Heat, Hormuz and high electricity prices: summer reminds the market of the value of hedging

AleaSoft Energy Forecasting, July 22, 2026. High temperatures, geopolitical risk in the Strait of Hormuz, low…

Read more >>

AleaSoft Energy Forecasting, July 22, 2026. High temperatures, geopolitical risk in the Strait of Hormuz, low…

Read more >>

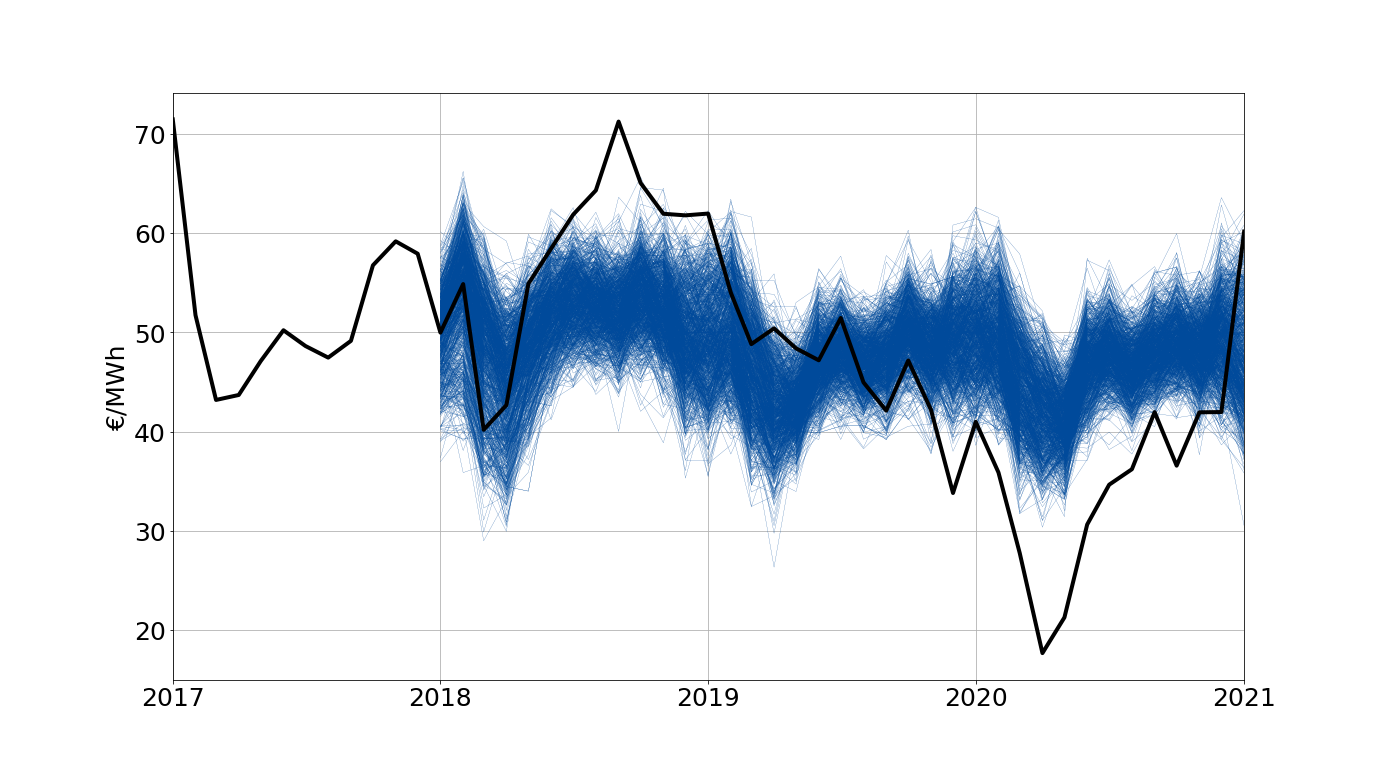

AleaSoft makes price forecasts for European markets in the medium term. The price forecasts have an hourly granularity, a 3-year horizon, and include probability distributions (forecasts with stochasticity) for each period (month, quarter and year) within the forecast horizon.

Forecasts with price stochasticity allow us to analyse the impact of the stochasticity of the explanatory variables on the medium-term price forecasts, and are a basic tool for risk management and the calculation of Values-at-Risk.

Price forecasts are calculated using data from the distributions of the explanatory variables and their associated probabilities. The main variables26 that are obtained stochastically are the following:

For each of them, their intrinsic variability is estimated based on their values historical.

A sufficiently high number of random forecasts is calculated for each of the explanatory variables consistent with each other. With these simulations of the variables, the corresponding simulations of the market price are calculated, and from these the percentiles of the price distribution are calculated.

Stochasticity will be generated using all the recorded data available at that time.

The shipment will include the probability distributions for each monthly, quarterly and annual product being currently trading in the futures markets within the forecast horizon. For each period, the distribution will include a reference to the latest prices traded in the stock markets. futures.

Short-term forecasts are essential for any actor participating in the daily market: producers, direct consumers, marketers, traders, etc.

Forecasts are offered in product format and in format service.

The product format consists of the installation of an application that works automatically, both for updating the data and for obtaining forecasts.

The service format consists of the daily sending of updated price forecasts and the main explanatory variables.

The main explanatory variables used in the price forecasts of short-term energy markets are demand, which in turn uses temperature and work force as explanatory variables, and the production of the different technologies, among which There are wind, solar, hydroelectric and nuclear. Furthermore, the price forecasts of the interconnected countries are taken into account and the forecast is optimised with the exchange capacity available in international interconnections.

The AleaSoft medium-term electricity market price simulations service includes 1000 price simulations with a horizon up to three years and hourly or monthly granularity. These simulations are an essential input for advanced analyses for risk management and allow obtaining probability distributions, estimates of Value-at-Risk and confidence bands. All this with a probabilistic metric with a completely scientific basis.

To obtain the price simulations, 1000 simulations of the following explanatory variables are carried out, taking into account the most probable average scenarios, the historical variability, the expected variability and the temporal correlations between them: