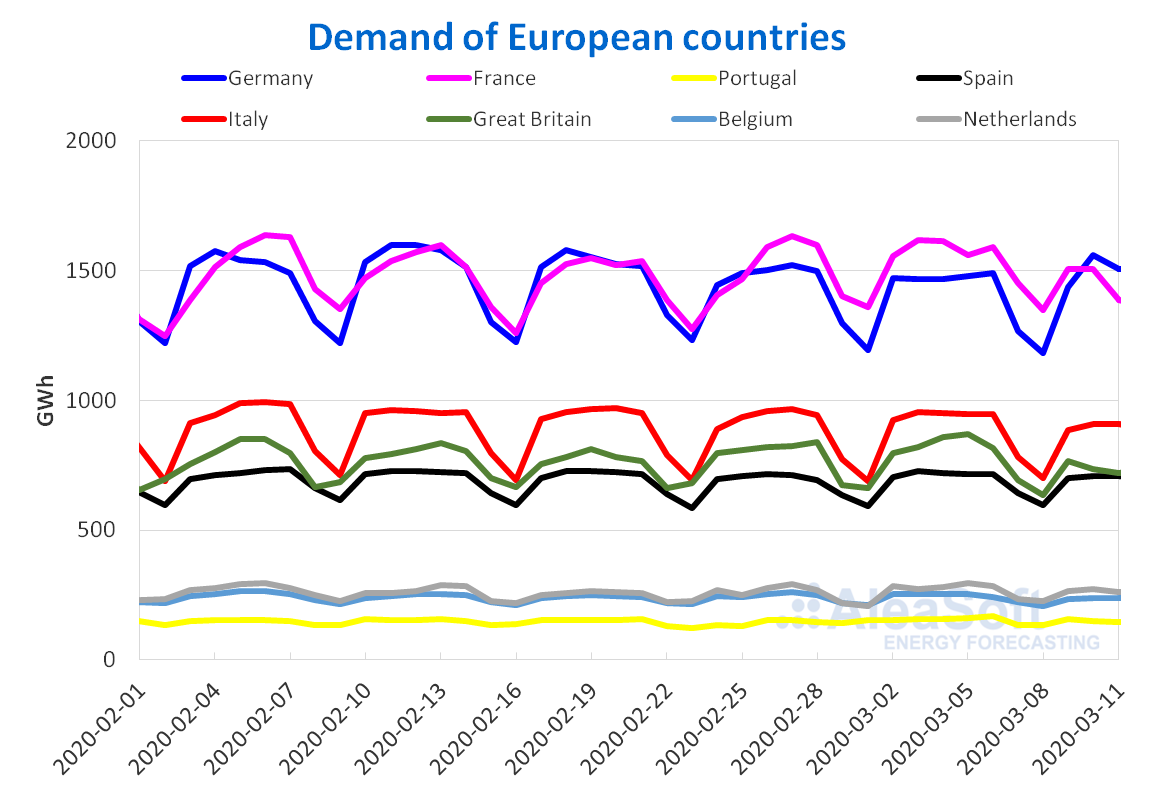

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA.As for electricity demand, the German market is the only one where it was higher so far this week, compared to the same period the previous week. In Italy, the electricity demand had a 4.6% reduction in the same period. This decrease is favoured by the measures that Italy took to contain the expansion of the coronavirus in its territory, which currently ranks third worldwide in terms of the number of infected, and the consequences of this on its economy. According to AleaSoft estimates, for this reason the demand in Italy in February was 1.8% lower than expected. Considering that the containment measures continue and that they are being more restrictive, it is expected that the electricity demand of this country will continue to decrease. In the rest of Europe, the demand also fell, mainly because the temperatures were less cold than during the same days of last week, although it is possible that the effects of the coronavirus are also beginning to be noticed in these countries. In general, in Europe a decrease in demand is expected in the coming months associated with the stagnation of the economy, with the measures to contain the spread of the coronavirus acting as a catalyst.

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE, TERNA, National Grid and ELIA.

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE, TERNA, National Grid and ELIA.Mainland Spain, renewable energy production

The solar energy production in Mainland Spain, which includes photovoltaic and solar thermal energy, increased by 40% during the first three days of this week compared to the average of the previous week. Comparing the first 11 days of March with the same period of 2019, the generation from this renewable source was 40% higher. The analysis carried out at AleaSoft indicates that this week the solar energy production will rise compared to last week’s total.

In contrast, the wind energy production of Mainland Spain this week fell 50% in the period between Monday and Wednesday compared to the average of the previous week. This result contrasts with those obtained during the current month, when 70% more than last year in the same period was produced until now. At AleaSoft, the wind energy production is expected to end up being lower this week compared to the previous week.

The electricity demand in the Spanish market fell 1.9% from Monday to Wednesday of this week compared to the same period of the previous week. The IMF lowered the growth forecasts for the Spanish economy due to the coronavirus, so at AleaSoft the electricity demand is expected to decrease in the coming months for this reason.

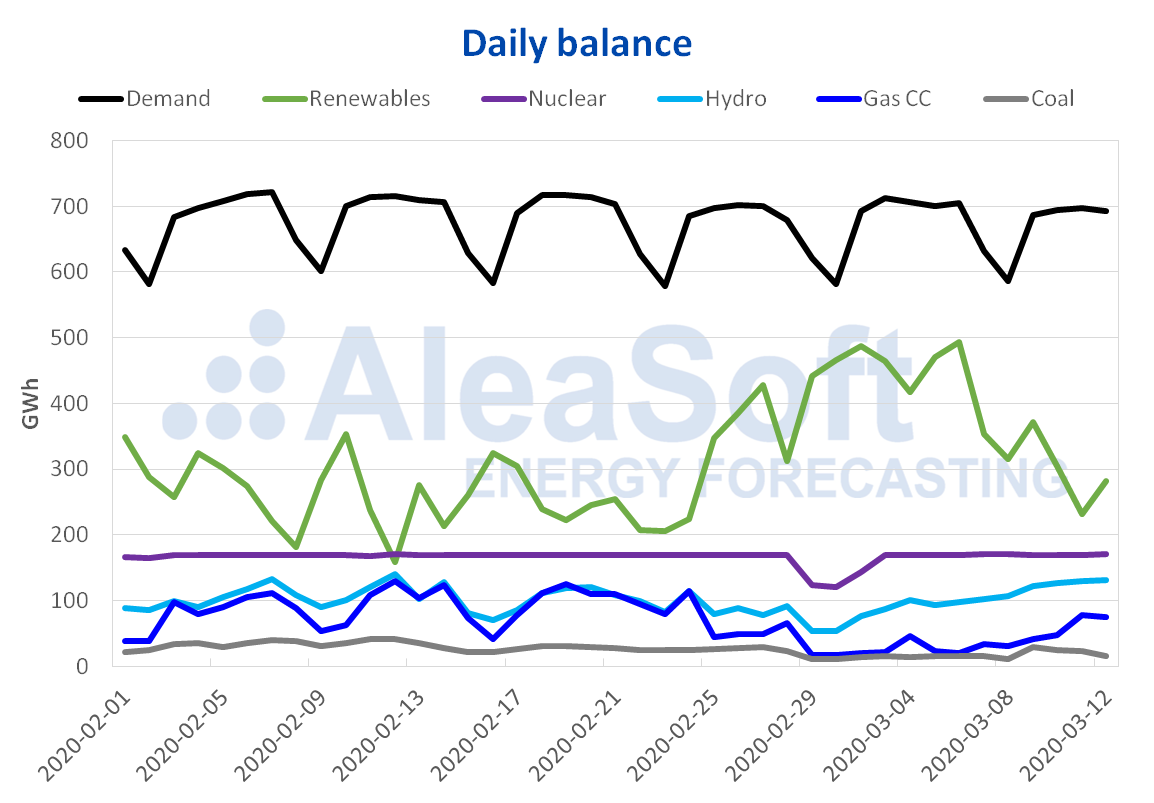

The daily nuclear energy production recovered its usual levels of 170 GWh, after falling from February 29 to March 2 due to lower demand and the high wind and renewable energy production during those days.

