AleaSoft, October 15, 2020. The prices of most of the European electricity markets recovered in the third week of October after the falls that were registered in the first days of the month. These increases were favoured by the decrease in wind energy production in markets such as Germany and France and the increase in demand in most of the markets. The TTF gas prices remain above €13/MWh and in the spot market they reached the highest value since the first half of December.

Photovoltaic and solar thermal energy production and wind energy production

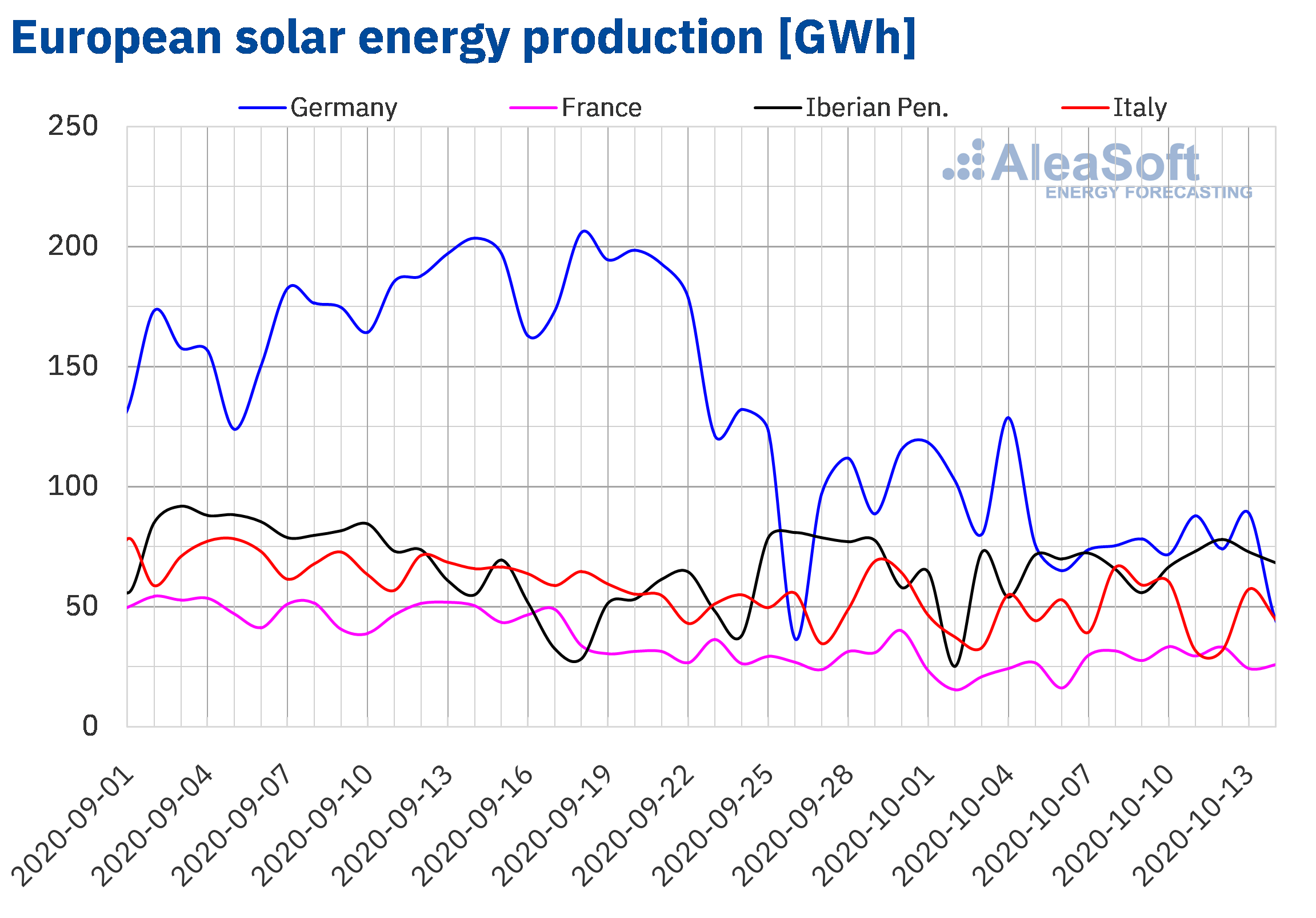

The average solar energy production of the first three days of the week that began on Monday, October 12, decreased by 12% in the Italian market compared to the week that preceded it, while in the German market it fell by 8.4%. In the French market, the average of these periods remained unchanged and in the Iberian Peninsula it increased by 7.7%.

During the first 14 days of October, the solar energy production grew by 42% in the Iberian Peninsula compared to the same days of 2019. In this period there was an increase of 1.0% in the German market, while in the Italian and the French it fell by 2.8% and 4.4% respectively.

For the week ending on Sunday, October 18, the analysis carried out at AleaSoft indicates that the solar energy production will be lower than that registered during the second week of October for most markets.

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA.

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA. Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA.

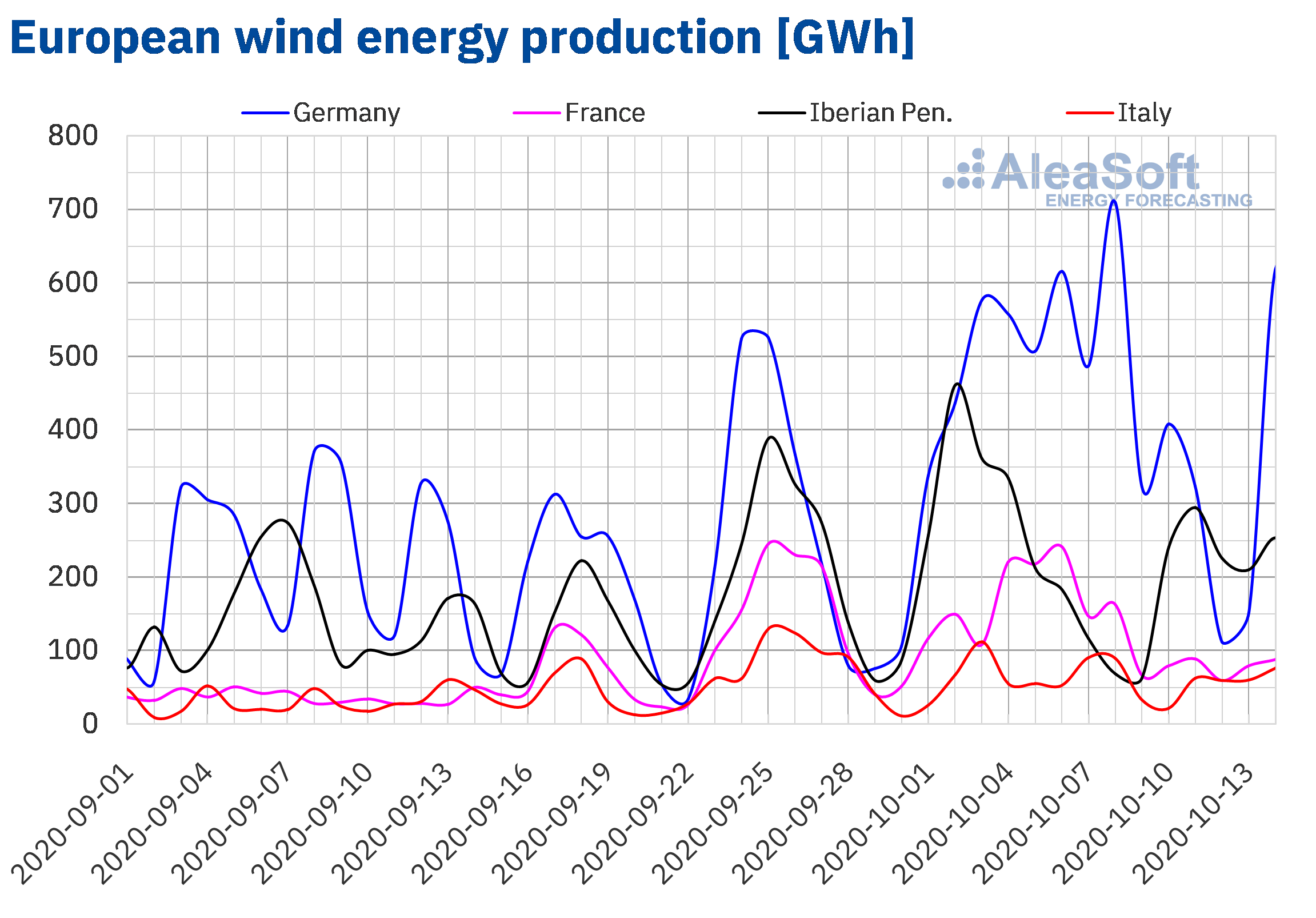

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA.The wind energy production from October 12 to 14 performed unevenly in the electricity markets of Europe compared to the average of the previous week. In the French market it fell by 47%, while in the German market the production with this technology decreased by 39% after having increased for three consecutive weeks. On the contrary, in the Italian market the production grew by 12% and in the Iberian Peninsula there was an increase of 36%.

In the year‑on‑year analysis, during the first 14 days of October, the production with this technology increased in all the European markets analysed at AleaSoft. The smallest percentage increase was registered in the German market, where the production grew by 3.9%. On the opposite side there is the Iberian Peninsula, where there was an increase in wind energy production of 53%. In the markets of France and Italy it increased by 9.1% and 16% respectively.

For the end of the third week of October, the AleaSoft‘s analysis indicates that the total wind energy production of the week will be higher in the markets of the Iberian Peninsula and Italy, while on the contrary, a reduction in production is expected in France and Germany.

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA.

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA.Electricity demand

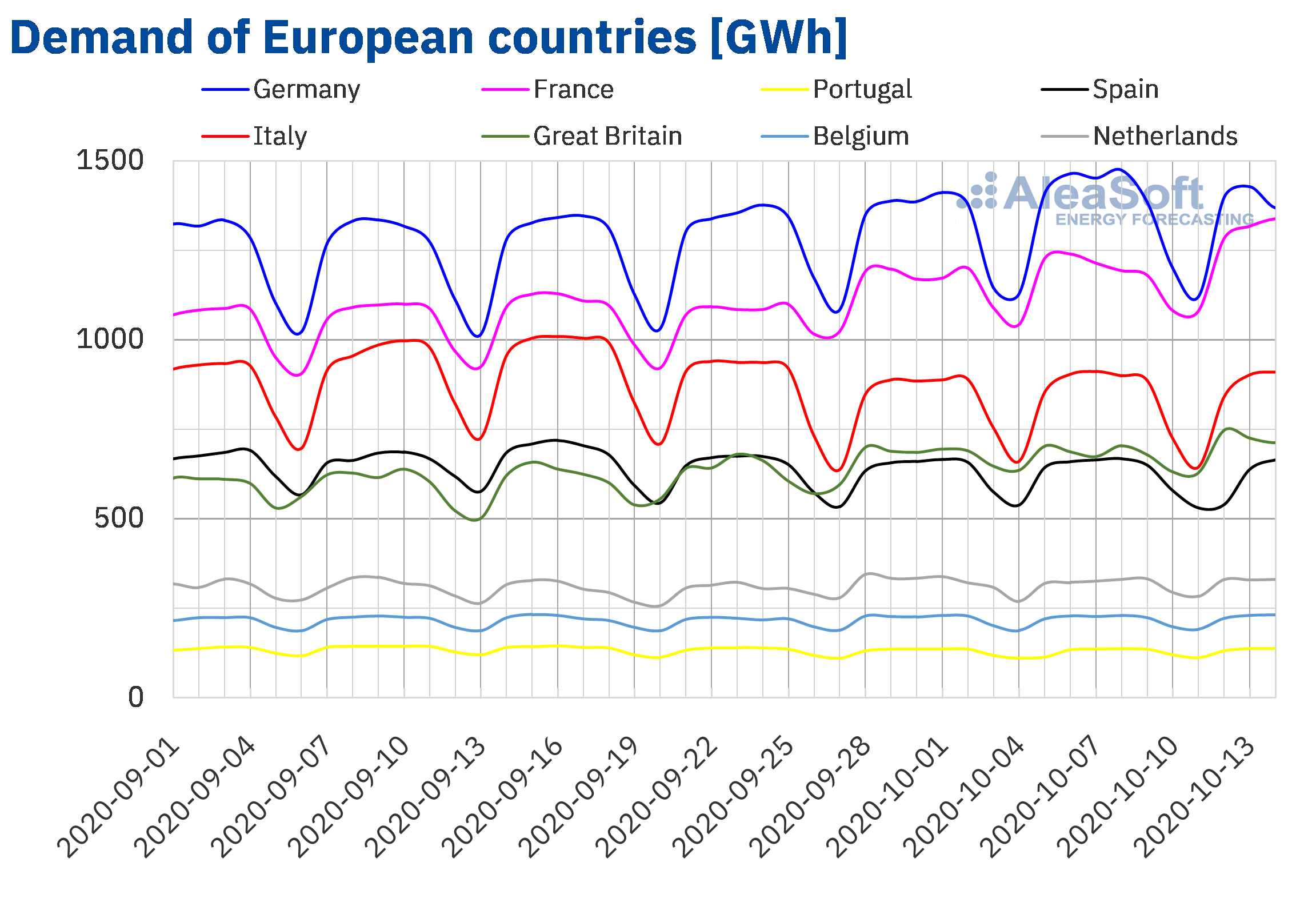

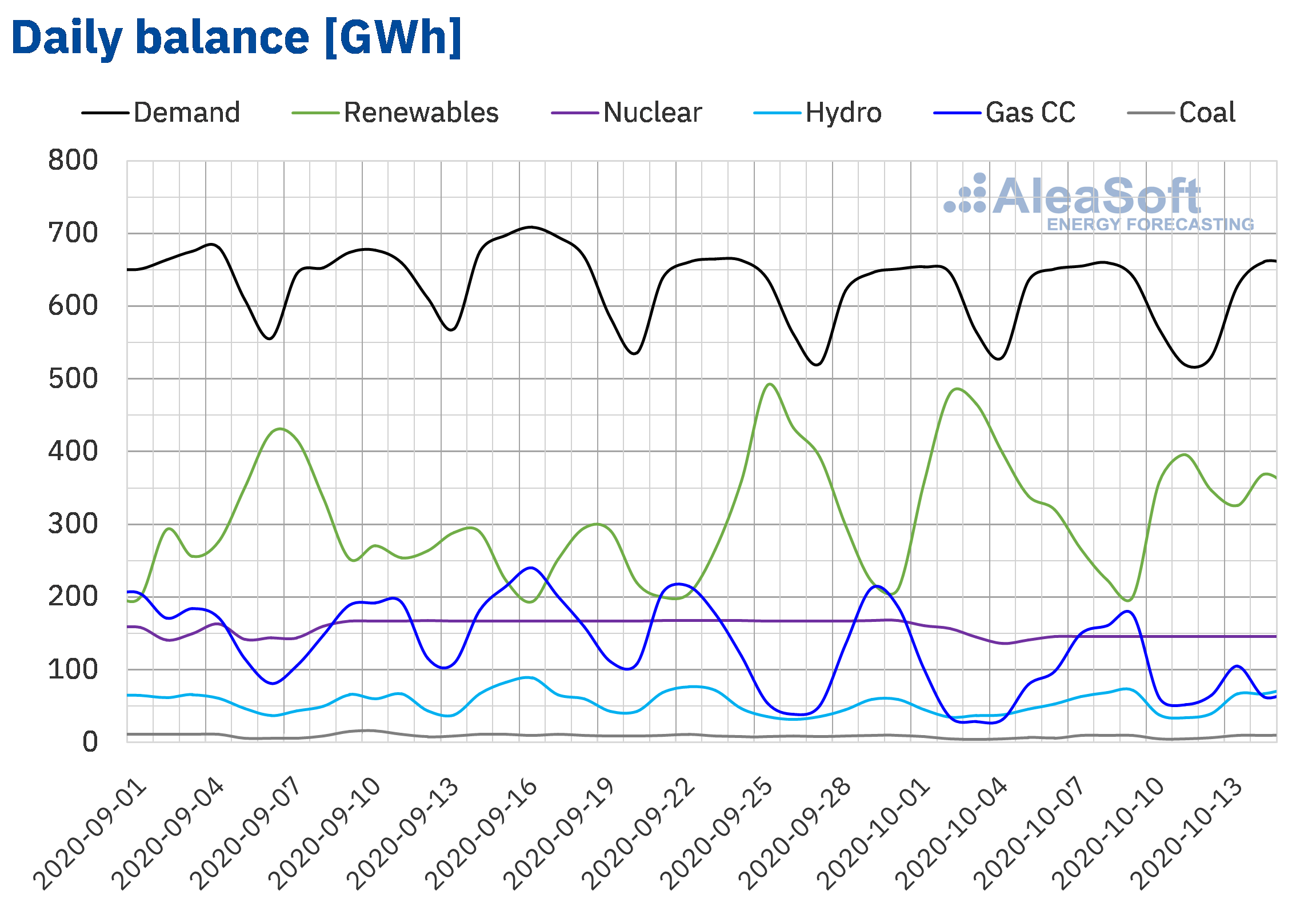

The electricity demand of the European markets registered ups and downs from Monday to Wednesday of the week of October 12 compared to the same period of the previous week. During those days, the average temperatures dropped between 2.5 °C and 4.7 °C compared to the average of the first three days of the week of October 5. The most notable changes in demand were the increases of 5.4%, 5.8% and 7.0% in the markets of Portugal, Great Britain and France respectively. In the market of the Netherlands the increase was 2.4%. The most neutral variations were the 0.8% increase in Belgium and the 0.6% decrease in Italy. On the other hand, in the German market the demand fell by 3.1% while in the Spanish market it fell by 6.3%.

The AleaSoft‘s demand forecasting indicates that at the end of the third week of October the average demand will continue to show the same trend registered during the first days of the week. The exception will be the market of the Netherlands, where the demand is expected to be slightly lower than that registered during the second week of October. The influence of the new confinement restrictions announced in some European countries to stop the second wave of infections by COVID‑19 will begin to be noticed at the end of this week and the beginning of the next, mainly in France and Spain, which at the moment present the most severe measures. The new adopted restrictions will cause a decrease in demand in these markets.

The evolution of the demand in this period of uncertainty can be followed at the AleaSoft‘s demand observatories, with daily updated data of the main markets.

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE, TERNA, National Grid and ELIA.

