AleaSoft, August 24, 2020. The prices of most European electricity markets fell during the third week of August due to the increase in wind energy production and the decrease in demand. In Germany some hours of Sunday registered negative values. However, in the Nord Pool market, the prices rose and the daily prices exceeded €10/MWh, something that did not happen since mid‑May. In the last week of the month, the prices are expected to rise, except in Germany where high wind energy production is expected.

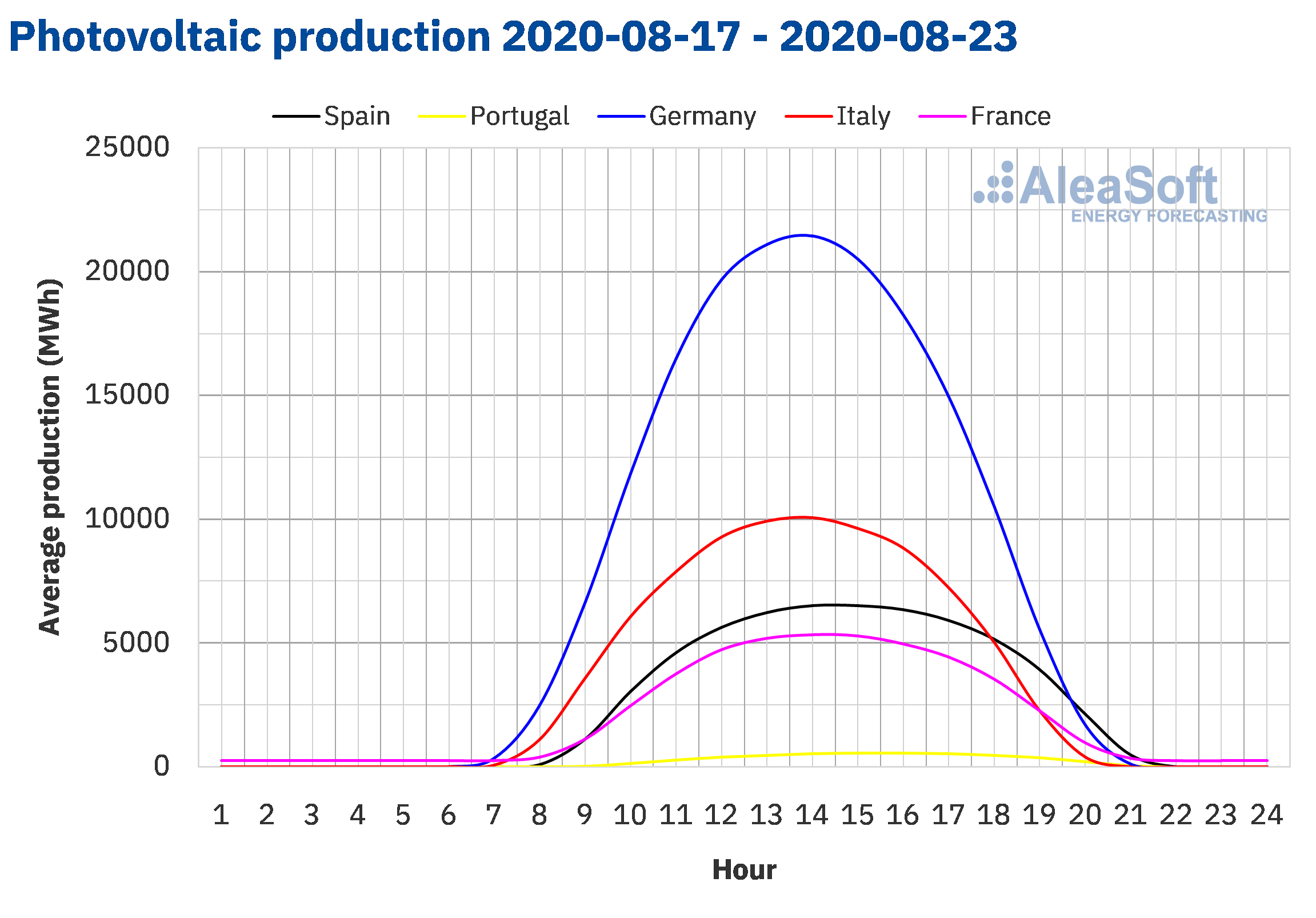

Photovoltaic and solar thermal energy production and wind energy production

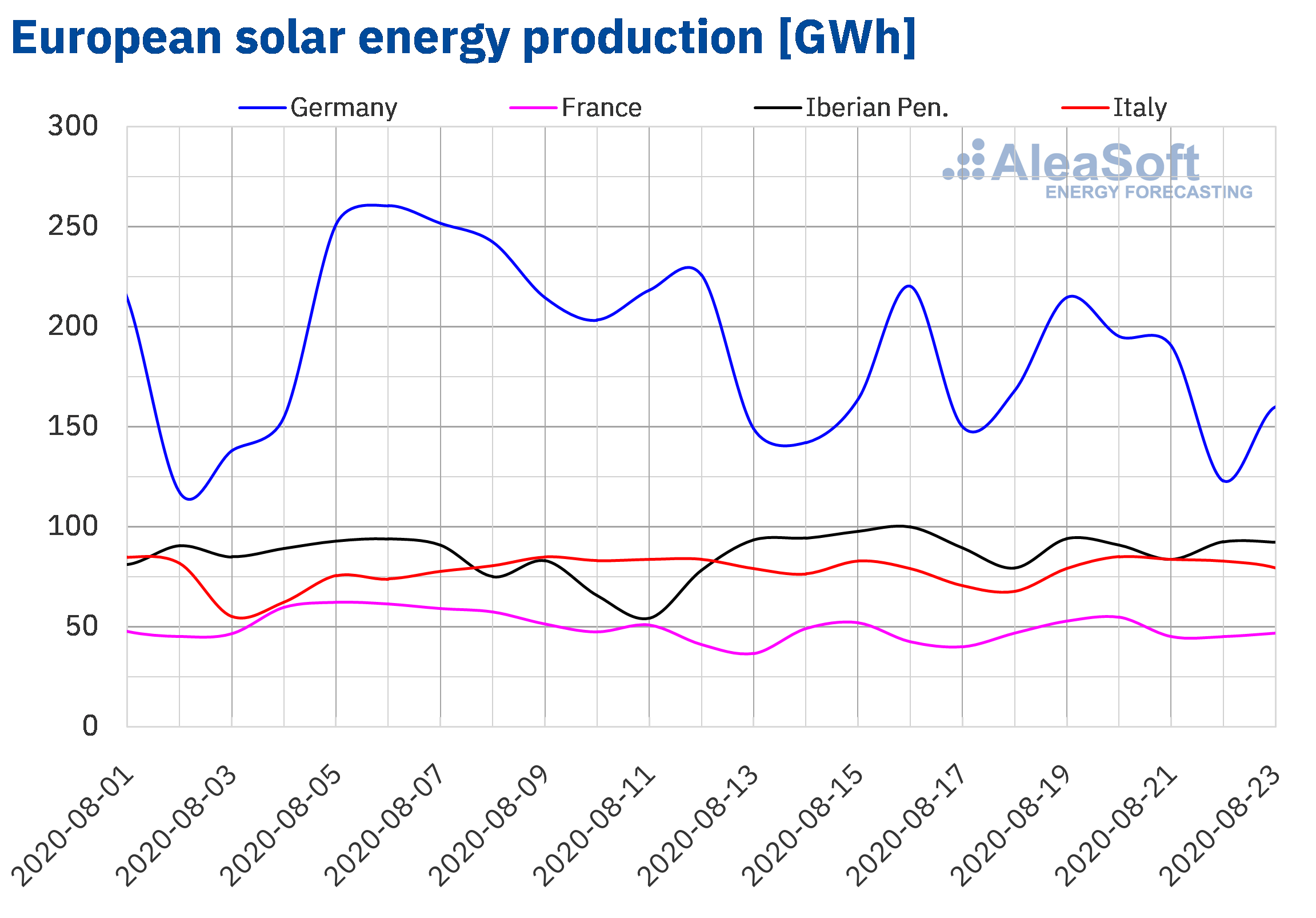

The solar energy production during the week of Monday, August 17, increased by 7.1% in the Spanish market and by 3.7% in the French market. On the contrary, in the German market it decreased by 9.2%, while in the markets of Italy and Portugal, the production decreased by 3.5% and 2.5% respectively.

During the first 23 days of August, the solar energy production was higher in all the markets analysed at AleaSoft when compared to that of the same period of 2019. The largest increases occurred in the Iberian Peninsula, being 35% in Spain and 22% in Portugal. The lowest variation was registered in the Italian market and it was 7.2%. In the German market, the production grew by 16% during this period and in the French by 12%.

For the week that began on Monday, August 24, the AleaSoft‘s solar energy production forecasting indicates a decrease in Spain, Germany and Italy.

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA.

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA. Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA.

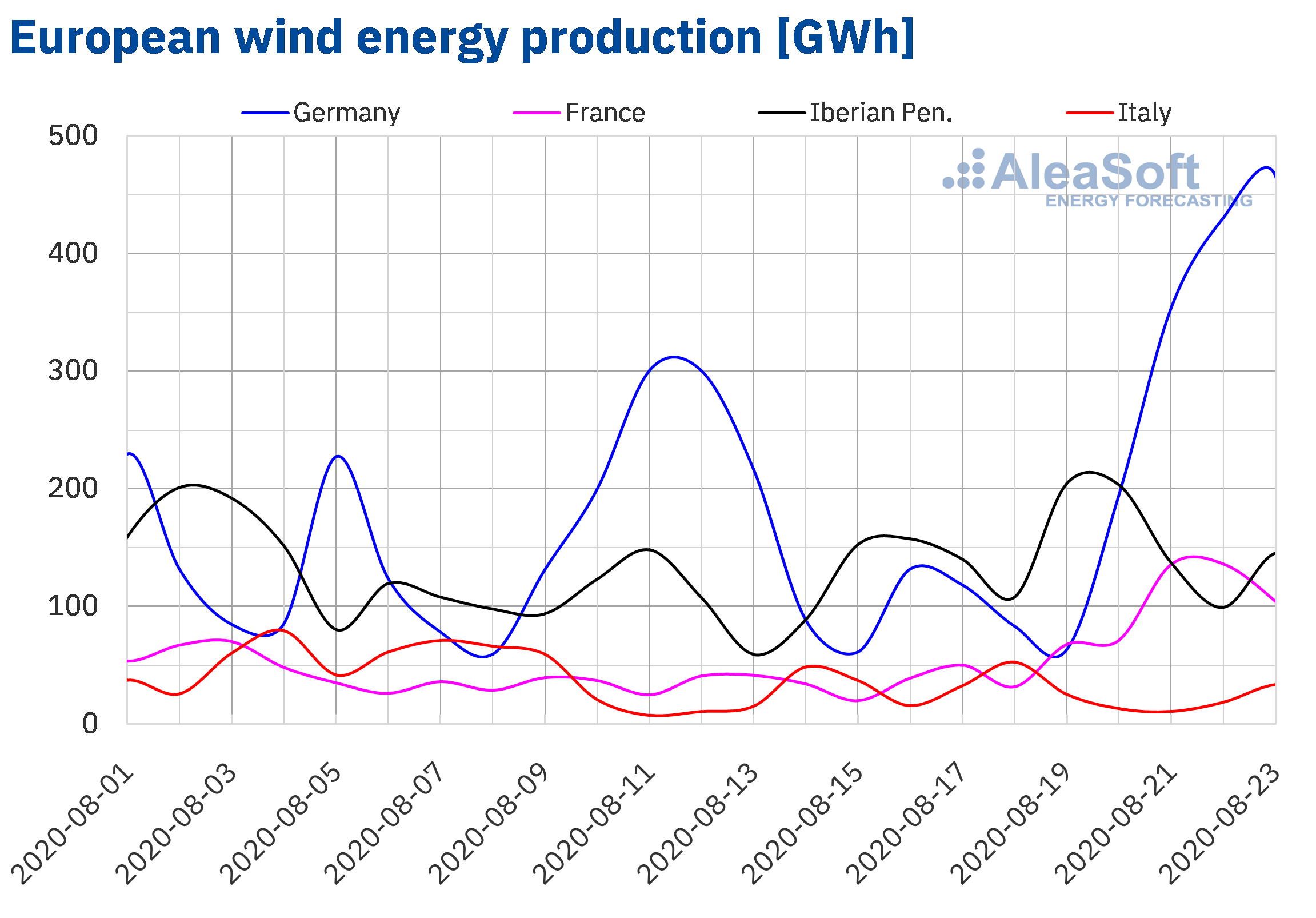

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA.During the third week of August, the wind energy production increased in all the analysed markets. In the French market the increase was 151%, while in the German market it was 32%. The smallest increases were registered in the Iberian Peninsula and Italy, with variations of 24% and 20% respectively.

Between August 1 and 23, the wind energy production decreased between 19% and 12% in the markets of Portugal, Germany and France compared to the same days of August 2019. On the contrary, in the Spanish market it increased 16% and in the Italian market 19%.

For the last week of August, the AleaSoft‘s wind energy production forecasting indicates an increase in production in the markets of Germany, Italy and France. On the contrary, for the markets of the Iberian Peninsula, a lower production with this technology is expected.

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA.

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE and TERNA.Renewable energy auctions

On August 24 and 25, the second renewable energy auction will be held in Portugal, scheduled for January and finally postponed due to the COVID‑19. On this occasion, 700 MW of solar energy will be auctioned and it will be only for the Alentejo and Algarve regions. Storage projects may participate in it and three modalities may be chosen, covering a period of 15 years from when the plants begin to produce. This is the first solar energy auction of 2020, planned by the Portuguese government to achieve the objectives set in the NECP for 2030, of having installed about 10 GW of solar energy. A new solar energy auction will be pending by the end of the year, where it is expected that about 500 MW or more will be offered, depending on the results obtained in this.

Electricity demand

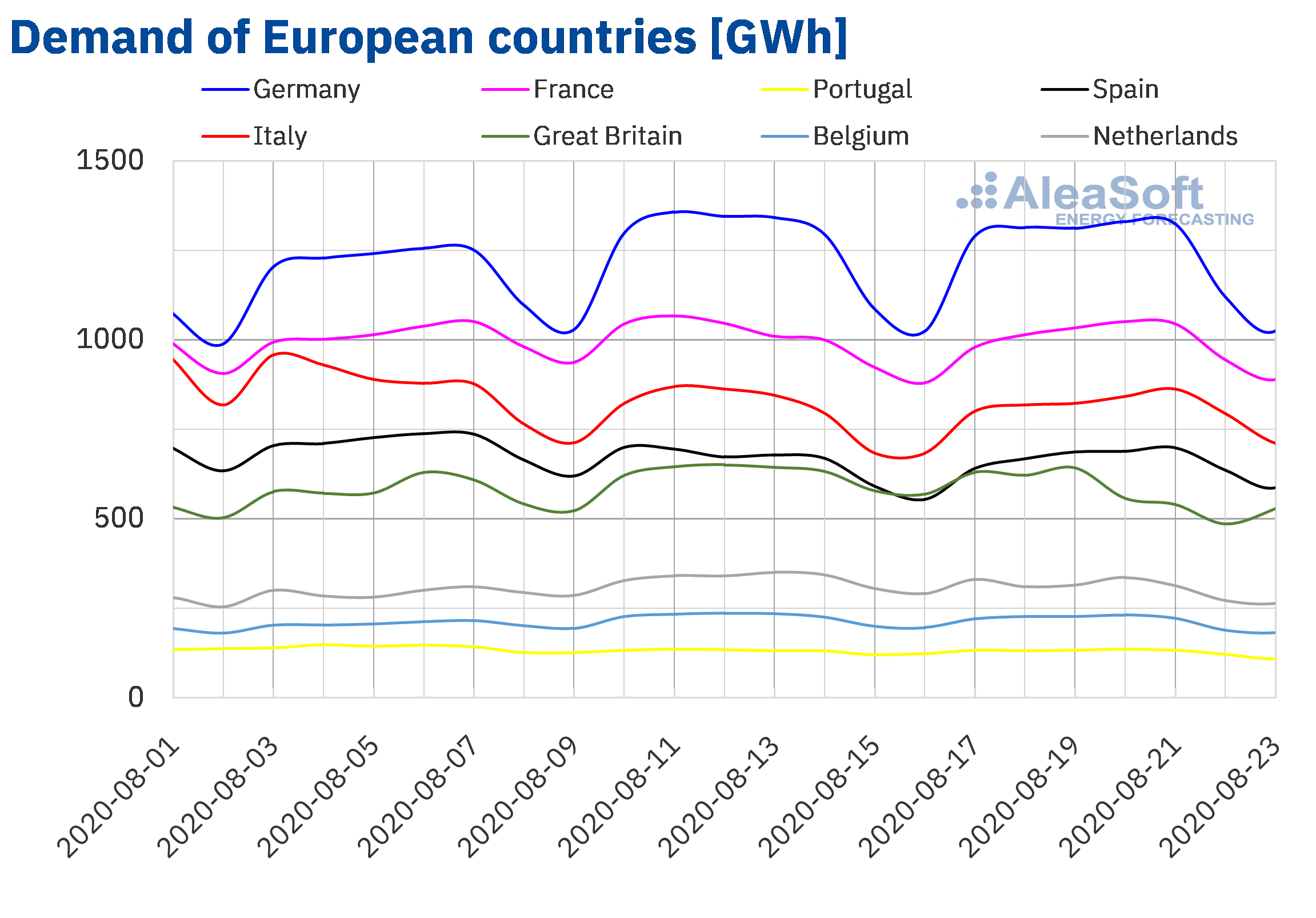

During the week of August 17, the electricity demand fell in most European markets compared to the second week of the month. The drop in demand was mainly due to the drop in temperatures during the third week of August after the end of the second heat wave of the summer. These decreases were between 0.2% and 7.7%. The exceptions were the markets of Spain and Italy where the temperatures were generally similar and the demand increased by 0.9% and 1.6% respectively.

At the AleaSoft‘s electricity markets observatories, the trend of the demand and other variables of interest of the European electricity markets in recent weeks can be analysed.

The AleaSoft’s demand forecasting for the current week indicates a decrease in demand in most of the markets due to the fact that the temperatures will continue to be less warm in most of Europe. The exceptions will be Spain and Portugal, where the demand is expected to be higher than that of the week of August 17, while in Great Britain it will be similar.

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE, TERNA, National Grid and ELIA.

Source: Prepared by AleaSoft using data from ENTSO-E, RTE, REN, REE, TERNA, National Grid and ELIA. European electricity markets