Sources: Prepared by AleaSoft using data from REE.

Sources: Prepared by AleaSoft using data from REE.The hydroelectric reserves currently have 13 314 GWh stored, representing an increase of 3.0% compared to the previous bulletin, according to data from the last Hydrological Bulletin of the Ministry for the Ecological Transition and the Demographic Challenge.

European electricity markets

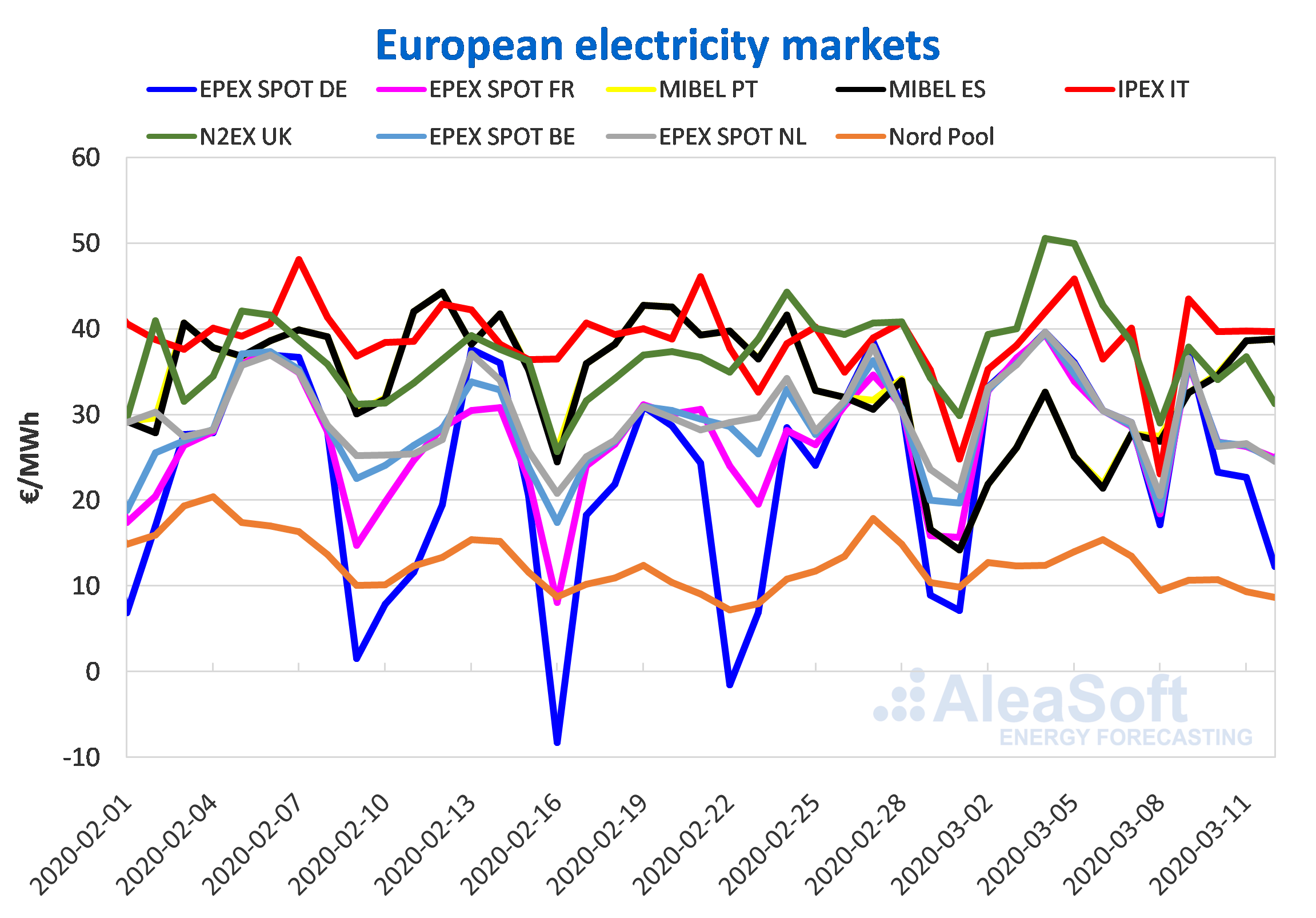

During the first four days of this week, the prices in most European markets decreased compared to the same days of last week. The EPEX SPOT market of Germany was the one with the greatest decrease, of 34%, with negative and close to zero prices at different hours for March 11 and 12 due to the high wind energy production registered since Tuesday. The EPEX SPOT markets of France, Belgium and the Netherlands had declines of around 21% and were quite coupled. In the N2EX market of Great Britain and the Nord Pool market of the Nordic countries, the prices also showed downward variations of 22% and 23% respectively. The exceptions to this behaviour were the MIBEL market of Spain and Portugal and the IPEX market of Italy. In the MIBEL market there was an increase of 37% while the Italian market was that where the price changed the least, being higher than the homologous days of the week of March 2 by only 0.9%, which is equivalent to a difference of €0.36/MWh.

The Nord Pool market of the Nordic countries continues to be the lowest‑priced market in most sessions, settling this Thursday, March 12, with the lowest average price for this market so far this month, of €8.66/MWh. On the contrary, the IPEX market, which during the first five days of the month was replaced by the N2EX market as the market with the highest prices, recovered its position on Monday, March 9, with an average price of €43.46/MWh and during the following days it had prices close to €40/MWh.

The decreases in the prices of the EPEX SPOT market of Germany and France so far this week compared to the previous week, were supported by the increase registered in the wind energy production of these markets since Tuesday, March 10, and by the decrease in demand compared to the same days of the week of March 2.

