AleaSoft Energy Forecasting, May 22, 2026. Fifteen years after producing a long‑term forecast for the Iberian electricity market, comparing it with the actual evolution of prices offers a key lesson: rigorous forecasting is essential for financing renewable energy, batteries and electricity assets without inflating expectations or taking on debt levels that the market cannot sustain. This article also marks the 750th collaboration between AleaSoft Energy Forecasting and El Periódico de la Energía.

Fifteen years later: a forecast with perspective

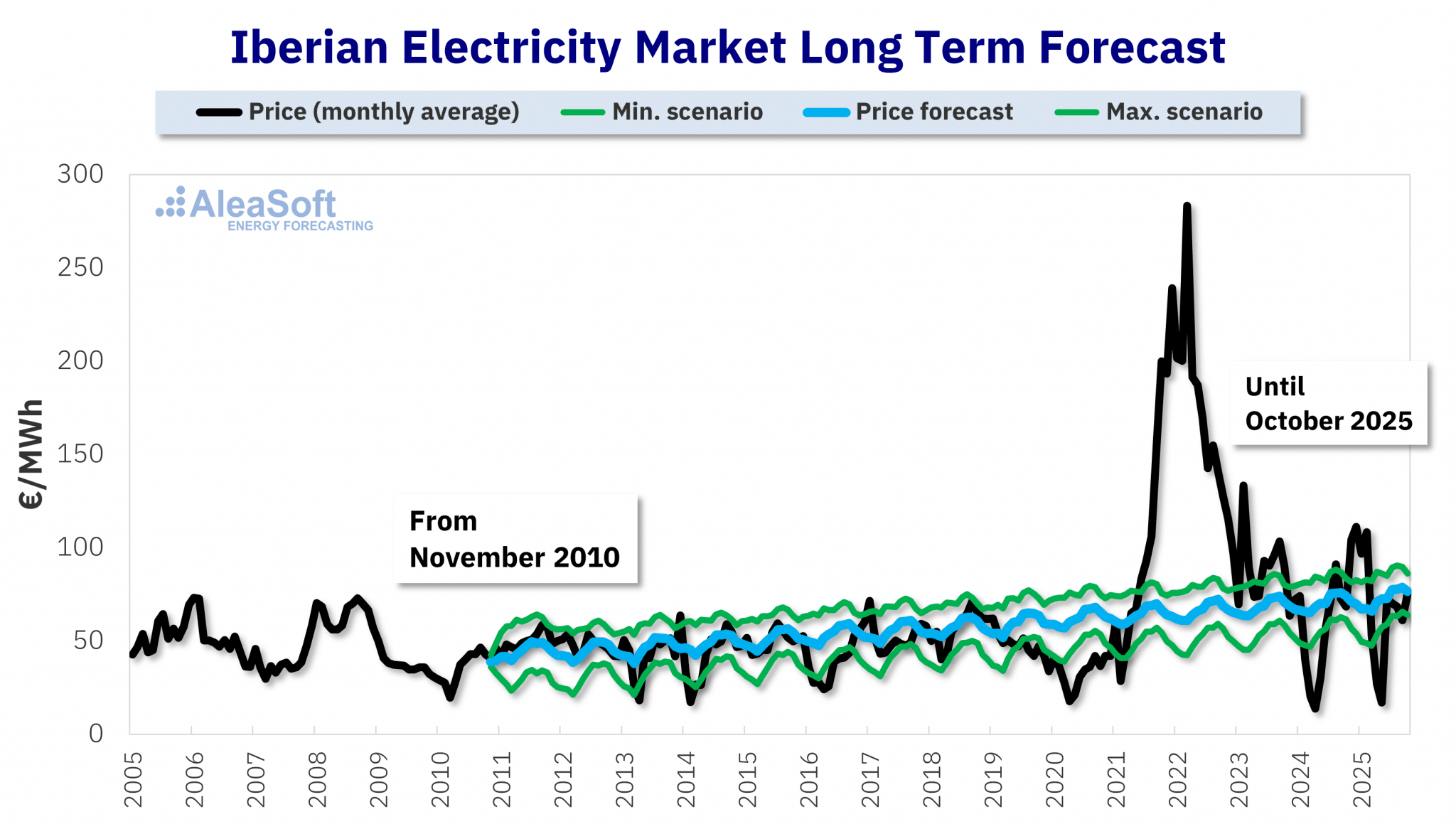

In November 2010, AleaSoft Energy Forecasting prepared a long‑term forecast for the Iberian electricity market. Fifteen years later, comparing that forecast with the actual evolution of prices leads to a clear conclusion: well‑founded long‑term forecasts are not intended to predict every short‑term episode accurately, but rather to anticipate the structural trends of the market.

The graph shows how, for much of the period analysed, monthly market prices moved around the projected path and within the range of scenarios considered. Naturally, the period included extraordinary events that no long‑term model can reproduce precisely, such as the COVID‑19 crisis, which depressed demand and prices, or the European energy crisis of 2021 and 2022, which pushed prices to historically high levels. However, with the perspective provided by fifteen years of data, the forecast succeeded in capturing the structural evolution of the Iberian market.

Source: AleaSoft Energy Forecasting.

Source: AleaSoft Energy Forecasting.This result also illustrates the role that artificial intelligence, advanced statistical models and expert knowledge of the energy sector can play when rigorously applied to electricity markets. AleaSoft has been using artificial intelligence‑based models in energy market forecasting for 27 years.

The value of a forecast does not lie in inflating expectations

Comparing forecasts with reality also revives a discussion that remains highly relevant today: which forecasts should be used to finance renewable energy, storage or hybridisation projects.

Fifteen years ago, a prudent and technically robust forecast such as this one may have appeared unattractive from a purely financial perspective. A less aggressive price path implied lower expected revenues, a tighter IRR and, therefore, a lower debt‑leveraging capacity. In that context, some developers may have been tempted to use artificially optimistic scenarios to improve the apparent profitability of their projects and raise more debt.

The problem is that an inflated forecast does not improve the project. It merely improves its financial presentation temporarily. If actual prices fail to match expectations, the debt remains, but the revenues do not materialise. This is when cash‑flow tensions, forced refinancing and, in some cases, a loss of asset value begin to emerge, even though the assets may still retain strong technical potential.

The lesson of the photovoltaic bubble

The photovoltaic sector provides a particularly clear example of this dynamic. During certain periods, excessively optimistic expectations for future prices contributed to the construction of financial models showing high paper returns and debt levels that were difficult to sustain under more realistic market scenarios.

When prices fall or remain below the expectations used for financing, market reality prevails. The issue does not affect only purely merchant projects. Many developers and IPP have accumulated highly demanding debt structures because they financed assets using forecasts that failed to reflect long‑term risks adequately.

Responsibility in such cases does not usually lie at a single point in the chain. Developers, financiers, advisers and intermediaries all share the incentive to use scenarios that make the transaction viable in the short term. However, a project’s financial sustainability depends on revenue assumptions being robust, traceable and defensible throughout the entire lifetime of the asset.

Photovoltaics, batteries and grid connection points: an optimistic but realistic view

This analysis should not be confused with a negative view of photovoltaic energy. On the contrary, photovoltaic energy production remains one of the most competitive technologies for producing electricity. In an electricity system moving towards decarbonisation, producing a photovoltaic MWh carries increasing strategic value.

Moreover, grid connection points are becoming increasingly scarce assets. Their limited availability makes them highly valuable for renewable development, particularly in a context where the electrification of the economy, energy storage and the gradual replacement of fossil‑fuel technologies will increase the need for new renewable capacity.

The incorporation of batteries can further improve the real profitability of projects. Optimal hybridisation between renewables and storage can increase captured prices, reduce curtailment, shift energy towards higher‑value hours and open up new revenue streams in balancing services or flexibility schemes.

The new phase: refinancing with rigorous forecasts

The sector is now entering a phase in which many decisions will revolve around debt refinancing, portfolio restructuring and the revision of business plans. In this context, the key question once again becomes: which long‑term price forecasts will be used as the benchmark?

The answer will have significant consequences. An overly optimistic forecast may once again create leverage problems. An excessively conservative forecast may undervalue assets that will play a central role in an electrified, decarbonised electricity system with increasing storage participation.

The challenge lies in working with forecasts capable of reflecting the complexity of the market: demand evolution, renewable energy deployment, nuclear phase‑out, gas and CO₂ prices, interconnections, price cannibalisation, storage, hybridisation, curtailment, flexibility services and regulatory changes.

Looking 5, 10, 20 or 40 years ahead

Energy investment decisions are not made for the short term. A renewable energy project, a battery or a hybrid plant requires a market vision spanning decades. That is why the value of a long‑term forecast does not lie in providing an isolated figure, but in building a coherent vision of scenarios, risks and opportunities.

If it were possible to observe today the captured prices 5, 10, 20 or 40 years from now, many assets currently under pressure because of their financial structures could reveal a much higher strategic value. In a zero‑emissions electricity system, with greater electrification and without nuclear power plants, renewable energy production, storage and grid connection points will play a fundamental role.

750th collaboration with El Periódico de la Energía

This article marks AleaSoft’s 750th collaboration with El Periódico de la Energía, an editorial relationship that began in 2019 and has continued with at least two publications every week.

Throughout these years, the objective has been to provide analysis, context and a long‑term perspective on European energy markets, price developments, project financing, renewable energy, PPA, storage and the major challenges of the energy transition.

The forecast produced in 2010 for the Iberian electricity market encapsulates that philosophy well: in a sector so exposed to volatility, uncertainty and regulatory changes, strategic decisions require independent, rigorous forecasts consistent with market fundamentals.

Source: AleaSoft Energy Forecasting.