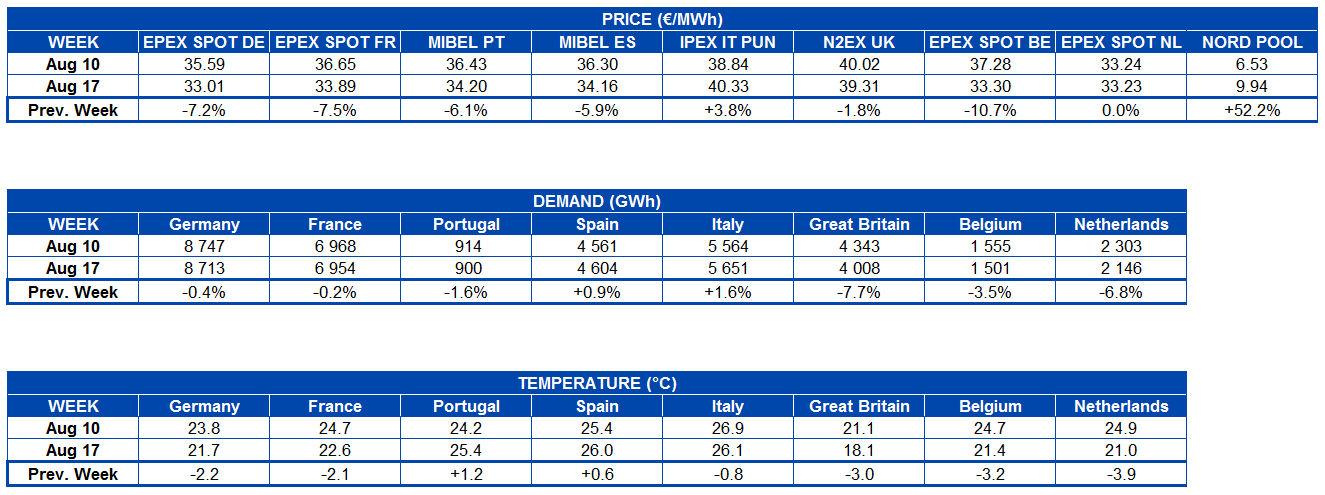

The week of August 17, the prices were lower than those of the previous week in most of the analysed European electricity markets. The exceptions were the Nord Pool market of the Nordic countries and the IPEX market of Italy with increases of 52% and 3.8% respectively. On the other hand, the market with the largest price drop, of 11%, was the EPEX SPOT market of Belgium, followed by the decreases of 7.5% in the French market and 7.2% in the German market. While in the EPEX SPOT market of the Netherlands, the average price during the third week of August was similar to that of the week of August 10, with a difference of €0.01/MWh. In the rest of the markets, the price drops were between 1.8% of the N2EX market of Great Britain and 6.1% of the MIBEL market of Portugal.

During the third week of August, the European market with the lowest average price, of €9.94/MWh, was the Nord Pool market. The rest of the analysed markets had weekly averages above €30/MWh. In the case of the IPEX market, it exceeded €40/MWh, becoming the market with the highest average price, of €40.33/MWh.

Regarding the daily prices, during the week of August 17, most European markets exceeded €40/MWh some day, except for the Nord Pool market and the MIBEL market of Spain and Portugal. The highest price, of €44.34/MWh, was reached in Italy on Wednesday, August 19.

In contrast, on Sunday, August 23, the prices were below €30/MWh in almost all markets. The exception was the N2EX market, which had a daily price of €39.73/MWh. On that day, the lowest prices were those of the Nord Pool and German markets, of €5.65/MWh and €16.33/MWh respectively.

On the other hand, on Sunday, August 23, negative hourly prices were reached in Germany. The lowest hourly price, of ‑€16.18/MWh, was at hour 14. This price was the lowest in this market since Sunday, July 26. In turn, these negative prices contrast with the hourly prices of Monday, August 24, in Great Britain, which reached €96.58/MWh for hour 20. Such high prices were not reached in the British market since March.

Source: Prepared by AleaSoft using data from OMIE, , N2EX, IPEX and Nord Pool.

Source: Prepared by AleaSoft using data from OMIE, , N2EX, IPEX and Nord Pool.The general increase in wind energy production in Europe and the increase in solar energy production in countries such as France and Spain, as well as the decrease in electricity demand, favoured the price decreases of the week of August 17 in most analysed markets. With the exception of the Italian market, where the increase in demand during this period, despite the high wind energy production, caused the prices to increase, also supported by the increase in gas prices.

The AleaSoft‘s price forecasting indicates that the week of August 24 the prices will increase in most European markets, except in the German market, where a significant increase in wind energy production is expected.

Electricity futures

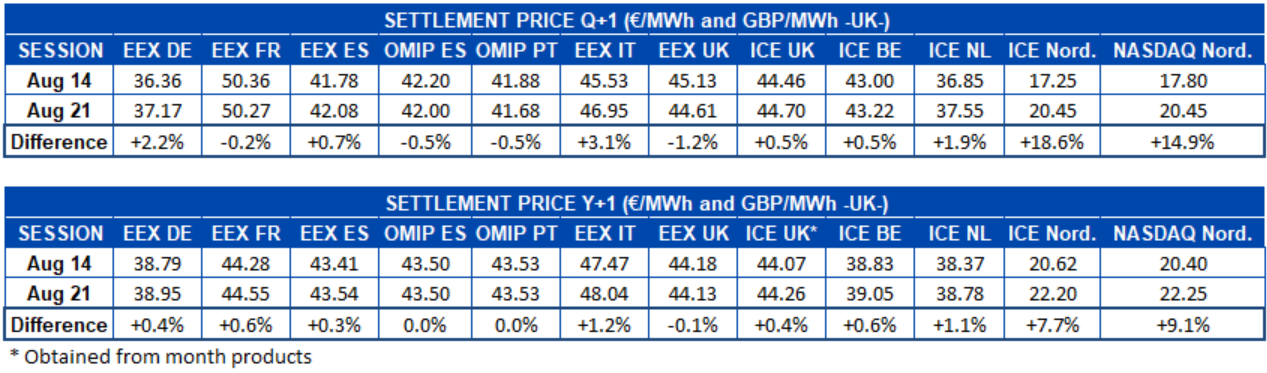

During the week of August 17, the electricity futures prices for the next quarter registered a mostly upward behaviour with respect to the end of the week of August 10. The exceptions were the EEX market of Great Britain and France and the OMIP market of Spain and Portugal, where the prices fell by 1.2% in the British market, 0.2% in the French and 0.5% in those of the Iberian Peninsula. The rest of the markets registered increases that went from 0.5% of the ICE market of Great Britain and Belgium to 19% in the same market for the Nordic countries. In Spain and Great Britain, different behaviours were registered between the different markets of those regions. For Spain, the prices increased in the EEX market while in the OMIP market they decreased. In the case of Great Britain, the prices decreased in the EEX market while they increased in the ICE market.