At AleaSoft, it is expected that for the rest of the days of this week, the prices will recover in the markets where they fell during the first four days of this week, although once the week is over, the average price will continue to be lower than that of last week. This change in trend will be due to lower wind energy production in the coming days. On the other hand, the markets where the prices increased at the beginning of this week will have an inverse behaviour for the rest of the days, but at the end of the week they will continue to be higher than those of the week of March 2.

Source: Prepared by AleaSoft using data from OMIE, , N2EX, IPEX and Nord Pool.

Source: Prepared by AleaSoft using data from OMIE, , N2EX, IPEX and Nord Pool.Iberian market

So far this week, the MIBEL market of Spain and Portugal, with average prices of €36.12/MWh and €36.18/MWh respectively, went from being the second and third lowest‑priced markets in the week of March 2 to occupy the same positions, but as the markets with the highest prices in Europe. Due to lower wind energy production in the first three days of this week, the prices in these markets increased by around €10/MWh compared to the same days of last week. The prices in both countries were between €32/MWh and €39/MWh from Monday to Thursday of this week and converged most of the time, except on Tuesday, March 10, when the average price of the Spanish market was lower than that of the Portuguese market by €0.24/MWh. This March 12, the highest price so far in March was reached, of €38.78/MWh.

For the rest of the days of the week, at AleaSoft the prices of the Iberian market are expected to decrease again due to a slight recovery in wind energy generation, as well as lower electricity demand over the weekend. Even so, according to AleaSoft forecasts, at the end of the week the average price of this market will continue to be higher than last week’s average.