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE, TERNA, National Grid and ELIA.Mainland Spain, photovoltaic and solar thermal energy production and wind energy production

From October 12 to 14, the electricity demand of Mainland Spain fell by 6.3% compared to the same days of the previous week. When correcting the effect of the holiday of October 12, National Holiday of Spain, the fall was 1.5%. At the end of the third week of October, at AleaSoft the demand in the Spanish market is expected to conclude below the demand of the previous week.

The average solar energy production from Monday to Wednesday of the week of October 12 in Mainland Spain, which includes the photovoltaic and solar thermal technologies, increased by 6.9% compared to the average of the previous week. Comparing year‑on‑year, from October 1 to 14, the production with this technology had an increase of 43%. At the end of the third week of October, at AleaSoft the total solar energy production is expected to be slightly lower than that registered during the previous week.

The average wind energy production in Mainland Spain for the first three days of the third week of October increased by 32% compared to the average of the previous week. In the year‑on‑year analysis, the production registered during the first 14 days of October increased by 59% compared to the same days of 2019. According to the analysis carried out at AleaSoft, at the end of the week of October 12, it is expected that the production with this technology shows little variation compared to that registered in the second week of the month.

During the first three days of the week of October 12, the nuclear energy production maintained a level close to 146 GWh per day, similar to that registered the previous week. Since last October 3, the unit II of the Ascó nuclear power plant is in a scheduled shutdown.

Sources: Prepared by AleaSoft using data from REE.

Sources: Prepared by AleaSoft using data from REE.The hydroelectric reserves currently have 10 248 GWh stored, according to data from the Hydrological Bulletin of the Ministry for Ecological Transition and Demographic Challenge number 41, which represents a decrease of 69 GWh compared to the bulletin number 40.

European electricity markets

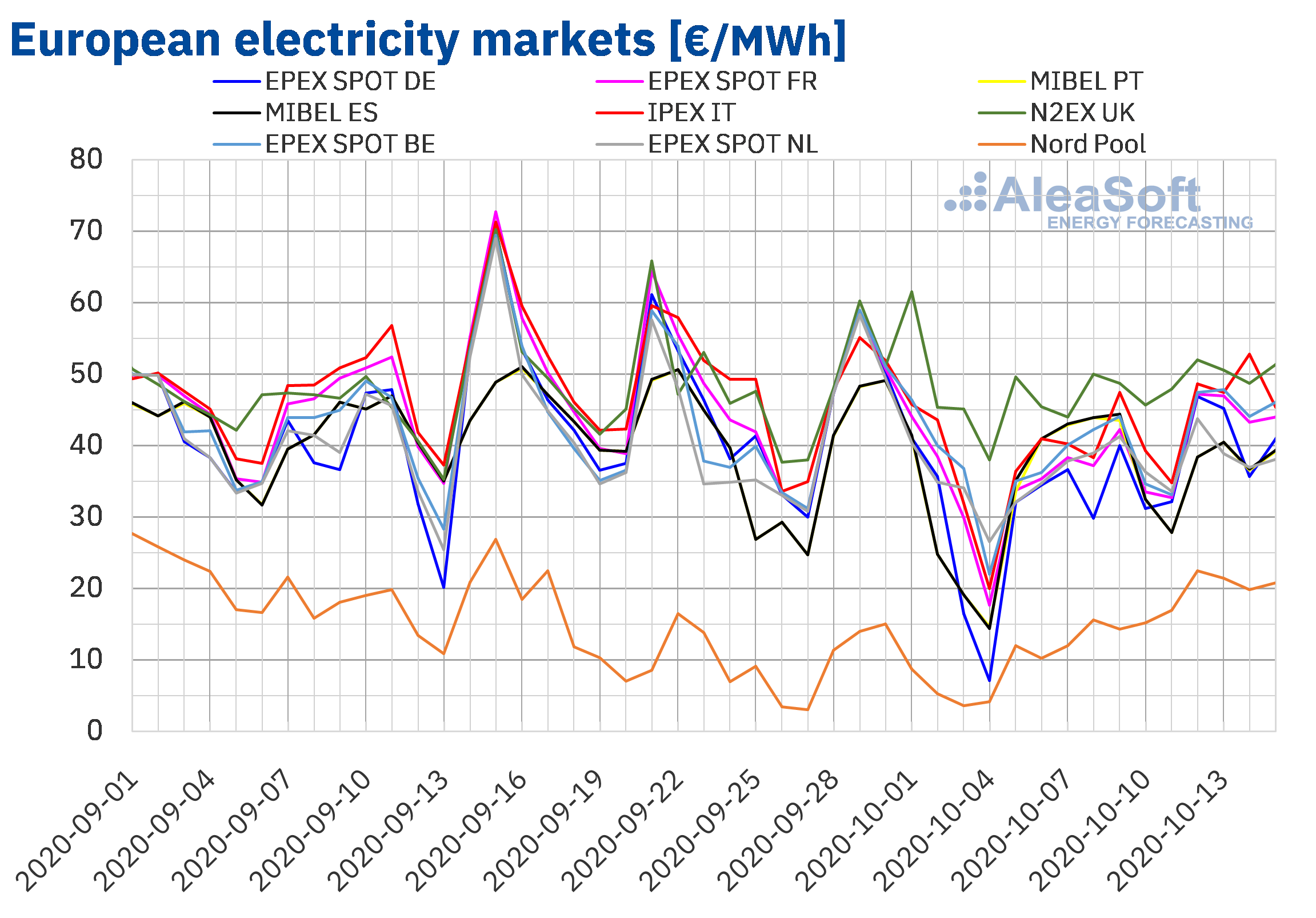

The first four days of the week of October 12, the prices increased in almost all the European electricity markets analysed at AleaSoft compared to the same period of the previous week. The exception was the MIBEL market of Spain and Portugal, which registered price drops of 5.0% and 4.2% respectively. On the other hand, the greatest price increase, of 70%, was that of the Nord Pool market of the Nordic countries. In contrast, in the N2EX market of Great Britain and the EPEX SPOT market of the Netherlands there were the lowest price increases, 7.2% and 9.8% in each case. In the rest of the markets, the increases were between 21% of the EPEX SPOT market of Belgium and 27% of the EPEX SPOT market of Germany.

As a consequence of these price increases, the average for the first four days of the third week of October was above €40/MWh in most of the analysed European markets. In the case of the markets of Portugal, Spain and the Netherlands, the prices were slightly lower, of €38.66/MWh, €38.73/MWh and €39.44/MWh respectively. While the market with the lowest average, of €21.14/MWh, was the Nord Pool market. On the other hand, the highest average price in this period, of €50.67/MWh, was that of the British market.

From Monday to Thursday of the week of October 12, the market with the highest daily prices for almost every day was the British market, except on Wednesday when the Italian market surpassed it. In contrast, the lowest daily prices in the period were those of the Nord Pool market. At the beginning of the week, the prices of the rest of the markets were quite coupled, except those of the MIBEL market, which were a little lower. But then the prices of the German and Dutch markets approached those of the MIBEL market.

The highest daily price of the first four days of the third week of October, of €52.82/MWh, was reached on Wednesday, October 14, in the IPEX market of Italy. On the other hand, the lowest daily price, of €19.80/MWh, was that of the same day in the Nord Pool market.

Regarding the hourly prices, in the first four days of the week of October 12, no negative hourly prices were reached in the analysed electricity markets. On the other hand, the highest hourly price, of €107.95/MWh, was reached at the hour 20 of Thursday, October 15, in the British market.

Source: Prepared by AleaSoft using data from OMIE, , N2EX, IPEX and Nord Pool.

Source: Prepared by AleaSoft using data from OMIE, , N2EX, IPEX and Nord Pool.The increase in electricity demand as well as the decrease in wind energy production in most markets and in solar energy production in countries such as Germany or Italy compared to the same days of the previous week favoured the increase in prices during the first days of the week of October 12.

The AleaSoft‘s price forecasting indicates that at the end of the third week of October the average price will be higher than that of the previous week in all European markets. On the other hand, for the week of October 19, the recovery of the wind energy production will favour price declines in most of these markets.

Iberian market

In the MIBEL market of Spain and Portugal, the average price of the first four days of the week of October 12 fell compared to the same period of the previous week. The fall was 5.0% in Spain and 4.2% in Portugal. In this period, the MIBEL market was the only one of the European electricity markets analysed at AleaSoft where the prices fell.

Due to these decreases, the average price from October 12 to 15 was €38.66/MWh in the Portuguese market and €38.73/MWh in the Spanish market. These were the second and third lowest prices in the European markets after the Nord Pool market average.

Regarding the daily prices of the MIBEL market, the minimum price, of €36.60/MWh, was reached on Wednesday, October 14, in the Portuguese market. While on October 13 the maximum daily price, of €40.47/MWh, was reached both in Spain and Portugal.

During the first days of the third week of October, the increase in wind and solar renewable energy production in the Iberian Peninsula allowed the prices to fall in the MIBEL market. Another factor that favoured this behaviour was the drop in demand in Spain due to the October 12 holiday.

The AleaSoft‘s price forecasting indicates that due to lower wind and solar energy production during the rest of the days of the third week of October the prices will increase, so that the weekly average will be higher than that of the previous week. On the other hand, it is expected that for the week of October 19, the prices will fall again favoured by the increase in wind energy production.

Electricity futures

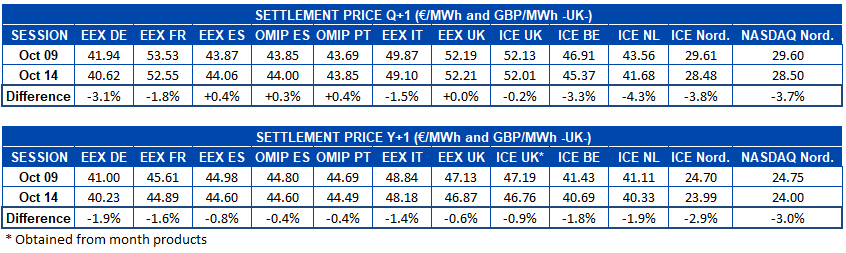

In the first three days of the week of October 12, the European electricity futures markets prices for the product of the first quarter of 2021 registered a fundamentally downward behaviour. Comparing the settlement of the session of Wednesday, October 14, with the settlement of the session of Friday, October 9, the prices rose in the Iberian region, both in the EEX market of Spain, by 0.4%, and in the OMIP market of Spain and Portugal, by 0.3% and 0.4% respectively. There was also a slight increase of €0.02/MWh in the EEX market of Great Britain, which together with the 0.2% decrease of the ICE market of the same region, were the markets with the lowest variations in the analysed period. In the rest of the markets, the prices fell between 1.5% and 4.3%.

On the other hand, the prices of the product of the calendar year 2021 in the European electricity futures markets registered a generalised downward behaviour compared to the settlement of the previous week. The market with the lowest variation, of ‑0.4%, was the OMIP of Spain and Portugal, while the NASDAQ market of the Nordic countries, with a decrease of 3.0%, was the one with the greatest decline, followed closely by the ICE market of the same region, where the decrease was 2.9%. In the rest of the markets the decreases were between 0.6% and 1.9%.