For the Cal‑21 product, the behaviour of the markets during the third week of August was more marked upwards than in the quarterly product. The prices were reduced only in the EEX market of Great Britain, with a variation of ‑0.1%. The OMIP market of Spain and Portugal did not register any variation, as the session of August 21 closed with the same price as that of Friday, August 14. The rest of the markets registered increases of between 0.3% of the EEX market of Spain and 9.1% of the NASDAQ market of the Nordic countries. For this product, Great Britain also had a different behaviour in the EEX and ICE markets. Although it should be noted that in the ICE market the annual product is not negotiated and AleaSoft works based on an estimate that uses the average of the monthly products corresponding to the calendar year.

Brent, fuels and CO2

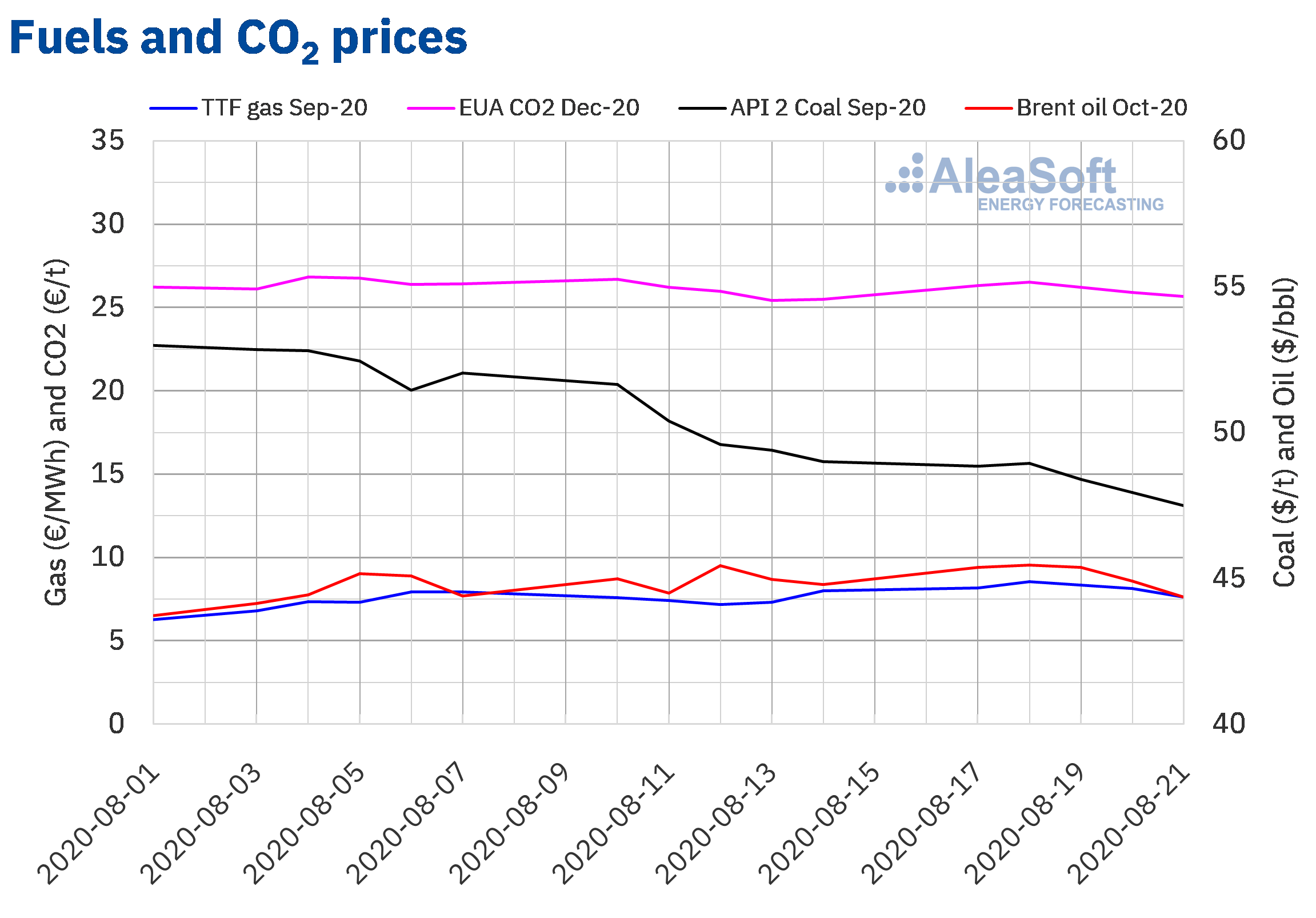

The first two days of the third week of August, the Brent oil futures prices for the month of October 2020 in the ICE market increased. As a consequence, on Tuesday, August 18, a settlement price of $45.46/bbl was registered. This price is the highest since the beginning of March. But for the rest of that week there were declines in prices. On Friday, August 21, the settlement price was $44.35/bbl. This is the second lowest settlement price since August started.

The concerns about the increase in COVID‑19 cases and the increase in production of the OPEC+ member countries are favouring the decline in prices. However, the Hurricane Marco and Tropical Storm Laura threaten the production in America, which already decreased on Sunday, August 23, in the Gulf of Mexico.

On the other hand, the cessation of the civil war in Libya may allow the increase in production in this country soon. This will increase the downward pressure on prices, especially when the weather conditions improve and the production recovers in the Gulf of Mexico.

As for the TTF gas futures prices in the ICE market for the month of September 2020, on Tuesday, August 18, they reached the highest settlement price in the last four months, of €8.55/MWh. However, as of Wednesday, August 19, the prices began to decrease and the settlement price of Friday, August 21, was €7.62/MWh, 5.0% lower than that of Friday, August 14.

Regarding the TTF gas in the spot market, on Wednesday, August 20, an index price of €8.18/MWh was reached, the highest since the end of March. The following days, the prices fell to €6.55/MWh of the weekend. But on Monday, August 24, the price increased again to €6.78/MWh.