Electricity futures

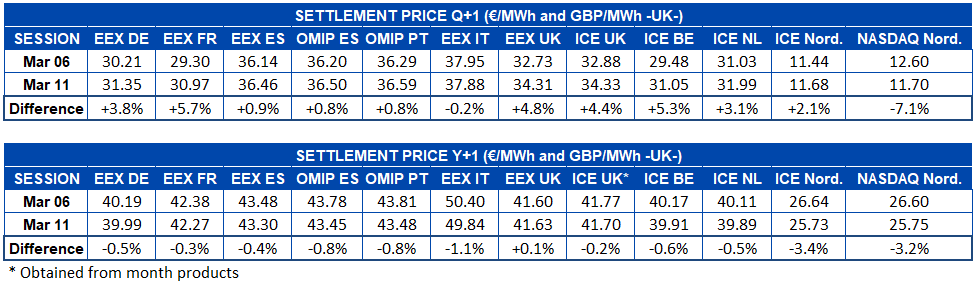

The electricity futures prices for the next quarter still do not show symptoms of being affected by the effects of the coronavirus pandemic. In the elapsed days of this week, from March 9 to 11, the prices registered increases in most European markets. The exceptions were, on the one hand, the EEX market of Italy, which registered a price of €37.17/MWh on Monday 9 and in the following two days recovered to €37.88/MWh, but remains at 0.2% below the settlement price of Friday, March 6. On the other hand, the NASDAQ market of the Nordic countries registered a drop of 7.1%, which corresponds to a difference of €0.90/MWh compared to the previous Friday. The price of this market stood at just €0.02/MWh above the ICE market of the same region, which registered an increase of 2.1%.

The outlook for the electricity futures for the 2021 calendar year is practically the opposite. Only the EEX market of Great Britain registered a rise of just 0.1% compared to the end of the week of March 2. Meanwhile, the rest of the markets analysed at AleaSoft registered declines of between 0.2% and 3.4%.

Brent, fuels and CO2

The Brent oil futures for the month of May 2020 in the ICE market, on Monday, March 9, registered a decrease of 24% compared to the price of Friday and 34% compared to Monday of last week, reaching a settlement price of $34.36/bbl. However, on Tuesday the price rose 8.3% from the previous day. On Wednesday it fell again by 3.8% to $35.79/bbl. This Thursday, March 12, the prices dropped, registering values around $34/bbl and even lower.

The declaration by the World Health Organisation of the global coronavirus pandemic situation and the suspension of flights from Europe to the United States caused the prices to fall again after the recovery of Tuesday. The drop in demand associated with the expansion of the coronavirus may continue to cause price drops in the coming days. On the other hand, after the failure of the OPEC+ negotiations last week, Russia, Saudi Arabia and the United Arab Emirates announced their intention to significantly increase their oil production from April, which will also favour the decrease in oil prices.

In the case of the TTF gas futures prices in the ICE market for the month of April 2020, on Monday, March 9, they reached a settlement price of €8.63/MWh, which was €0.02/MWh lower than that of the previous Friday. However, the following days, the prices recovered, registering increases of 4.2% compared to the previous day, both on Monday and Wednesday. Thus, the settlement price for this Wednesday was €9.37/MWh, 5.1% higher than that of Wednesday of last week and the highest so far this month. This Thursday the prices are lower, staying below €9.20/MWh.

The TTF gas prices in the spot market, the first days of this week remained around €9/MWh. The lowest index price since the first half of October 2019, of €8.70/MWh, was reached on Tuesday, March 10. While today the highest price so far this week, of €9.20/MWh, was registered.

As for the API 2 coal futures in the ICE market for the month of April 2020, on Monday, March 9, the lowest settlement price of the last two years, of $47.25/t, was registered. But, on Tuesday and Wednesday, the prices were higher, of $47.75/t and $47.70/t respectively.

The CO2 emission rights futures in the EEX market for the reference contract of December 2020, on Tuesday, March 10, reached the maximum settlement price so far this month, of €24.09/t. This Wednesday the decrease compared to the previous day was less than 1%, with a settlement price of €23.92/t.

Source: AleaSoft Energy Forecasting