Brent, fuels and CO2

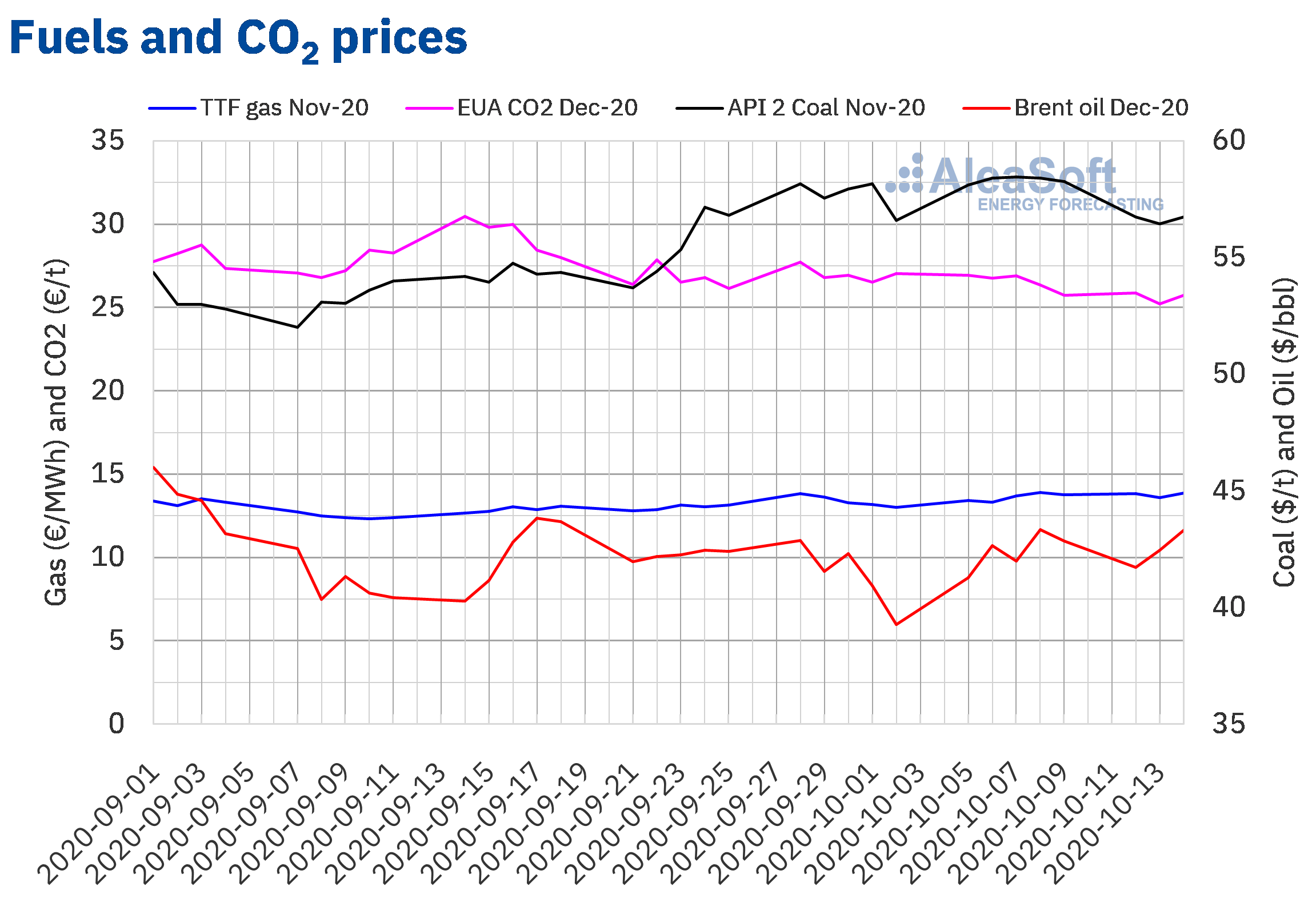

The Brent oil futures for the month of December 2020 in the ICE market on Monday, October 12, registered a settlement price of $41.72/bbl, 2.6% lower than that of the previous Friday. But the following days, the prices recovered and on Wednesday, October 14, the settlement price was $43.32/bbl, 3.2% higher than that of the previous Wednesday.

The news about the compliance with the agreements on the OPEC+ production levels and the declines in US reserves favoured the recovery of the prices. Furthermore, the recovery of the demand in India and China also exerted its upward influence on the prices. But the measures to control the coronavirus pandemic in Europe might affect the demand and favour lower prices in the coming days.

On the other hand, the TTF gas futures prices in the ICE market for the month of November 2020, the first days of the third week of October, remained above €13.50/MWh. The maximum settlement price, of €13.87/MWh, was reached on Wednesday, October 14. This price was 1.2% higher than that of the same day of the previous week.

Regarding the TTF gas prices in the spot market, the index price of Monday, October 12, was €13.74/MWh, the highest since the first half of December 2019. Subsequently, the prices fell to reach an index price of €13.46/MWh on Wednesday, October 14. But, on Thursday, the prices recovered to €13.67/MWh.

As for the API 2 coal futures prices in the ICE market for the month of November 2020, they began the third week of October with decreases. On Tuesday, October 13, a settlement price of $56.45/t was reached, 3.3% lower than that of the same day of the previous week. But, on Wednesday, the settlement price recovered slightly to the $56.75/t reached on Monday, October 12.

Regarding the CO2 emission rights futures prices in the EEX market for the reference contract of December 2020, the first three days of the third week of October they remained below €26/t. The maximum price of the week was reached on Monday, October 12, of €25.88/t, 0.6% higher than that of the Friday of the previous week. On the other hand, the minimum settlement price, of €25.23/t, was reached on Tuesday, October 13. This price was 5.8% lower than that of the previous Tuesday and the lowest since the end of July.

Source: Prepared by AleaSoft using data from ICE and EEX.

Source: Prepared by AleaSoft using data from ICE and EEX.AleaSoft analysis of the evolution of the energy markets in the second wave of the pandemic

The increase in those infected by COVID‑19 caused that, in recent days, in different countries and regions of Europe, more restrictive measures are being announced to try to stop the spread of the coronavirus. The adoption of these measures increases the existing uncertainty, due to the consequences that this can bring to the already affected European economies and, in the specific case of the energy markets, on the demand and prices. In the second part of the webinar “Energy markets in the recovery from the economic crisis” that is being organised at AleaSoft for next October 29, the evolution of the energy markets in this context will be discussed. Other topics to be addressed are the financing of the renewable energy projects and the importance of the forecasting in the audits and the portfolio valuation. The speakers will be Pablo Castillo Lekuona, Senior Manager of Global IFRS & Offerings Services and Carlos Milans del Bosch, Partner of Financial Advisory, both from the consulting firm Deloitte, as well as Oriol Saltó i Bauzà, Manager of Data Analysis and Modelling at AleaSoft.

The AleaSoft‘s long‑term prices curves of the European electricity markets take into account the most up‑to‑date scenarios of the evolution of the economic crisis. This forecasting is a fundamental input for the consulting in renewable energies, for example, in the PPAs, in the valuation of portfolios and the audits, and in the risk and coverage management.

The AleaSoft’s observatories are a tool that allows monitoring the evolution of the main European electricity, fuels and CO2 emission rights markets. The fact that the data is updated daily and that they are presented in comparative graphs of the recent weeks is very useful to analyse the effects on the markets due to the new measures that are being adopted to stop the spread of the coronavirus.

Source: AleaSoft Energy Forecasting.