On the other hand, the API 2 coal futures prices in the ICE market for the month of September 2020, the third week of August, remained below $50/t, with a generally downward trend. Consequently, on Friday, August 21, a settlement price of $47.50/t was registered, 3.1% lower than that of Friday of the second week of the month and the lowest since the third week of June.

As for the CO2 emission rights futures in the EEX market for the reference contract of December 2020, they reached the highest settlement price of the third week of August, of €26.54/t, on Tuesday, August 18. Subsequently, the prices fell until reaching a settlement price of €25.65/t on Friday, August 21.

Source: Prepared by AleaSoft using data from ICE and EEX.

Source: Prepared by AleaSoft using data from ICE and EEX.AleaSoft analysis of the recovery of the energy markets at the end of the economic crisis

At AleaSoft a series of webinars “Energy markets in the recovery of the economic crisis” is being organised to analyse the evolution of the energy markets after the economic crisis caused by the COVID‑19 pandemic. The economic data of the second quarter of 2020 showed significant falls in GDP at the European level. Although this level of falls is not expected to be repeated, as they occurred as a result of the confinement measures taken to contain the pandemic, the outbreaks of the disease that are occurring , which may increase when in September and October the school year in person starts, continue to generate a lot of uncertainty. The webinars will analyse the effects on the markets in this situation, as well as the financing of the renewable energy projects. The importance of the forecasting in audits and portfolio valuation will also be discussed. The webinar will be held in two parts, on September 17 and October 29, and it will feature speakers from Deloitte, Engie, Banco Sabadell and AleaSoft.

At AleaSoft, the long‑term price forecasting of the main European electricity markets were updated, taking into account the scenarios of recovery from the coronacrisis.

To analyse the evolution of the European electricity, fuels and CO2 markets, at AleaSoft the observatories were also created. This tool includes charts of the main variables of the markets with updated data of the last weeks.

Source: AleaSoft Energy Forecasting.